If you still have money in European banks, you need to get it out. This is particularly true if you have money in southern European banks. As I write this, the final details of the Cyprus bailout are being worked out, but one thing has become abundantly clear: at least some depositors are going to lose a substantial amount of money. Personally, I never dreamed that they would go after private bank accounts in Europe, but now that this precedent has been set it should be apparent to everyone that no bank account will ever be considered 100% safe ever again. Without trust, a banking system simply cannot function, and right now there are prominent voices on both sides of the Atlantic that are loudly warning that trust in the European banking system has been shattered and that people need to get their money out of those banks as rapidly as they can. Even if you don’t end up losing a significant chunk of your money, you could still end up dealing with very serious capital controls that greatly restrict what you are able to do with your money. Just look at what is already happening in Cyprus. Cash withdrawals through ATMs have now been limited to 100 euros per day, and when the banks finally do reopen there will be strict limits on financial transactions in order to prevent a full-blown bank run. And of course anyone with half a brain will be trying to get as much of their money as they can out of those banks once they do reopen. So the truth is that the problems for Cyprus banks are just beginning. The size of the “bailout” that will be needed to keep those banks afloat will just keep getting larger and larger the more money that is withdrawn. Cyprus is heading for a complete and total banking meltdown, and because the economy of the island is so dependent on banking that means that the economy of the entire nation is going to collapse. Sadly, similar scenarios will soon start playing out all over Europe.

If you still have money in European banks, you need to get it out. This is particularly true if you have money in southern European banks. As I write this, the final details of the Cyprus bailout are being worked out, but one thing has become abundantly clear: at least some depositors are going to lose a substantial amount of money. Personally, I never dreamed that they would go after private bank accounts in Europe, but now that this precedent has been set it should be apparent to everyone that no bank account will ever be considered 100% safe ever again. Without trust, a banking system simply cannot function, and right now there are prominent voices on both sides of the Atlantic that are loudly warning that trust in the European banking system has been shattered and that people need to get their money out of those banks as rapidly as they can. Even if you don’t end up losing a significant chunk of your money, you could still end up dealing with very serious capital controls that greatly restrict what you are able to do with your money. Just look at what is already happening in Cyprus. Cash withdrawals through ATMs have now been limited to 100 euros per day, and when the banks finally do reopen there will be strict limits on financial transactions in order to prevent a full-blown bank run. And of course anyone with half a brain will be trying to get as much of their money as they can out of those banks once they do reopen. So the truth is that the problems for Cyprus banks are just beginning. The size of the “bailout” that will be needed to keep those banks afloat will just keep getting larger and larger the more money that is withdrawn. Cyprus is heading for a complete and total banking meltdown, and because the economy of the island is so dependent on banking that means that the economy of the entire nation is going to collapse. Sadly, similar scenarios will soon start playing out all over Europe.

So if you hear that a “deal” has been reached to “bail out” Cyprus, please keep in mind that the economy of Cyprus is going to collapse no matter what happens. It is just a matter of apportioning the pain at this point.

According to the New York Times, it looks like much of the pain is going to be placed on the backs of those with deposits of over 100,000 euros…

The revised terms under discussion would assess a one-time tax of 20 percent on deposits above 100,000 euros at the Bank of Cyprus, which has the largest number of savings accounts on the island. Because the Bank of Cyprus suffered huge losses on bets that it took on Greek bonds, the government appears to be taking depositors’ money to help plug the hole.

A separate tax of 4 percent would be assessed on uninsured deposits at all other banks, including the 26 foreign banks that operate in Cyprus.

Does that sound bad to you?

Well, if a deal is not reached, there is a possibility that those with uninsured deposits could lose everything. According to Ekathimerini, EU officials are telling Cyprus to choose between a “bad scenario” and a “very bad scenario”…

The main question surrounds the future of the island’s largest lender, Bank of Cyprus. If unsecured deposits (above 100,000 euros) at all Cypriot banks are taxed then large savings at Bank of Cyprus are likely to be taxed between 20 and 25 percent. If the levy is not imposed on deposits at other lenders, the haircut for Bank of Cyprus customers will be much larger.

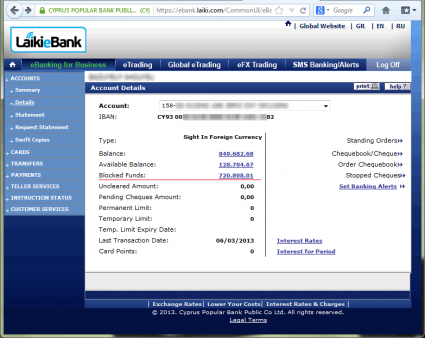

The option of a full bail in of Bank of Cyprus depositors is still on the table. As with the Popular Bank of Cyprus (Laiki), which is to go through a resolution process, the full bail in option could lead to deposits above 100,000 euros being lost. The only compensation for unsecured depositors will be shares in the “good” bank that will be created by a possible merger between the “healthy” Laiki and Bank of Cyprus entities.

When asked by Kathimerini how the Cypriot economy will survive if all company and personal deposits above 100,000 euros disappear from the country’s two biggest lenders, the EU official said: “Unfortunately, Cyprus’s choices are between a bad scenario and a very bad scenario.”

So what percentage of the deposits in Cyprus are uninsured deposits?

Well, nobody knows for sure, but according to JPMorgan close to half of the total amount of money on deposit in EU banks as a whole is uninsured.

Do you think that some of those people will start moving their money to safer locations after watching how things are going down in Cyprus?

They would be crazy if they didn’t.

And if you think that “deposit insurance” will keep you safe, you are just being delusional.

According to CNBC, very strict capital controls are coming to Cyprus. These rules will apply even to accounts that contain less than 100,000 euros…

Financial controls are coming. Depositors with less than 100,000 euros may not lose their money outright, but they won’t like the restrictions–no matter how much they have in the bank. Limits on withdrawals, limits on check cashing, and perhaps even outright conversion of checking accounts into fixed term deposits are coming (translation: you don’t have a checking account, you have a bond from the bank).

A lot of people are going to lose a lot of money in Cyprus banks, and a significant percentage of them are going to be Russian.

And as I wrote about the other day, you don’t want to have the Russians mad at you.

According to the Guardian, Moscow is already considering various ways that it might “punish” the EU…

However, with Russian investors having an estimated €30bn (£26bn) deposited in banks on the island, the growing optimism about a deal was accompanied by fears of retaliation from Moscow. Alexander Nekrassov, a former Kremlin adviser, said: “If it is the case that there will be a 25% levy on deposits greater than €100,000 then some Russians will suffer very badly.

“Then, of course, Moscow will be looking for ways to punish the EU. There are a number of large German companies operating in Russia. You could possibly look at freezing assets or taxing assets. The Kremlin is adopting a wait and see policy.”

Could this be the start of a bit of “economic warfare” between east and west?

One thing is for sure – the Russians simply do not allow people to walk all over them.

Meanwhile, things in Cyprus are getting more desperate with each passing day. Because they cannot get money out of the banks, many retail stores find themselves running low on cash. In a few more days many of them may not be able to function at all…

Retailers, facing cash-on-delivery demands from suppliers, warned stocks were running low. “At the moment, supplies will last another two or three days,” said Adamos Hadijadamou, head of Cyprus’s Association of Supermarkets. “We’ll have a problem if this is not resolved by next week.”

But do you know who was able to get their money out in time?

The insiders.

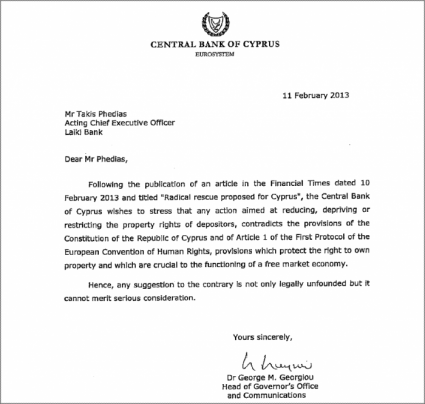

According to the Daily Mail, the President of Cyprus actually warned “close friends” about what was going to happen and told them to get their money out Cyprus…

Cypriot president Nikos Anastasiades ‘warned’ close friends of the financial crisis about to engulf his country so they could move their money abroad, it was claimed on Friday.

Overall, approximately 4.5 billion euros was moved out of Cyprus during the week just before the crisis struck.

Wouldn’t you like to get advance warning like that?

Well, at this point it does not take a genius to figure out what to do about any money that you may have in European banks. The following is from a recent Forbes article by economist Laurence Kotlikoff…

Whatever happens, no one is going to trust or use Cypriot banks. This will shut down the country’s financial highway and flip Cyprus’ economy to a truly awful equilibrium in a replay of our own country’s Great Depression, which was kicked off by the failure of one-in-three U.S. banks.

Cyprus is a small country. Still, the failure of its banks could trigger massive bank runs in Greece. After all, if the European Central Bank is abandoning Cypriot depositors, they may abandon Greek depositors next. A run on Greek banks could then spread to Portugal, Ireland, Spain, and Italy and from there to Belgium and France and, you get the picture, to other countries around the globe, including, drum roll, the U.S. Every bank in each of these countries has made promises they can’t keep were push come to shove, i.e., if all depositors demand their money back immediately.

We’ve seen this movie before. And not just in real life. Every Christmas our tellys show It’s a Wonderful Life in which banker Jimmy Stewart barely saves his small town from economic ruin arising from a banking panic.

Others are being even more blunt with their warnings. For example, Nigel Farage, a member of the European Parliament, is warning everyone to get their money out of southern European banks while they still can…

The appalling events in Cyprus over the course of the past week have surpassed even my direst of predictions.

Even I didn’t think that they would stoop to stealing money from people’s bank accounts. I find that astonishing.

There are 750,000 British people who own properties, or who live, many of them in retirement down in Spain.

Our message to expats now that the EU has crossed this line, must be: Get your money out of there while you’ve still got a chance.

And Martin Sibileau is proclaiming that if you still have an unsecured deposit in a eurozone bank that you should have your head examined…

What are depositors of Euros faced with today? Anything but a clean bet! They don’t know what the expected loss on their capital will be, because it will be decided over a weekend by politicians who don’t even represent them. They don’t really know where their deposits went to and they also ignore what jurisdiction they really belong to. Finally, depositors are paid mere basis points for their trust in the system vs. the 20% p.a. Argentina offered in 2001 (thanks to the zero-interest rate policies of the 21st century). In light of all this, I can only conclude that anyone still having an unsecured deposit in a Euro zone bank should get his/her head examined!

So where should you put your money?

I don’t know that there is anywhere that is 100% safe at this point. But many are pointing to hard assets such as gold and silver. The following is what trends forecaster Gerald Celente had to say during one recent interview…

“People always say to me, ‘Mr. Celente you are always talking about gold. What are you going to do with gold when everything collapses and there is no money?’ Well, let’s say you are a Cypriot and all of the ATM machines are out of money and the banks are closed? Do you think those pieces of silver are going to buy you what you need? Do you think that ounce of gold is going to get you what you want?

That’s the real money. There is no other money. When it all comes down, gold and silver are the only things you have to buy what you need, get what you want, or even get out if you need to.”

I used to tell people that putting their money in U.S. banks was safer than putting it other places because U.S. bank deposits are covered by deposit insurance up to a certain amount.

But now we see that deposit insurance means absolutely nothing. If they decide to “tax” (i.e. steal) your money from your bank accounts they will just go ahead and do it.

So what should we all do?

Personally, I think that not having all of your eggs in one basket is a wise approach. If you have your wealth a bunch of different places and in several different forms, I think that will help.

But as the global financial system falls apart, there will be no such thing as 100% safety. So if you are looking for that you can stop trying.

Our world is becoming a very unstable place, and things are going to get a lot worse. We are all going to have to adjust to this new paradigm and do the best that we can.

The price of oil collapsed by more than 8 percent on Wednesday, and a decision by the European Central Bank has Greece at the precipice of a complete and total financial meltdown. What a difference 24 hours can make. On Tuesday, things really seemed like they were actually starting to get better. The price of oil had rallied by more than 20 percent since last Thursday, things in Europe seemed like they were settling down, and there appeared to be a good deal of optimism about how global financial markets would perform this month. But now fear is back in a big way. Of course nobody should get too caught up in how the markets behave on any single day. The key is to take a longer term point of view. And the fact that the markets have been on such a roller coaster ride over the past few months is a really, really bad sign. When things are calm, markets tend to steadily go up. But when the waters start really getting choppy, that is usually a sign that a big move down in on the horizon. So the huge ups and the huge downs that we have witnessed in recent days are likely an indicator that rough seas are ahead.

The price of oil collapsed by more than 8 percent on Wednesday, and a decision by the European Central Bank has Greece at the precipice of a complete and total financial meltdown. What a difference 24 hours can make. On Tuesday, things really seemed like they were actually starting to get better. The price of oil had rallied by more than 20 percent since last Thursday, things in Europe seemed like they were settling down, and there appeared to be a good deal of optimism about how global financial markets would perform this month. But now fear is back in a big way. Of course nobody should get too caught up in how the markets behave on any single day. The key is to take a longer term point of view. And the fact that the markets have been on such a roller coaster ride over the past few months is a really, really bad sign. When things are calm, markets tend to steadily go up. But when the waters start really getting choppy, that is usually a sign that a big move down in on the horizon. So the huge ups and the huge downs that we have witnessed in recent days are likely an indicator that rough seas are ahead.