It is starting to look a lot like the last financial crisis. Americans are defaulting on their credit cards at a rate that we haven’t seen in more than a decade, and this could have very serious implications for our financial institutions as we move into 2025. Easy credit has enabled many Americans to enjoy lifestyles that are far beyond what they actually deserve, but outrageously high interest rates, absurd penalties and predatory fees have sucked the financial life out of millions of households. The temptation of easy credit has proven to be too much for many Americans to resist, and now a day of reckoning has arrived and it isn’t going to be fun.

It is starting to look a lot like the last financial crisis. Americans are defaulting on their credit cards at a rate that we haven’t seen in more than a decade, and this could have very serious implications for our financial institutions as we move into 2025. Easy credit has enabled many Americans to enjoy lifestyles that are far beyond what they actually deserve, but outrageously high interest rates, absurd penalties and predatory fees have sucked the financial life out of millions of households. The temptation of easy credit has proven to be too much for many Americans to resist, and now a day of reckoning has arrived and it isn’t going to be fun.

It was expected that credit card defaults would continue to rise this year.

But a 50 percent jump is ridiculous…

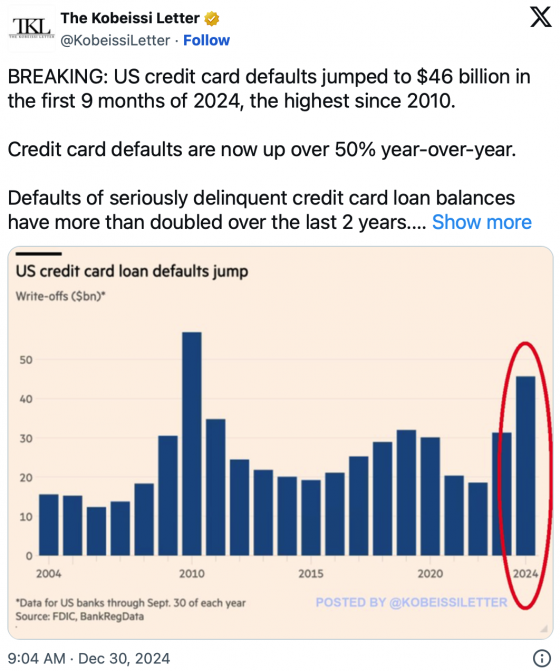

Credit card defaults are at their highest level since 2010 as consumers feel increasingly stretched.

As the Financial Times (FT) reported Sunday (Dec. 29), card lenders wrote off $46 billion in seriously delinquent loans in the first nine months of this year, a 50% jump over 2023. That’s the highest level in 14 years, the report said, citing industry data compiled by BankRegData.

In the last 20 years, there has only been one other year when credit card defaults have reached this level.

This is yet another indication that our economy is rapidly moving in the wrong direction.

Thanks to our seemingly endless cost of living crisis, an increasing number of Americans have been forced to turn to credit card debt just to make ends meet.

At this point, 74.5 percent of all U.S. consumers are carrying at least some credit card debt…

As covered here earlier this month, the share of consumers carrying at least some card debt is pervasive, at 74.5%, per PYMNTS Intelligence research. While that percentage is more or less static across income levels, it leaps to more than 90% for consumers living paycheck to paycheck and having trouble paying their bills.

The research showed that the average outstanding balance among paycheck-to-paycheck cardholders who have issues paying their bills is $7,038, compared to those who live paycheck to paycheck without such difficulties, who had average outstanding balances of $5,766.

This is a nightmare.

Our economy is highly dependent on consumer spending, but now the bottom third of the economic pyramid is “tapped out”…

Mark Zandi, the head of Moody’s Analytics, said, “High-income households are fine, but the bottom third of US consumers are tapped out. Their savings rate right now is zero.”

Credit card debt is one of the most destructive forms of debt that you can accumulate.

In fact, it would be difficult for me to overstate just how devastating credit card debt can be to a family.

If you owe $10,000 on a credit card with a 20 percent interest rate and only make a payment of 300 dollars each month, it will take you more than four years to pay it off.

During that time you will pay $4,718 in interest rate charges in addition to the $10,000 in principal that you are required to pay back.

That does not even account for any penalties or late fees.

Are you starting to get the picture?

The truth is that credit cards are one of the greatest inventions for sucking the wealth out of middle class American families ever invented.

Today, Americans have over a billion credit cards, and they owe over a trillion dollars on those cards.

I just asked Google AI, and I was told that “the combined GDP of the 100 poorest countries is estimated to be around $500 billion”.

So that means that what Americans owe on their credit cards is twice as large as the GDP of the 100 poorest nations on the entire planet combined.

What in the world is wrong with us?

The top 10 credit card issuers in the U.S. control approximately 82 percent of the credit card market.

When we go into credit card debt, we are making them even wealthier.

And that is precisely what they want.

Right now, there are no federal laws that limit the interest rates that credit card companies can charge.

If they want to charge you 30 percent, they can do that.

If they want to charge you 40 percent, they can do that.

And of course they love to hit us with all sorts of fees and penalties as well.

According to Google AI, this is how much revenue some of the largest credit card companies earned in 2022…

American Express: $50.7 billion

Bank of America: $92.4 billion

Capital One: $34.2 billion

Chase: $154.8 billion

Citibank: $101 billion

Discover: $15.2 billion

That is a ton of money.

The higher we push our credit card balances, the richer they become.

The bottom line is that we need to change our behavior.

We work so hard to earn the money that we make.

Why hand that money over to greedy bankers?

Last week, I discussed the fact that our central banking system has been designed to funnel as much wealth as possible to the very top of the pyramid.

The same thing is true for credit cards.

If you are paying 20 or 30 percent interest on a credit card balance every month, you are literally committing financial suicide.

The bankers are getting rich from your hard work, and you need to get out of credit card debt as soon as you can.

Sadly, for many American families it is already too late. It is almost impossible to pay off debt if you don’t have a job and you are about to lose your home. At this moment, many American families find themselves literally being torn apart by financial stress.

Yesterday, I wrote about how homelessness in the U.S. is at an all-time record high.

Today, I am writing about how credit card defaults have risen to the highest level in 14 years.

If you can’t see where all of this is heading, I don’t know what to say.

We are in far more trouble than most people realize, and the outlook for 2025 is not promising at all.

Michael’s new book entitled “Why” is available in paperback and for the Kindle on Amazon.com, and you can subscribe to his Substack newsletter at michaeltsnyder.substack.com.

About the Author: Michael Snyder’s new book entitled “Why” is available in paperback and for the Kindle on Amazon.com. He has also written eight other books that are available on Amazon.com including “Chaos”, “End Times”, “7 Year Apocalypse”, “Lost Prophecies Of The Future Of America”, “The Beginning Of The End”, and “Living A Life That Really Matters”. When you purchase any of Michael’s books you help to support the work that he is doing. You can also get his articles by email as soon as he publishes them by subscribing to his Substack newsletter. Michael has published thousands of articles on The Economic Collapse Blog, End Of The American Dream and The Most Important News, and he always freely and happily allows others to republish those articles on their own websites. These are such troubled times, and people need hope. John 3:16 tells us about the hope that God has given us through Jesus Christ: “For God so loved the world, that he gave his only begotten Son, that whosoever believeth in him should not perish, but have everlasting life.” If you have not already done so, we strongly urge you to invite Jesus Christ to be your Lord and Savior today.

Get prepared for what is ahead by visiting some of our sponsors…

The Jase Case is more than an emergency medication supply. The right meds the moment you need them: https://shorturl.at/gMpOj

Protect your home and vehicle with EMP Shield: https://shorturl.at/Hh2oz

Ready Hour Emergency Food: https://shorturl.at/RB6ul

My Patriot Supply: https://shorturl.at/GhppY

InstaFire: https://shorturl.at/brRN1

AlexaPure: https://shorturl.at/CH23z

Operation Blackout: https://eflow.americablackout.com/2964TZB/7XDN2/

Exodus Effect: https://trk.exodusrevealed.com/2964TZB/225JFQ/

Final Famine: https://trk.finaleagainstfamine.com/2964TZB/BP658/

Genesis Code: https://trk.discovergenesiscode.com/2964TZB/M2GJW/

Final Blackout: https://trk.borderdatareport.com/2964TZB/2N721M/

Last Blackout: https://trk.last-blackout.com/2964TZB/2J2CRS/