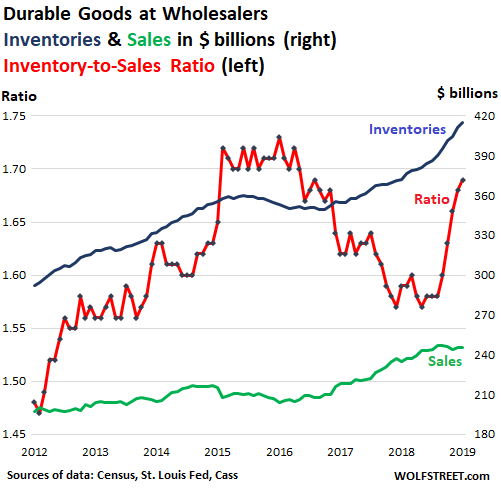

When economic conditions initially begin to slow down, businesses continue to order goods like they normally would but those goods don’t sell as quickly as they previously did. As a result, inventory levels begin to rise, and that is precisely what is happening right now. In fact, the U.S. inventory to sales ratio has risen sharply for five months in a row. This is mirroring the pattern that we witnessed just prior to the financial crisis of 2008, and it is exactly what we would expect to see if a new recession was now beginning. In recent weeks, I have been sharing number after number that indicates that a serious economic slowdown is upon us, and many believe that what is coming will eventually be even worse than what we experienced in 2008.

When economic conditions initially begin to slow down, businesses continue to order goods like they normally would but those goods don’t sell as quickly as they previously did. As a result, inventory levels begin to rise, and that is precisely what is happening right now. In fact, the U.S. inventory to sales ratio has risen sharply for five months in a row. This is mirroring the pattern that we witnessed just prior to the financial crisis of 2008, and it is exactly what we would expect to see if a new recession was now beginning. In recent weeks, I have been sharing number after number that indicates that a serious economic slowdown is upon us, and many believe that what is coming will eventually be even worse than what we experienced in 2008.

And even though I write about this stuff every day, I was stunned by how rapidly inventory levels have been rising recently. The following numbers come from Peter Schiff’s website…

This comes on the heels of the largest gain in wholesale inventories in more than five years in December.

Inventories rose 7.7% from a year ago in January. Meanwhile, sales only rose by 2.7%. Overall, total inventories were $669.9 billion at the end of January, up 1.2% from the revised December level.

The increase in durable goods inventories at the wholesale level was even starker. These inventories were up 11.7% from January a year ago, and are up 17% from January two years ago, hitting $415 billion, the highest ever.

Businesses don’t like to have excess inventory, because carrying excess inventory is expensive and cuts into profits. So they try very hard to manage their inventories efficiently, but if the economy slows down unexpectedly that can catch them off guard…

There are few indications of economic slowing that are more convincing than an unwanted build in inventories — and that apparently is what’s underway in the wholesale sector.

When inventory levels get too high, businesses often start reducing the amount of stuff they are ordering from manufacturers.

So we would expect the numbers to indicate that manufacturing output is down, and that is precisely what we have witnessed over the last couple of months…

U.S. manufacturing output fell for a second straight month in February and factory activity in New York state hit nearly a two-year low this month, offering further evidence of a sharp slowdown in economic growth early in the first quarter.

If manufacturers are making and sending less stuff to businesses, and if businesses are selling less stuff to their customers, then we would expect to see less stuff moved around the U.S. by truck, rail and air.

And wouldn’t you know it, the numbers also tell us that this has been happening too. The following comes from Wolf Richter…

Now it’s the third month in a row, and the red flag is getting more visible and a little harder to ignore about the goods-based economy: Freight shipment volume in the US across all modes of transportation – truck, rail, air, and barge – in February fell 2.1% from February a year ago, according to the Cass Freight Index, released today. The three months in a row of year-over-year declines are the first such declines since the transportation recession of 2015 and 2016.

So there you have it. Anyone that tries to tell you that the U.S. economy is “booming” is simply not being accurate.

And when you throw in the fact that we just witnessed one of the worst disasters for U.S. agriculture in all of U.S. history, it is easy to understand why the economic outlook for the remainder of 2019 is rather bleak. One agribusiness company just announced that it will have “a negative pretax operating profit impact of $50 million to $60 million for the first quarter” as a result of all the flooding…

Already suffering from low crop prices and the U.S.-China trade war, Mother Nature has delivered yet another blow to the beleaguered American farmer. Growers in the heartland this year have seen arctic cold blasts, been blanketed by snow and just in the last week were inundated by floods. Archer-Daniels-Midland Co., one of the world’s biggest agribusinesses, said Monday that it expects weather disruptions to have a negative pretax operating profit impact of $50 million to $60 million for the first quarter.

Korth said he fears the worst for local farmers, citing a friend who lost 85 cows to flooding and another who sells seeds and has already seen order cancellations.

“It’s going to put a lot of people out of business,” Korth said. “It’s just a terrible deal.”

Unfortunately, the flooding in the middle portion of the country is just getting started. According to the National Weather Service, we are going to see more catastrophic flooding for the next two months.

As you can see, the elements for a “perfect storm” are definitely coming together, and I encourage everyone to get prepared for rough times ahead.

But many people are not that concerned about a new crisis, because they remember that global central banks were able to pull us out of the fire last time around.

Unfortunately, they may not be able to do it this time. Just consider the words of the deputy director of the IMF…

Major financial institutions may be powerless to prevent the next global economic downturn from tuning into a full-blow recession, the International Monetary Fund has warned.

In a speech on the future of the eurozone, the IMF’s deputy director David Lipton, warned of the depleted power of central banks and governments to combat another sharp economic shock.

“The bottom line is this: the tools used to confront the global financial crisis may not be available or may not be as potent next time” he said.

But I am sure that global central banks will try to patch the system back together again, and at certain moments it may even look like they are having some success.

In the end, however, they will not be able to stop the “Bubble To End All Bubbles” from completely bursting.

It has taken decades of exceedingly foolish decisions to get us to this point, and there is simply no way that we can avoid the day of reckoning that is coming.

About the author: Michael Snyder is a nationally-syndicated writer, media personality and political activist. He is the author of four books including Get Prepared Now, The Beginning Of The End and Living A Life That Really Matters. His articles are originally published on The Economic Collapse Blog, End Of The American Dream and The Most Important News. From there, his articles are republished on dozens of other prominent websites. If you would like to republish his articles, please feel free to do so. The more people that see this information the better, and we need to wake more people up while there is still time.

About the author: Michael Snyder is a nationally-syndicated writer, media personality and political activist. He is the author of four books including Get Prepared Now, The Beginning Of The End and Living A Life That Really Matters. His articles are originally published on The Economic Collapse Blog, End Of The American Dream and The Most Important News. From there, his articles are republished on dozens of other prominent websites. If you would like to republish his articles, please feel free to do so. The more people that see this information the better, and we need to wake more people up while there is still time.

The long-term trends that are gutting the U.S. economy continue to get even worse. As you will see below, our goods trade deficit with the rest of the world hit a brand new record high in 2018, and most Americans simply do not understand why this is such a massive problem. Every year, we buy far more from the rest of the world than they buy from us, and that means that the amount of money going out of the country far surpasses the amount that is coming in. This constant outflow of cash is one of the reasons why we are unable to pay our bills, and so we have to keep begging the rest of the world to lend us our money back. Needless to say, this is one of the big factors that has fueled

The long-term trends that are gutting the U.S. economy continue to get even worse. As you will see below, our goods trade deficit with the rest of the world hit a brand new record high in 2018, and most Americans simply do not understand why this is such a massive problem. Every year, we buy far more from the rest of the world than they buy from us, and that means that the amount of money going out of the country far surpasses the amount that is coming in. This constant outflow of cash is one of the reasons why we are unable to pay our bills, and so we have to keep begging the rest of the world to lend us our money back. Needless to say, this is one of the big factors that has fueled

{kind=link}

{kind=link}