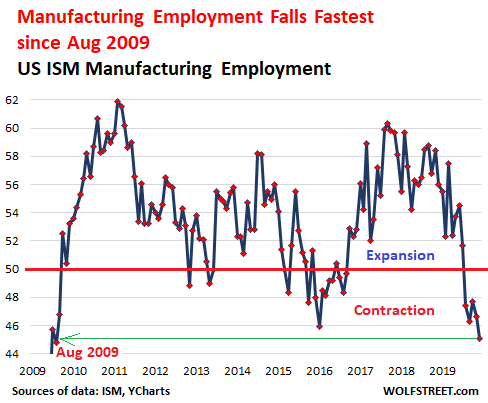

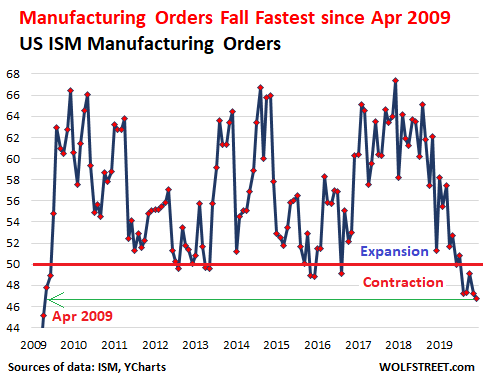

Even though economic conditions were absolutely awful, during the month of June the mainstream media kept insisting that the U.S. economy was “recovering” and the stock market kept surging on every hint of good news. But now the “economic recovery” narrative is completely dead, because the numbers clearly show that the U.S. economy is rapidly moving in the wrong direction. On Thursday, the Labor Department announced that another 1.416 million Americans filed new claims for unemployment benefits last week. Prior to this year, the all-time record for a single week was just 695,000, and so we are talking about a level of unemployment that is absolutely catastrophic. But what is really alarming many analysts is that the number for last week was quite a bit higher than the number for the week before. Many states are rolling out new restrictions as the number of confirmed COVID-19 cases continues to surge, and this is having a huge impact on economic activity. For months I have been warning that fear of COVID-19 would prevent economic activity from returning to normal levels for the foreseeable future, and that is precisely what has happened.

Even though economic conditions were absolutely awful, during the month of June the mainstream media kept insisting that the U.S. economy was “recovering” and the stock market kept surging on every hint of good news. But now the “economic recovery” narrative is completely dead, because the numbers clearly show that the U.S. economy is rapidly moving in the wrong direction. On Thursday, the Labor Department announced that another 1.416 million Americans filed new claims for unemployment benefits last week. Prior to this year, the all-time record for a single week was just 695,000, and so we are talking about a level of unemployment that is absolutely catastrophic. But what is really alarming many analysts is that the number for last week was quite a bit higher than the number for the week before. Many states are rolling out new restrictions as the number of confirmed COVID-19 cases continues to surge, and this is having a huge impact on economic activity. For months I have been warning that fear of COVID-19 would prevent economic activity from returning to normal levels for the foreseeable future, and that is precisely what has happened.

Overall, more than 52 million Americans have filed new claims for unemployment benefits over the past 18 weeks, and that makes this the biggest spike in unemployment in U.S. history by a very wide margin.

In fact, this dwarfs all previous spikes by so much that the others are not even worth mentioning.

Of course it isn’t just the employment numbers that are depressingly bad. According to Jefferies, in late June 19 percent of all U.S. small businesses were closed, but now that number has risen to 24.5 percent…

As of Sunday, 24.5% of small businesses in the United States were closed, according to Jefferies. That is worse than late June, when only 19% were closed. Jefferies pointed to “particular weakness in COVID hot spots” and noted that small business employment had dropped to levels unseen since the end of May.

Just think about that number for a minute.

Nearly a quarter of all small businesses in the entire country are closed.

And the really bad news is that many of them will never end up reopening.

At the beginning of the pandemic, I received a lot of criticism for stating that many of the small businesses that were shutting down at that time would never open again, but over the long-term the numbers have shown that I was correct.

In fact, Yelp says that a whopping 60 percent of the restaurants that were initially listed as “temporarily closed” on their site are now classified as permanently closed…

It’s tough out there for restaurants and other small businesses.

Yelp’s Economic Average report out Wednesday shows exactly how tough: 60 percent of the 26,160 temporarily closed restaurants on the business review site as of July are now permanently shut. Temporary closures are dropping, and permanent shutdowns are increasing.

Fear of COVID-19 is going to cause a large portion of the population to continue to avoid restaurants for as long as this pandemic persists, and it is becoming clear that it is likely to persist for a long time to come.

We are going to lose so many small and independent places to eat. Many of the big corporate chains that have very deep pockets will survive, at least for a while, but there is simply no replacing what small and independent restaurants mean to our communities.

Bars and clubs are being hit extremely hard as well. According to Yelp, 44 percent of the bars and clubs on their site that were initially listed as “temporarily closed” have now been shut down on a permanent basis…

Bars and clubs are also closing forever at high rates: 44 percent (as of July) of 5,454 temporarily shuttered bars and other nightlife establishments are shut for good.

Other sectors of the economy are doing relatively better, but the overall outlook for small businesses in America is exceedingly bleak.

In New York City, it is being projected that one-third of all small businesses will never be able to open again…

As many as 76,000 small businesses in New York City – a third of the 230,000 citywide – may never reopen after forced to close during the COVID-19 lockdown, business leaders have warned.

The Partnership for New York City, a not-for-profit organization that connects business leaders with local government, predicted that 76,000 small businesses will never be able to reopen in a report produced by 14 consulting firms.

I know that number is hard to believe, but this is actually happening.

Our politicians want to encourage people “to go back to work”, but for millions upon millions of Americans the jobs that they once had are gone forever.

Air travel is another industry that is being absolutely devastated by this pandemic. After a modest bounce in June, the number of air passengers is starting to fall again…

The resurgence of coronavirus infections is derailing the travel industry’s modest recovery. The number of air passengers processed through TSA security lines fell during the week ended July 20, compared with the prior week, according to Bank of America. This metric is down more than 70% from a year ago.

United (UAL) CEO Scott Kirby told CNBC on Wednesday that the airline doesn’t “expect to get anywhere close to normal until there’s a vaccine that’s been widely distributed to a large portion of the population.”

All of the numbers that I have shared in this article tell us that we are in an economic depression.

Many had hoped that this economic downturn would be short-lived and that a “V-shaped recovery” would commence once the coronavirus lockdowns were lifted.

But instead a resurgence of cases has caused new restrictions to be implemented, and economic activity is slowing down again.

The bottom line is that all of us need to get prepared to weather a long-term economic storm that is going to be incredibly painful.

The last recession was bad, but it isn’t even worth comparing to the times that we are entering now. All of our lives are being turned upside down, and a lot of people are not going to be able to handle what comes next.

About the Author: I am a voice crying out for change in a society that generally seems content to stay asleep. My name is Michael Snyder and I am the publisher of The Economic Collapse Blog, End Of The American Dream and The Most Important News, and the articles that I publish on those sites are republished on dozens of other prominent websites all over the globe. I have written four books that are available on Amazon.com including The Beginning Of The End, Get Prepared Now, and Living A Life That Really Matters. (#CommissionsEarned) By purchasing those books you help to support my work. I always freely and happily allow others to republish my articles on their own websites, but due to government regulations I need those that republish my articles to include this “About the Author” section with each article. In order to comply with those government regulations, I need to tell you that the controversial opinions in this article are mine alone and do not necessarily reflect the views of the websites where my work is republished. The material contained in this article is for general information purposes only, and readers should consult licensed professionals before making any legal, business, financial or health decisions. Those responding to this article by making comments are solely responsible for their viewpoints, and those viewpoints do not necessarily represent the viewpoints of Michael Snyder or the operators of the websites where my work is republished. I encourage you to follow me on social media on Facebook and Twitter, and any way that you can share these articles with others is a great help. During these very challenging times, people will need hope more than ever before, and it is our goal to share the gospel of Jesus Christ with as many people as we possibly can.

As America slowly but surely shuts down from coast to coast, everyone is acknowledging the fact that we are heading into a very serious economic downturn. Originally, many experts were warning that this coronavirus pandemic could spark a recession, but now some are actually starting to use the “d” word. Yesterday, I wrote about the government planning document that envisions

As America slowly but surely shuts down from coast to coast, everyone is acknowledging the fact that we are heading into a very serious economic downturn. Originally, many experts were warning that this coronavirus pandemic could spark a recession, but now some are actually starting to use the “d” word. Yesterday, I wrote about the government planning document that envisions

{kind=link}

{kind=link}