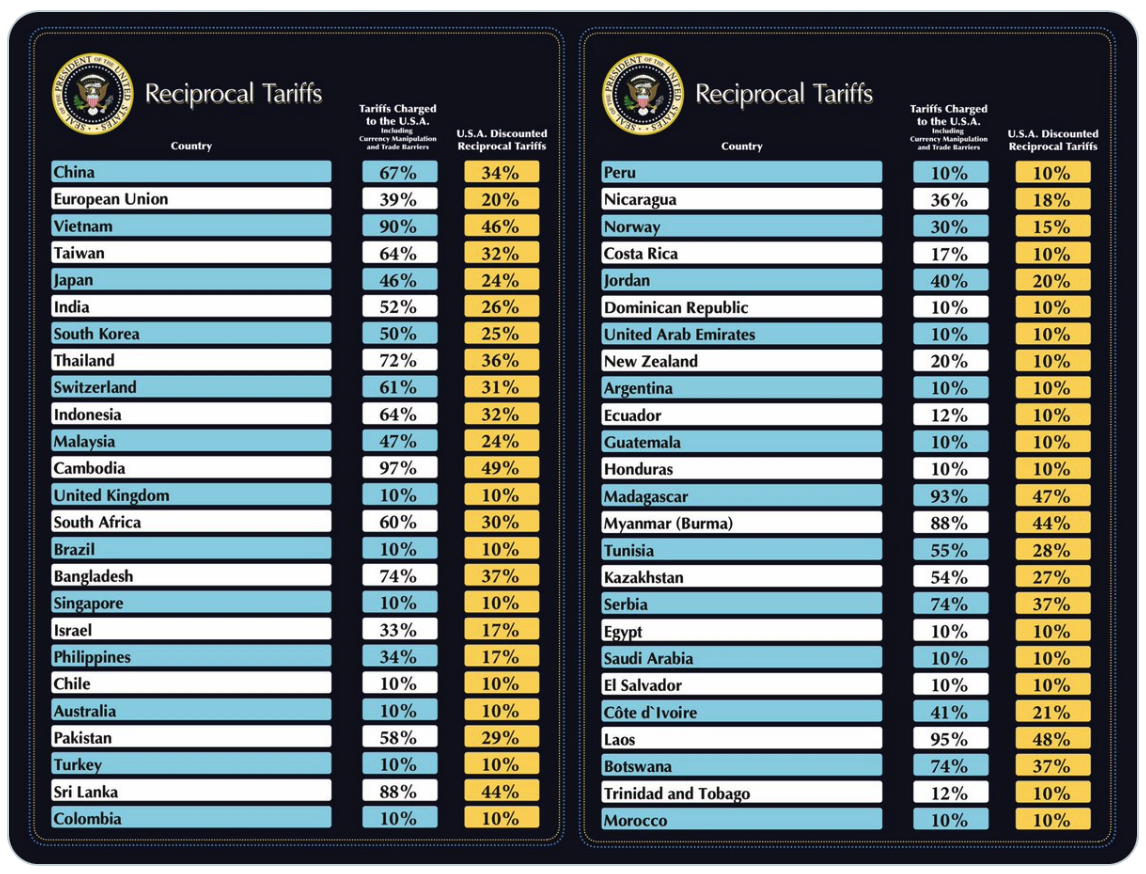

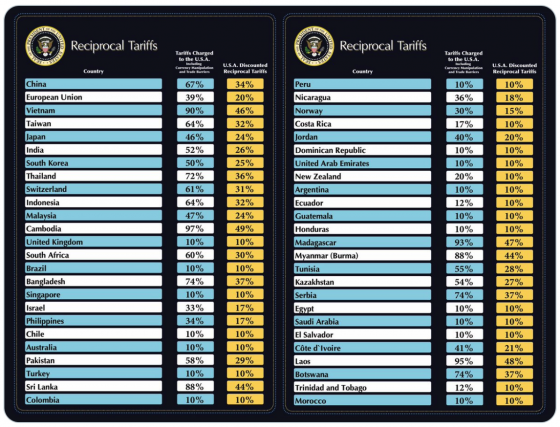

Well, isn’t this fun? News that President Trump had decided to pause some of the tariffs that he recently unveiled for 90 days sent stock prices soaring. The Dow Jones Industrial Average was up more than 2,900 points on Wednesday, and that is very good news. But not that much has actually changed, and the global trade war is still officially on. In fact, President Trump just hiked the tariff rate on Chinese imports to 125 percent… (Read More...)

Well, isn’t this fun? News that President Trump had decided to pause some of the tariffs that he recently unveiled for 90 days sent stock prices soaring. The Dow Jones Industrial Average was up more than 2,900 points on Wednesday, and that is very good news. But not that much has actually changed, and the global trade war is still officially on. In fact, President Trump just hiked the tariff rate on Chinese imports to 125 percent… (Read More...)

Trump’s Economic War Against The Communist Chinese Empire Just Went Nuclear