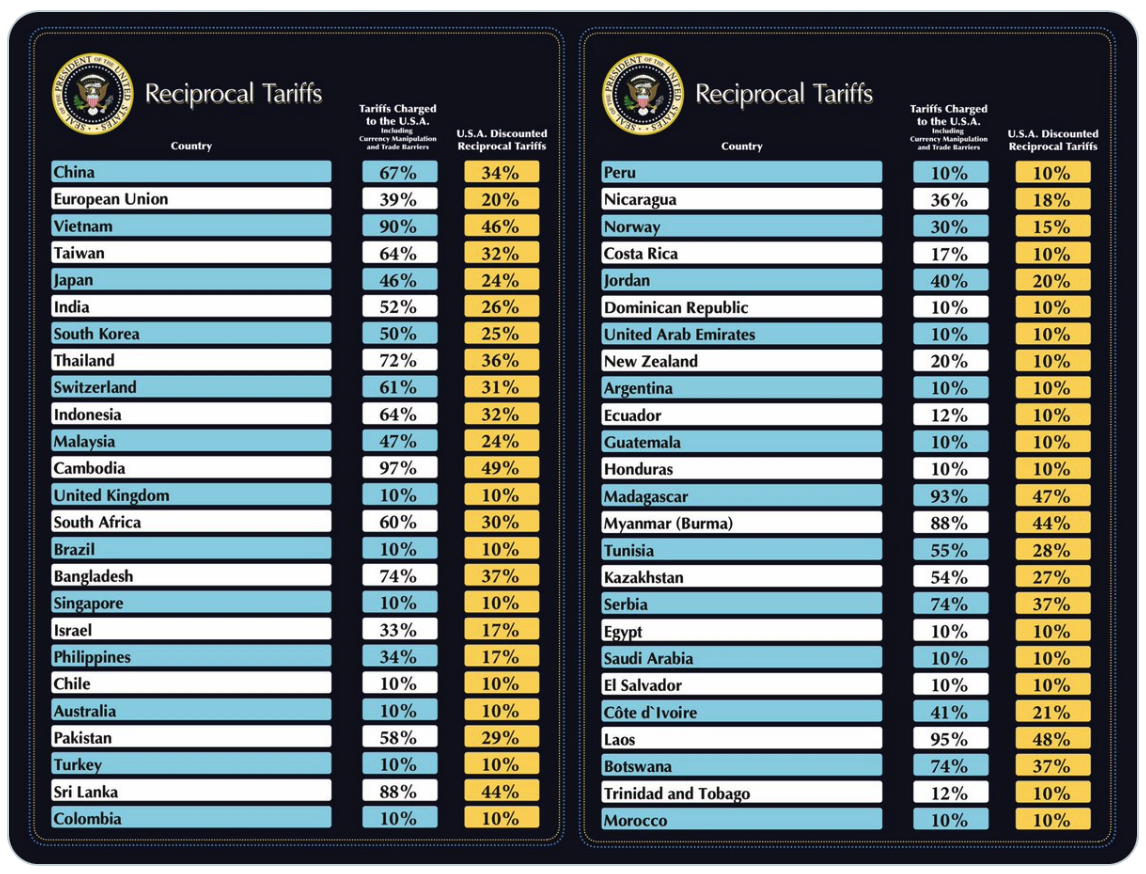

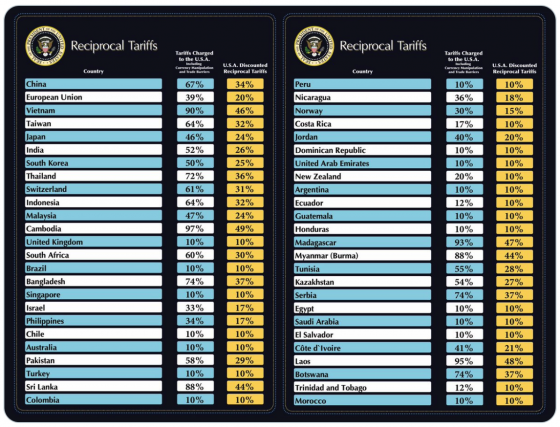

I am trying to find the words to describe the economic carnage that we are witnessing right now. Even before President Trump unveiled his new tariffs, the U.S. economy was rapidly heading in the wrong direction, layoffs were soaring, and stock prices were steadily falling. But now it is as if enormous amounts of gasoline have been suddenly poured on the fire. Trump’s tariffs have caused a massive wave of panic on Wall Street, and the Dow Jones Industrial Average was down 1,679 points on Thursday. That was the biggest decline that we have seen since the early days of the pandemic in 2020. The S&P 500 and the Nasdaq also experienced the largest declines that we have seen since 2020. Everywhere you look there is carnage. The small-cap Russell 2000 index has now fallen more than 20 percent from the peak, and that officially puts it in bear market territory. What we are witnessing is absolutely horrifying. (Read More...)

I am trying to find the words to describe the economic carnage that we are witnessing right now. Even before President Trump unveiled his new tariffs, the U.S. economy was rapidly heading in the wrong direction, layoffs were soaring, and stock prices were steadily falling. But now it is as if enormous amounts of gasoline have been suddenly poured on the fire. Trump’s tariffs have caused a massive wave of panic on Wall Street, and the Dow Jones Industrial Average was down 1,679 points on Thursday. That was the biggest decline that we have seen since the early days of the pandemic in 2020. The S&P 500 and the Nasdaq also experienced the largest declines that we have seen since 2020. Everywhere you look there is carnage. The small-cap Russell 2000 index has now fallen more than 20 percent from the peak, and that officially puts it in bear market territory. What we are witnessing is absolutely horrifying. (Read More...)

Wake Up! The Stock Market Is Crashing, Layoffs Have Surged More Than 200 Percent, And We Are Being Warned A Depression Is Coming