The world is now 188 trillion dollars in debt, and that number continues to grow rapidly each year. It is a form of enslavement that is deeply insidious, because most of those living on the planet do not even understand how the system works, and even if they did most of them would have absolutely no hope of ever getting free from it. The borrower is the servant of the lender, and the global financial system is designed to funnel as much wealth to the top 0.1% as possible. Of course throughout human history there has always been slavery, and the primary motivation for having slaves is to extract an economic benefit from those that are enslaved. And even though most of us don’t like to think of ourselves as “slaves” today, the truth is that the global elite are extracting more wealth from all of us than ever before. So much of our labor is going to make them wealthy, and yet most people don’t even realize what is happening.

The world is now 188 trillion dollars in debt, and that number continues to grow rapidly each year. It is a form of enslavement that is deeply insidious, because most of those living on the planet do not even understand how the system works, and even if they did most of them would have absolutely no hope of ever getting free from it. The borrower is the servant of the lender, and the global financial system is designed to funnel as much wealth to the top 0.1% as possible. Of course throughout human history there has always been slavery, and the primary motivation for having slaves is to extract an economic benefit from those that are enslaved. And even though most of us don’t like to think of ourselves as “slaves” today, the truth is that the global elite are extracting more wealth from all of us than ever before. So much of our labor is going to make them wealthy, and yet most people don’t even realize what is happening.

Let’s start with a very simple example to help illustrate this.

When you go into credit card debt and you only make small payments each month, you can easily end up paying back more than double the amount of money that you originally borrowed.

So where does all that money go?

Well, of course it goes to the financial institution that you got your credit card from, and in turn that financial institution is owned by the global elite.

In essence, you willingly became a debt slave when you chose to go into credit card debt, and the hard work that it took to earn enough money to pay back that debt with interest ended up enriching others.

On a much larger scale, the same thing is happening to entire nations.

Today, the United States government is nearly 23 trillion dollars in debt. In essence, we have been collectively enslaved, and we have been obligated to pay back all of that money with interest. Of course at this point it is literally impossible for us to ever pay back all that debt, and every year we add another trillion dollars or so to the balance. The global elite are now extracting more than 500 billion dollars in interest from this debt on an annual basis, and it is expected that number will greatly escalate in the years ahead.

It is not an accident that the Federal Reserve and the federal income tax were both instituted in 1913. The Federal Reserve system was designed to create an endless debt spiral that would get the federal government in as much debt as possible, and since that time the size of our national debt has gotten more than 7000 times larger. And the federal income tax was needed as the mechanism through which our wealth is transferred to the government to service all of this debt.

It is truly a deeply, deeply insidious system, and the American people should refuse to back any politician that does not favor shutting it down, but at this point this isn’t even a major political issue in our nation.

And of course the United States is far from alone. Even though we can’t get the whole world to agree on much of anything, somehow virtually the entire planet has been convinced that debt-based central banking is the way to go.

In fact, at this point 99.9 percent of the population of the world lives in a country that has a central bank.

According to Wikipedia, there are only 9 very small nations that do not have a central bank at this point…

-Andorra

-Isle of Man

-Monaco

-Nauru

-Kiribati

-Tuvalu

-Palau

-Marshall Islands

-Federated States of Micronesia

If you combine the populations of all of those 9 nations together, it comes to much less than 0.1% of the total global population.

Do you think that this is just a coincidence?

The global elite do not want humanity to be free. They want us to be in as much debt as possible so that we can make them richer.

When you realize how badly the game has been rigged, then a lot of things start to make a whole lot more sense.

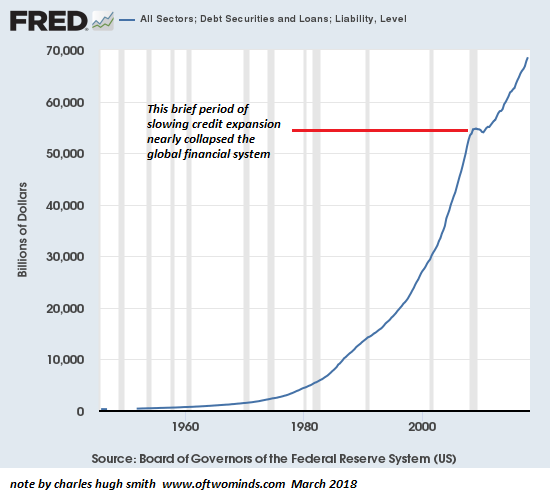

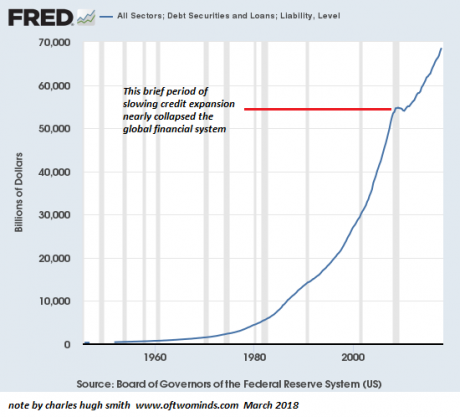

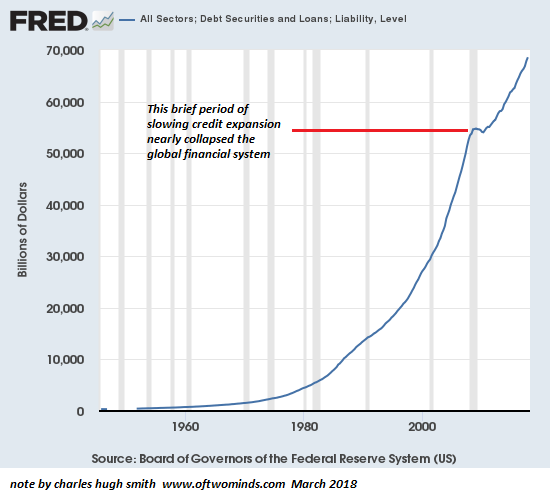

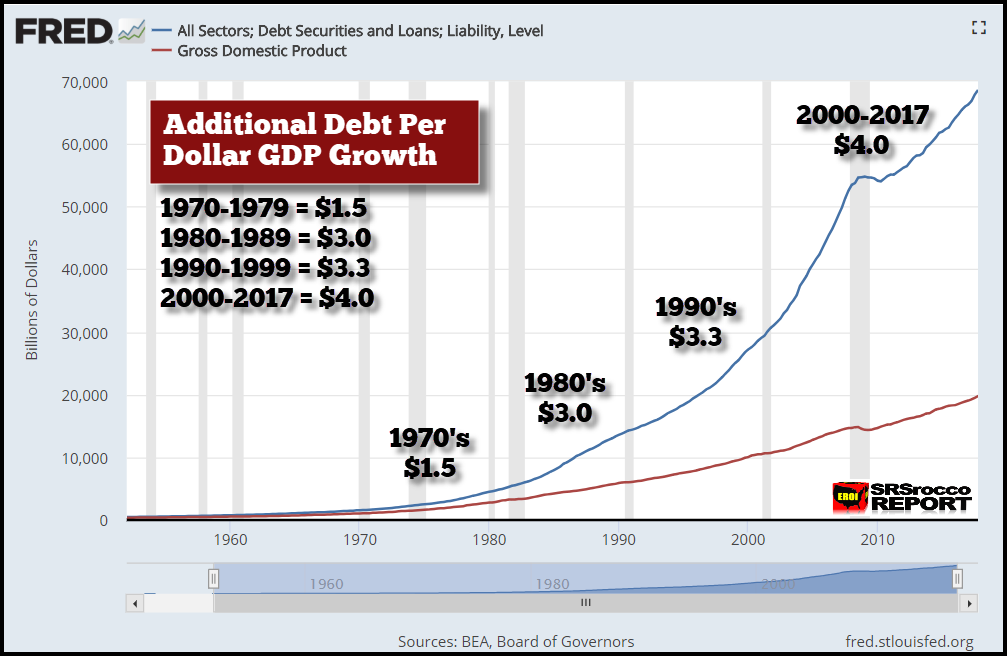

For example, for those that understand how the system works it is certainly not surprising that the total amount of debt in the world has hit a new all-time record high of 188 trillion dollars…

The global debt load has surged to a new all-time record equivalent to more than double the world’s economic output, IMF chief Kristalina Georgieva warned Thursday.

While private sector borrowing accounts for the vast majority of the total, the rise puts governments and individuals at risk if the economy slows, she said.

“Global debt — both public and private — has reached an all-time high of $188 trillion. This amounts to about 230 percent of world output,” Georgieva said in a speech to open a two-day conference on debt.

That number has risen by 24 trillion dollars since 2016, and it is the biggest debt bubble that the world has ever seen by a very wide margin.

Of course at some point this debt bubble is going to burst in a global disaster of epic proportions, but meanwhile the global elite are going to continue to milk all of us for as long as they possibly can.

Here in the United States, we have been on the greatest debt binge in the history of our nation since the last financial crisis. U.S. government debt has more than doubled, state and local government debt has ballooned to ridiculous proportions in much of the nation, corporate debt has doubled, student loan debt has more than doubled, auto loan debt just keeps hitting new record highs, and U.S. consumers are now 14 trillion dollars in debt.

Our mountain of debt has become so colossal that the only way to keep the game going is to borrow even more money, but by borrowing more money we make our enslavement even worse.

Meanwhile, those that are holding our debt just continue to live the high life as they laugh all the way to the bank.

About the Author: I am a voice crying out for change in a society that generally seems content to stay asleep. My name is Michael Snyder and I am the publisher of The Economic Collapse Blog, End Of The American Dream and The Most Important News, and the articles that I publish on those sites are republished on dozens of other prominent websites all over the globe. I have written four books that are available on Amazon.com including The Beginning Of The End, Get Prepared Now, and Living A Life That Really Matters. (#CommissionsEarned) By purchasing those books you help to support my work. I always freely and happily allow others to republish my articles on their own websites, but due to government regulations I need those that republish my articles to include this “About the Author” section with each article. In order to comply with those government regulations, I need to tell you that the controversial opinions in this article are mine alone and do not necessarily reflect the views of the websites where my work is republished. This article may contain opinions on political matters, but it is not intended to promote the candidacy of any particular political candidate. The material contained in this article is for general information purposes only, and readers should consult licensed professionals before making any legal, business, financial or health decisions. Those responding to this article by making comments are solely responsible for their viewpoints, and those viewpoints do not necessarily represent the viewpoints of Michael Snyder or the operators of the websites where my work is republished. I encourage you to follow me on social media on Facebook and Twitter, and any way that you can share these articles with others is a great help.

{kind=link}

{kind=link}