The election of Donald Trump has sent shockwaves through the U.S. economy and the U.S. financial system. Since November 8th, the Dow has hit a brand new all-time record high, the U.S. dollar has strengthened greatly, and bank stocks are way up. But not all of the economic news is good news. Unlike stocks, bonds have reacted very negatively to Trump’s election victory. The past week has been an absolute bloodbath for bond traders, and as you will see below this is going to have dramatic implications for all U.S. consumers moving forward.

The election of Donald Trump has sent shockwaves through the U.S. economy and the U.S. financial system. Since November 8th, the Dow has hit a brand new all-time record high, the U.S. dollar has strengthened greatly, and bank stocks are way up. But not all of the economic news is good news. Unlike stocks, bonds have reacted very negatively to Trump’s election victory. The past week has been an absolute bloodbath for bond traders, and as you will see below this is going to have dramatic implications for all U.S. consumers moving forward.

Over just a two day period, more than a trillion dollars was wiped out as bond yields spiked all over the globe. As CNN has noted, this type of “violent reaction” in the bond market has only happened three other times within the past ten years…

The rate on 10-year Treasury notes has surged to 2.3%, from 1.77% before the election. Last week’s spike in Treasury rates was so big, that it had only happened three times before in the last decade.

BlackRock’s Russ Koesterich called it a “violent reaction.”

The move stands to have broad repercussions for all Americans. Not only will the U.S. government have to pay more to borrow money, but mortgage rates and car loan costs should also rise. That’s because Treasuries are used as the benchmark for many other forms of credit.

As interest rates rise, virtually everyone in our society is going to feel the pain.

Those that need an auto loan in order to purchase a vehicle are going to find that loan payments are significantly higher than they were before.

Credit card rates will also go up, and those just getting out of school will discover that their student loan payments are even more suffocating.

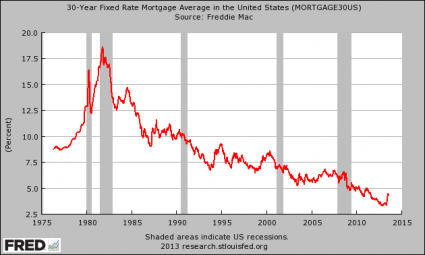

But the biggest impact will be felt in the housing market. The average rate on a 30-year fixed mortgage just hit the psychologically-important 4 percent barrier, and that could mean big trouble for the housing market in 2017…

The average contract rate on the popular 30-year fixed mortgage hit 4 percent, according to Mortgage News Daily, a level most didn’t expect to see until the middle of next year. Rates have now moved nearly a half a percentage point higher since Donald Trump was elected president.

“The situation on the ground is panicked. Damage control,” said Matthew Graham, chief operating officer of Mortgage News Daily. “People were trying to lock loans quickly last week and are now facing a tough choice to lock today or hope for a bounce. Many hoped for a bounce last week heading into the long weekend and we obviously didn’t get it.”

Rising interest rates was one of the key factors that precipitated the financial crisis of 2008, and many fear that it could happen again.

And without a doubt, this rise in rates is going to affect the affordability of homes that are already on the market…

“If you’re going to buy a house and your mortgage payment went up by $200 or $300, you may buy a smaller house. There’s impact on interest rate sensitive sectors, like autos and housing, and also corporate bonds themselves, where financial engineering has helped juice up the equity market,” said George Goncalves, head of rate strategy at Nomura.

In addition, rising rates will make it more difficult for those with adjustable rate mortgages to keep their homes. Foreclosure activity was already up 27 percent during the month of October, and many are projecting that we could see another giant spike in foreclosures during the months ahead that is similar to what we saw during the last financial crisis.

Many Trump supporters don’t really care what the rest of the world thinks of our new president, but this is an area where what the rest of the world thinks really, really matters.

The truth is that the rest of the planet is not all too fond of Trump, and if that makes them a lot less eager to lend us money that is a major problem.

The only way that we can maintain our massively inflated debt-fueled standard of living is to continue to borrow gigantic mountains of money from the rest of the world at ultra-low interest rates.

If the rest of the world starts demanding higher rates of return now that Trump is president, we are going to experience economic pain on a scale that most Americans don’t believe is possible.

One of our big lenders has been China, and right now they are deeply concerned about what a Trump presidency might mean. Trump has talked very tough about trade with China, and the Chinese are gearing up for a major trade war. The following comes from CNBC…

During his election campaign this year, Trump spoke of a 45 percent import tariff on all Chinese goods while failing to outline how it would work. Should any such policy come into effect, China will take a “tit-for-tat approach”, according to an opinion piece in the Global Times, a newspaper backed by the Communist party.

“A batch of Boeing orders will be replaced by Airbus. U.S. auto and iPhone sales in China will suffer a setback, and U.S. soybean and maize imports will be halted. China can also limit the number of Chinese students studying in the U.S.,” the Global Times article read.

Most Trump supporters assume that since Trump has been a very successful businessman that he will be able to strengthen the U.S. economy.

But it isn’t that simple.

The only reason we are able to live the way that we live today is because we have been able to borrow trillions upon trillions of dollars at irrationally low interest rates.

The moment the rest of the world decides that they are not going to loan us money at irrationally low interest rates any longer the game is over, and it won’t really matter who is in the White House at that point.

So watch interest rates very carefully. If they keep going up, it is inevitable that a major economic slowdown will follow no matter what economic policies the new Trump administration implements.