A conference committee has been merging the tax bills that were passed by the House of Representatives and the Senate, and even though we could still see some minor changes, it looks like the major parameters of the final bill have now been agreed upon. The final bill will be known as the Tax Cuts and Jobs Act, and we are being told that it will be one of the largest tax cuts in U.S. history. Unfortunately, the impact on our tax bills will be relatively minor, but at least it is a step in the right direction. The following summary of the major provisions in the final bill comes from AOL…

A conference committee has been merging the tax bills that were passed by the House of Representatives and the Senate, and even though we could still see some minor changes, it looks like the major parameters of the final bill have now been agreed upon. The final bill will be known as the Tax Cuts and Jobs Act, and we are being told that it will be one of the largest tax cuts in U.S. history. Unfortunately, the impact on our tax bills will be relatively minor, but at least it is a step in the right direction. The following summary of the major provisions in the final bill comes from AOL…

- A less generous corporate rate cut: Republicans may cut the corporate rate to 21% from the current federal rate of 35%, instead of the 20% proposed in both the house and Senate bills. The new rate would start in 2018.

- A lower top individual tax rate: The top individual bracket would drop to 37% instead of the 38.5% proposed in the Senate bill. It would still be down from the current 39.6%.

- Keep the estate tax, but raise the threshold to qualify: Instead of phasing out the estate tax over time, like the House bill, the compromise bill would instead simply increase the threshold for an estate to qualify — from $5.6 million to around $11 million. That aligns with the Senate bill.

- Repeal the corporate alternative minimum tax (AMT): The corporate AMT in the Senate bill was a sore spot for many companies because it would have negated the effects of many popular deductions and credits, like the research and development credit.

The reduction in the corporate tax rate is probably the most important provision in this tax overhaul package. For decades, the United States has had a much higher corporate tax rate than much of the rest of the world, and this has given large corporations an incentive to locate operations elsewhere. By making the corporate tax rate more competitive with everyone else around the globe, it is hoped that this will mean more good jobs for American workers.

This bill also reduces individual tax rates, but not by that much. So you will notice a reduction in your tax bill, but don’t expect anything “game changing” in nature.

In addition, this bill will eliminate the Obamacare individual mandate. This is something that should have been done back in January, and I am very happy that Congress is finally getting it done.

It is anticipated that both the House and the Senate will vote on the final version of this tax bill next week.

Sadly, it is not a slam dunk that this bill will actually get through the Senate.

Senator Bob Corker voted against the original Senate bill, and he may vote against this version too.

Ron Johnson of Wisconsin and Susan Collins of Maine have also expressed reservations about this bill, and it is unclear how they will vote at this point.

And let us not forget that Senator John McCain’s health is rapidly failing. Hopefully he would be present for any vote, but there is no guarantee that will happen.

In the end, Republicans can only lose two votes in the Senate, and so this is going to come down to the wire.

But President Trump is quite optimistic that this bill will succeed, and he says that it will “breathe new life into the American economy”…

“Our tax cuts will break down — and they’ll break it down fast — all forms of government and all forms of government barriers and breathe new life into the American economy,” Trump said.

“They will unleash the American people, they will tear down the constraints on discovery, innovation and creation, and they will restore the hopes and dreams of the American family. Millions of middle class families will win under our plan.”

Of course even if this bill passes, our tax code will still be a complete and utter nightmare.

The tax code will still be over two million words, and the regulations will still be more than seven million words. Our system will still greatly favor those that can hire accountants and tax attorneys to find every conceivable loophole possible, and it will still be a tremendous burden on the middle class.

If I am elected to Congress, I am going to fight to completely abolish the IRS and the income tax. As I travel around Idaho and speak to groups, many are extremely receptive to these proposals, but they wonder how we would fund the government without an income tax.

Well, the truth is that the individual income tax only accounts for about 46 percent of all federal revenue, so we could definitely eliminate the individual income tax but we would also have to dramatically reduce the size of the federal government at the same time.

And we have a historical precedent for what this would look like.

Between 1872 and 1913 there was no federal income tax, and it was the best period of economic growth in U.S. history.

Of course the Democrats are not just going to roll over and allow us to cut the size of the federal government in half, so in the short-term we can focus on some other solutions. A flat tax or a fair tax would both be far superior to the system that we have today, and there are some very good proposals already out there that just need to be implemented.

I once spent an entire year studying our tax code, and I still shudder when I think about those 12 months. Our tax code is a complete and utter abomination, and while I applaud Congress for trying to “simplify” it, the truth is that this bill that is about to be passed won’t make that much of a difference.

We need to fundamentally change the way that we fund government in this nation, and that is why I want to completely abolish the income tax. The system that we have right now is simply not fixable, and we should not pretend that any “tax reform bill” is going to solve our problems.

Michael Snyder is a Republican candidate for Congress in Idaho’s First Congressional District, and you can learn how you can get involved in the campaign on his official website. His new book entitled “Living A Life That Really Matters” is available in paperback and for the Kindle on Amazon.com.

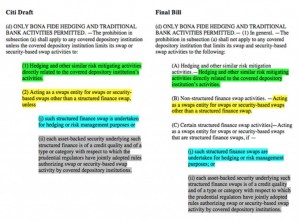

Are you ready for mass chaos in Washington? There are lobbyists for just about every cause that you can possibly imagine, and they are always working hard to influence members of Congress on their particular issues. But when you are talking about a major tax reform bill, that is something that virtually every single lobbyist in the entire city will want to be involved in. Our tax code is over two million words long, and the regulations are over seven million words long, and any changes to our immensely complex system could have absolutely enormous implications. There will be winners and there will be losers with any piece of legislation, and lobbyists will zealously fight to defend the turf belonging to their particular clients. Often lobbyists from different sides will literally be pitted directly against one another, and it won’t be pretty. In fact, one analyst that works for Cowen Washington Research Group says that we could soon be watching

Are you ready for mass chaos in Washington? There are lobbyists for just about every cause that you can possibly imagine, and they are always working hard to influence members of Congress on their particular issues. But when you are talking about a major tax reform bill, that is something that virtually every single lobbyist in the entire city will want to be involved in. Our tax code is over two million words long, and the regulations are over seven million words long, and any changes to our immensely complex system could have absolutely enormous implications. There will be winners and there will be losers with any piece of legislation, and lobbyists will zealously fight to defend the turf belonging to their particular clients. Often lobbyists from different sides will literally be pitted directly against one another, and it won’t be pretty. In fact, one analyst that works for Cowen Washington Research Group says that we could soon be watching