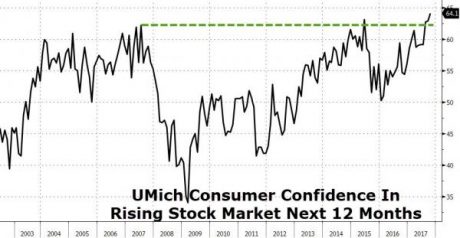

The only other times in our history when stock prices have been this high relative to earnings, a horrifying stock market crash has always followed. Will things be different for us this time? We shall see, but without a doubt this is what a pre-crash market looks like. This current bubble has been based on irrational euphoria that has been fueled by relentless central bank intervention, but now global central banks are removing the artificial life support in unison. Meanwhile, the real economy continues to stumble along very unevenly. This is the longest that the U.S. has ever gone without a year in which the economy grew by at least 3 percent, and many believe that the next recession is very close. Stock prices cannot stay completely disconnected from economic reality forever, and once the bubble bursts the pain is going to be unlike anything that we have ever seen before.

The only other times in our history when stock prices have been this high relative to earnings, a horrifying stock market crash has always followed. Will things be different for us this time? We shall see, but without a doubt this is what a pre-crash market looks like. This current bubble has been based on irrational euphoria that has been fueled by relentless central bank intervention, but now global central banks are removing the artificial life support in unison. Meanwhile, the real economy continues to stumble along very unevenly. This is the longest that the U.S. has ever gone without a year in which the economy grew by at least 3 percent, and many believe that the next recession is very close. Stock prices cannot stay completely disconnected from economic reality forever, and once the bubble bursts the pain is going to be unlike anything that we have ever seen before.

If you think that these ridiculously absurd stock prices are sustainable, there is something that I would like for you to consider. The only times in our history when the cyclically-adjusted return on stocks has been lower, a nightmarish stock market crash happened soon thereafter…

The Nobel-Laureate, Robert Shiller, developed the cyclically-adjusted price/earnings ratio, the so-called CAPE, to assess whether stocks are likely to be over- or under-valued. It is possible to invert this measure to obtain a cyclically-adjusted earnings yield which allows one to measure prospective real returns. If one does this, the answer for the US is that the cyclically-adjusted return is now down to 3.4 percent. The only times it has been still lower were in 1929 and between 1997 and 2001, the two biggest stock market bubbles since 1880. We know now what happened then. Is it going to be different this time?

Since the market bottomed out in early 2009, the S&P 500 has been on a historic run. If this rally had been based on a booming economy that would be one thing, but the truth is that the U.S. economy has not seen 3 percent yearly growth since the middle of the Bush administration. Instead, this insane bubble has been almost entirely fueled by central bank manipulation, and now that manipulation is being dramatically scaled back.

And the guys on Wall Street know what is coming. For example, Joe Zidle says that this bull market is now in “the ninth inning”…

Joe Zidle, of Richard Bernstein Advisors, is arguing that the bull market has entered the bottom of the ninth inning.

“This is a late-cycle environment,” Zidle said on CNBC’s “Futures Now” recently.

“In innings terms, they’re not time dependent. An inning could be shorter or they could be longer. It just really depends,” the strategist said.

This bubble has lasted for much longer than it ever should have, and everyone understands that a day of reckoning is coming.

In fact, earlier today I came across an article on Zero Hedge that contained an absolutely remarkable quote from Eric Peters…

“We are investing as if 1987 will happen tomorrow, because it will,” said the CIO. “But we need to be long, or we’ll be out of business,” he explained, under pressure to perform. “So we construct option trades that are binary bets.” Which pay X profit if stocks rally, and cost Y if markets fall. No more and no less.

“What you do not want is a portfolio whose losses multiply depending on the severity of a decline.” That’s what most people have today. “At the last stage of the cycle, you want lots of binary bets. Many small wins. Before the big loss.”

“Are we at the start or the end of the ‘Don’t know what I’m buying’ cycle?” asked the same CIO. “No one knows.” But we’re definitely within it.

“When their complex swaps drop 40%, and prime brokers demand more margin, investors will cry ‘It’s not possible!’ But anything is possible.” The prime brokers will hang up and stop them out.

In case you don’t remember, in 1987 we witnessed the largest one day percentage decline in U.S. stock market history.

When it finally happens, millions upon millions of ordinary Americans will be completely shocked, but most insiders know that the other shoe is going to drop at some point.

In particular, watch financial stock prices very closely. Last month, Richard Bove issued a chilling warning about bank stocks…

One of Wall Street’s most vocal bank analysts is troubled by the rally in financials.

The Vertical Group’s Richard Bove warns that the overall market is just as dangerous as the late 1990s, and he cites momentum — not fundamentals — as what’s driving bank stocks to all-time highs.

“If we don’t get some event in the economy or in politics or in somewhere that is going to create more loan volume and better margins for the banks, then yes, they would come crashing down,” Bove said Monday on CNBC’s “Trading Nation.” “I think that the risk in these stocks is very high at the present time.”

It isn’t going to take much to set off an unstoppable chain of events. Our financial markets are even more vulnerable than they were in 2008, and the right trigger could unleash a crisis unlike anything we have ever seen in modern American history.

Unfortunately, most Americans keep getting fooled by the artificial boom and bust cycles that the central banks create. Right now most people seem to have been lulled into a false sense of security, and they truly believe that everything is going to be okay.

But every time before when the market has looked like this a crash has always followed, and this time will be no exception.

Michael Snyder is a Republican candidate for Congress in Idaho’s First Congressional District, and you can learn how you can get involved in the campaign on his official website. His new book entitled “Living A Life That Really Matters” is available in paperback and for the Kindle on Amazon.com.

{kind=link}