Federal Reserve Chairman Ben Bernanke has done it. He has succeeded in creating a new housing bubble. By driving mortgage rates down to the lowest level in 100 years and recklessly printing money with wild abandon, Bernanke has been able to get housing prices to rebound a bit. In fact, in some of the more prosperous areas of the country you would be tempted to think that it is 2005 all over again. If you can believe it, in some areas of the country builders are actually holding lotteries to see who will get the chance to buy their homes. Wow – that sounds great, right? Unfortunately, this “housing recovery” is not based on solid economic fundamentals. As you will see below, this is a recovery that is being led by investors. They are paying cash for cheap properties that they believe will appreciate rapidly in the coming years. Meanwhile, the homeownership rate in the United States continues to decline. It is now the lowest that it has been since 1995. There are a couple of reasons for this. Number one, there has not been a jobs recovery in the United States. The percentage of working age Americans with a job has not rebounded at all and is still about the exact same place where it was at the end of the last recession. Secondly, crippling levels of student loan debt continue to drive down the percentage of young people that are buying homes. So no, this is not a real housing recovery. It is an investor-led recovery that is mostly limited to the more prosperous areas of the country. For example, the median sale price of a home in Washington D.C. just hit a new all-time record high. But this bubble will not last, and when this new housing bubble does burst, will it end as badly as the last one did?

Federal Reserve Chairman Ben Bernanke has done it. He has succeeded in creating a new housing bubble. By driving mortgage rates down to the lowest level in 100 years and recklessly printing money with wild abandon, Bernanke has been able to get housing prices to rebound a bit. In fact, in some of the more prosperous areas of the country you would be tempted to think that it is 2005 all over again. If you can believe it, in some areas of the country builders are actually holding lotteries to see who will get the chance to buy their homes. Wow – that sounds great, right? Unfortunately, this “housing recovery” is not based on solid economic fundamentals. As you will see below, this is a recovery that is being led by investors. They are paying cash for cheap properties that they believe will appreciate rapidly in the coming years. Meanwhile, the homeownership rate in the United States continues to decline. It is now the lowest that it has been since 1995. There are a couple of reasons for this. Number one, there has not been a jobs recovery in the United States. The percentage of working age Americans with a job has not rebounded at all and is still about the exact same place where it was at the end of the last recession. Secondly, crippling levels of student loan debt continue to drive down the percentage of young people that are buying homes. So no, this is not a real housing recovery. It is an investor-led recovery that is mostly limited to the more prosperous areas of the country. For example, the median sale price of a home in Washington D.C. just hit a new all-time record high. But this bubble will not last, and when this new housing bubble does burst, will it end as badly as the last one did?

Federal Reserve Chairman Ben Bernanke has stated over and over that one of his main goals is to “support the housing market” (i.e. get housing prices to go up). It took a while, but it looks like he is finally getting his wish. According to USA Today, U.S. home prices have been rising at the fastest rate in nearly seven years…

U.S. home prices in the USA’s 20 biggest cities rose 9.3% in the 12 months ending in February. It was the biggest annual growth rates in almost seven years, a closely watched housing index out Tuesday said.

In particular, home prices have been rising most rapidly in cities that experienced a boom during the last housing bubble…

Year over year, Phoenix continued to stand out with a gain of 23%, followed by San Francisco at almost 19% and Las Vegas at nearly 18%, the S&P/Case-Shiller index showed. Most of the cities seeing the biggest gains also fell hardest during the crash.

But is this really a reason for celebration? Instead of addressing the fundamental problems in our economy that caused the last housing crash, Bernanke has been seemingly obsessed with reinflating the housing bubble. As a recent article by Edward Pinto explained, the housing market is being greatly manipulated by the government and by the Fed…

While a housing recovery of sorts has developed, it is by no means a normal one. The government continues to go to extraordinary lengths to prop up sales by guaranteeing nearly 90% of new mortgage debt, financing half of all home purchase mortgages to buyers with zero equity at closing, driving mortgage interest rates to the lowest level in 100 years, and turning the Fed into the world’s largest buyer of new mortgage debt.

Thus, with real incomes essentially stagnant, this is a market recovery largely driven by low interest rates and plentiful government financing. This is eerily familiar to the previous government policy-induced boom that went bust in 2006, and from which the country is still struggling to recover. Creating over a trillion dollars in additional home value out of thin air does sound like a variant of dropping money out of helicopters.

And the Obama administration has been pushing very hard to get lenders to give mortgages to those with “weaker credit”. In other words, the government is once again trying to get the banks to give home loans to people that cannot afford them. The following is from the Washington Post…

The Obama administration is engaged in a broad push to make more home loans available to people with weaker credit, an effort that officials say will help power the economic recovery but that skeptics say could open the door to the risky lending that caused the housing crash in the first place.

President Obama’s economic advisers and outside experts say the nation’s much-celebrated housing rebound is leaving too many people behind, including young people looking to buy their first homes and individuals with credit records weakened by the recession.

We are repeating so many of the same mistakes that we made the last time.

But surely things will turn out differently this time, right?

I wouldn’t count on it.

Right now, an increasingly large percentage of homes are being purchased as investments. The following is from a recent Washington Times article…

Much of the pickup in sales and prices has been powered by investors who, convinced that the market is bottoming, are scooping up bountiful supplies of distressed and foreclosed properties at bargain prices and often paying with cash.

With investors targeting lower-priced homes that they intend to purchase and rent out, they have been crowding out many first-time buyers who are having difficulty getting mortgage loans and are at a disadvantage when competing with well-heeled buyers. Cash sales to investors now account for about one-third of all home sales, according to the National Association of Realtors.

And as we have seen in the past, an investor-led boom can turn into an investor-led bust very rapidly.

If this truly was a real housing recovery, the percentage of Americans that own a home would be going up.

Instead, it is going down.

As I mentioned above, the U.S. Census Bureau is reporting that the homeownership rate in the United States is now the lowest that it has been since 1995.

In particular, homeownership among college-educated young people is way down. They can’t afford to buy homes due to crippling levels of student loan debt…

For the average homeowner, the worst news is that these overleveraged and defaulting young borrowers no longer qualify for other kinds of loans — particularly home loans. In 2005, nearly nine percent of 25- to 30-year-olds with student debt were granted a mortgage. By late last year, that percentage, as an annual rate, was down to just above four percent.

The most precipitous drop was among those who owe $100,000 or more. New mortgages among these more deeply indebted borrowers have declined 10 percentage points, from above 16 percent in 2005 to a little more than 6 percent today.

“These are the people you’d expect to buy big houses,” said student loan expert Heather Jarvis. “They owe a lot because they have a lot of education. They have been through professional and graduate schools, but their payments are so significant, they have trouble getting a mortgage. They have mortgage-sized loans already.”

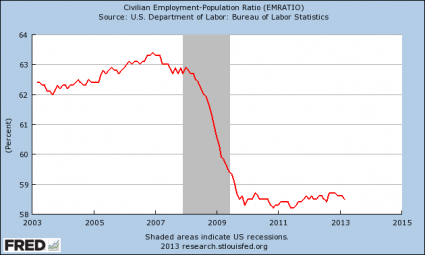

And the truth is that there simply are not enough good jobs in this country to support a housing recovery. In a previous article, I used the government’s own statistics to prove that there has not been a jobs recovery. If we were having a jobs recovery, the percentage of working age Americans with a job would be going up. Sadly, that is not happening…

And as I mentioned above, the “housing recovery” is mostly happening in the prosperous areas of the country.

In other areas of the United States, the devastating results of the last housing crash are still clearly apparent.

For example, the city of Dayton, Ohio is dealing with an estimated 7,000 abandoned properties.

As I wrote about the other day, there are approximately 70,000 abandoned buildings in Detroit, Michigan.

And all over the nation there are still “ghost towns” that were created when builders abruptly abandoned housing developments during the last recession. You can see some pictures of some of these ghost towns right here.

So the truth is that this is an isolated housing recovery that is being led by investors and that is being fueled by very reckless behavior by the Federal Reserve. It is not based on economic reality whatsoever.

In the end, will the collapse of this new housing bubble be as bad as the collapse of the last one was?

Please feel free to post a comment with your thoughts below…