Is this the beginning of the end for the eurozone? For years, European officials have been trying to “fix Greece”, but nothing has worked. Now a worst case scenario is rapidly unfolding, and a “Grexit” has become more likely than not. On Sunday, the European Central Bank announced that it was not going to provide any more emergency support for Greek banks. But that was the only thing keeping them alive. In order to prevent total chaos, Greek banks have been shut down for at least a week. ATMs are still open, but it is being reported that daily withdrawals will be limited to 60 euros. Of course nobody knows for sure if or when the banks will reopen after this “bank holiday” is over, so needless to say average Greek citizens are pretty freaked out right about now. In addition, the stock market in Greece is not going to open on Monday either. This is what a national financial meltdown looks like, and the nightmare that has been unleashed in Greece will soon start spreading to much of the rest of Europe.

Is this the beginning of the end for the eurozone? For years, European officials have been trying to “fix Greece”, but nothing has worked. Now a worst case scenario is rapidly unfolding, and a “Grexit” has become more likely than not. On Sunday, the European Central Bank announced that it was not going to provide any more emergency support for Greek banks. But that was the only thing keeping them alive. In order to prevent total chaos, Greek banks have been shut down for at least a week. ATMs are still open, but it is being reported that daily withdrawals will be limited to 60 euros. Of course nobody knows for sure if or when the banks will reopen after this “bank holiday” is over, so needless to say average Greek citizens are pretty freaked out right about now. In addition, the stock market in Greece is not going to open on Monday either. This is what a national financial meltdown looks like, and the nightmare that has been unleashed in Greece will soon start spreading to much of the rest of Europe.

This reminds me so much of what happened in Cyprus. Up until the very last minute, politicians were promising everyone that their money was perfectly safe, and then the hammer was brought down.

The exact same pattern is playing out in Greece. For example, just check out what one very prominent Greek politician said on television on Saturday…

“Citizens should not be scared, there is no blackmail,” Panos Kammenos, head of the government’s coalition ally, told local television. “The banks won’t shut, the ATMs will (have cash). All this is exaggeration,” he said.

One day later, the banks did get shut down and ATMs all over the country started running out of cash. The following comes from CNBC…

Despite a tweet from Greek Finance Minister Yanis Varoufakis that his government “opposed the very concept” of any controls, Greek Prime Minister Alexis Tsipras said later Sunday that he had forced the country’s central bank to recommend a bank holiday and capital controls.

The Athens stock exchange will also be closed as the government tries to manage the financial fallout of the disagreement with the European Union and the International Monetary Fund. Greece’s banks, kept afloat by emergency funding from the European Central Bank, are on the front line as Athens moves towards defaulting on a 1.6 billion euros payment due to the International Monetary Fund on Tuesday.

So what is the moral of this story?

Never trust politicians – especially when a major financial crisis is looming.

All over Greece, people are taking photos of very long lines at the ATMs that actually do still have some cash. Here are just a couple of examples…

Queue for an ATM in Greece. People wanting physical Euros. Most ATMs are empty now. pic.twitter.com/iKW6EvHGGC

— Jason Hunter (@hunterhacker) June 27, 2015

—–

My brother sends me this pic of ATM lines in Greece, many have run out of cash already. pic.twitter.com/tceblU28ZS — Andrea Tantaros (@AndreaTantaros) June 27, 2015

Of course those that were smart enough to see this coming took their money out of the banks long ago. And even as late as last week, people were pulling more than a billion euros out of the banks every single day. Without direct intervention by the European Central Bank, most Greek banks would have totally collapsed by now…

Customers have been withdrawing money in vast quantities ever since Syriza came to power, fearing that if Greece is thrown out of the single currency their euro savings will be converted into drachma – likely to be worth far less.

In the last week, the sums being taken out have risen to well over one billion euros a day, moved either to foreign banks or stashed in notes under mattresses.

It has been a slow and steady run on Greece’s banks which is now speeding up – for the finish line may well be in sight. Until now, the country’s banks have been kept afloat by €88 billion in loans from the European Central Bank.

So now that the banks are shut down, what happens next?

Needless to say, economic activity in Greece is going to come to a grinding halt. In addition, very few foreigners are going to want to travel to Greece or deal with Greece financially until this crisis is resolved somehow…

An extended bank shutdown and tough capital controls will likely wreak further havoc on the Greek economy by scaring away tourists and chilling commercial activity.

And with Greece unable to borrow from financial markets, and apparently unwilling to strike a deal with the only institutions prepared to lend it money, it will find itself sliding rapidly towards exit from the euro.

When the Greek banks finally do reopen, which of them will still be solvent?

Will some of them need “bail-ins”?

Will account holders be forced to take “haircuts” like we saw in Cyprus?

For the moment, what we do know is that the banks will all be shut down until at least July 6th. Greek Prime Minister Alexis Tsipras has called for a national referendum to be held on July 5th. The Greek people will get a chance to vote on whether or not the latest creditor proposals should be accepted. But the funny thing is that Tsipras and the rest of Syriza are already encouraging the Greek people to vote no…

Greece’s parliament has voted in favor of Prime Minister Alexis Tsipras’ motion to hold a referendum on the country’s creditor proposals for reforms in exchange for loans, the Associated Press reported. Tsipras and his coalition government have urged people to vote against the deal, throwing into question the country’s financial future.

The vote is to be held next Sunday, July 5. It has raised the question of whether Greece can remain in Europe’s joint currency, the euro.

So why hold a referendum if you just want everyone to vote no?

It is because Tsipras does not want to solely shoulder the blame for what comes next. A “no vote” would essentially be a vote to leave the euro and go back to the drachma. The following comes from the Daily Mail…

Should Greeks vote against the new bailout, most economists believe Greece will be forced to quit the single currency and return to the drachma. The country could even eventually be forced out of the EU, though Greek politicians have long argued a Grexit would not be the automatic result of default.

However, next week’s referendum is likely to be billed as, in effect, an in-out vote on the euro.

If Greece does default and ends up leaving the euro, the short-term economic consequences for Greece will be catastrophic.

But the rest of Europe will feel a tremendous amount of pain as well. In fact, we are already getting a sneak peek at coming attractions. As we approach Monday morning in Europe, Asian stocks are crashing big time, and European futures are absolutely cratering. It should be very interesting to see how Monday plays out.

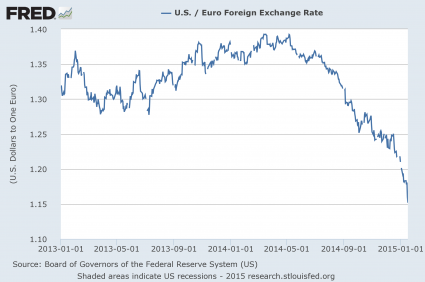

In addition, the euro is already way down in early trading. If Greece does ultimately leave the euro, the value of the euro is going to plunge like a rock. As I have warned repeatedly, the euro is heading for parity with the U.S. dollar, and at some point it will drop below parity.

And once Greece is out, everyone is going to be speculating who the “next Greece” will be. Expect bond yields for Italy, Spain, Portugal and France to go skyrocketing.

Just a couple of days ago, I issued a red alert for the second half of 2016. We are entering a period of time when the global financial system is beginning to unravel. Most people still have a tremendous amount of faith in the system and assume that those running it are fully capable of keeping it from collapsing. In fact, many have accused me of being crazy for suggesting that the global financial system is in imminent danger of imploding.

A very wise man once said that “pride goeth before destruction”. Our arrogance and our blind faith in the fundamentally flawed systems that we have established will contribute greatly to our undoing.

Events are starting to accelerate greatly now, and it is just a matter of time before we see who was right and who was wrong.