Global economic conditions are really starting to deteriorate quite rapidly. Economists were projecting that Japan’s GDP would shrink by 3.8 percent on an annualized basis in the fourth quarter, but instead it greatly surpassed expectations by plunging 6.3 percent. If Japan’s GDP falls again during the first quarter of 2020, and thanks to the coronavirus outbreak that seems very likely, then the world’s third largest economy will officially be in a recession. But of course the outlook for China is even worse. At this point, economic activity in China has come to a standstill, and this has thrown global supply chains into a state of chaos. It certainly appears that the entire global economy will shrink during the first quarter, and that will be the very first time that has happened in more than a decade. And if this coronavirus outbreak continues to intensify in the months ahead, the economic consequences are going to be absolutely catastrophic.

Global economic conditions are really starting to deteriorate quite rapidly. Economists were projecting that Japan’s GDP would shrink by 3.8 percent on an annualized basis in the fourth quarter, but instead it greatly surpassed expectations by plunging 6.3 percent. If Japan’s GDP falls again during the first quarter of 2020, and thanks to the coronavirus outbreak that seems very likely, then the world’s third largest economy will officially be in a recession. But of course the outlook for China is even worse. At this point, economic activity in China has come to a standstill, and this has thrown global supply chains into a state of chaos. It certainly appears that the entire global economy will shrink during the first quarter, and that will be the very first time that has happened in more than a decade. And if this coronavirus outbreak continues to intensify in the months ahead, the economic consequences are going to be absolutely catastrophic.

Even though the experts were anticipating a slowdown in Japan, nobody had any idea that it would be this bad…

Japan’s gross domestic product shrank at an annualized pace of 6.3 percent from the previous quarter in the three months through December, according to a preliminary estimate by the Cabinet Office released Monday.

Economists surveyed had predicted a fall of 3.8 percent, flagging the adverse impact of a sales tax increase, weak global demand and typhoon disruption.

The sales tax increase is being primarily blamed for this collapse in GDP, and without a doubt consumer spending in Japan was way down last quarter…

Consumer spending fell 11.1% after the national sales tax was raised in October to 10% from 8%. During the same month, Typhoon Hagibis ravaged a large swathe of the country.

Capital spending declined 14.1% and exports slipped 0.4% due to the fallout from the U.S.-China trade war.

Japanese officials were hoping that GDP would bounce back this quarter, but now the coronavirus outbreak has changed everything.

At this point it is very difficult to be positive about the immediate future of the Japanese economy, and an increasing number of experts are now anticipating a recession. Here is one example…

“I’m getting ready for another contraction in Japan’s first quarter. There just aren’t any positive factors to build a positive growth forecast,” said Mari Iwashita, chief market economist at Daiwa Securities Co., flagging her view that the economy is likely falling into recession.

The Japanese economy greatly benefits from the horde of tourists that usually come over from China, and the two nations have developed a very close trading relationship.

Now that those two factors are being disrupted, the outlook for the second quarter is decidedly grim…

“There is a good chance of Japan’s economy falling into a recession,” Yoshiki Shinke, chief economist at Dai-ichi Life Research Institute, said before Monday’s data was released. He flagged the risks of supply chains being affected if the outbreak was prolonged.

The coronavirus is taking a toll on the number of Chinese tourists to Japan and manufacturing activity due to the economy’s close ties with China, prompting some economists to forecast a contraction lasting two quarters.

Ultimately, it is going to be exceedingly difficult for Japan to avoid a recession.

But if Chinese GDP also plunges into recession territory this year, that will be even bigger news.

According to the New York Times, “the entire global economy could suffer from a prolonged shock in China”, and so investors will be watching the development of this crisis very carefully.

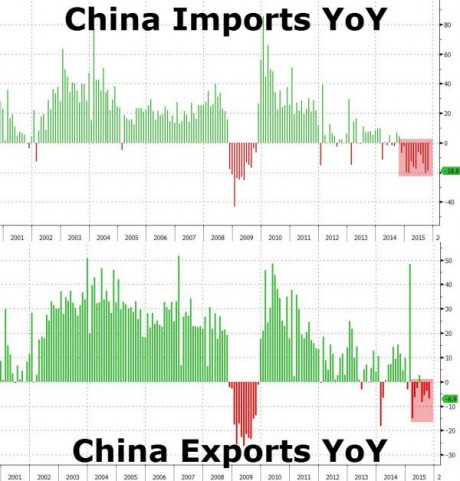

The number of confirmed cases and the official death toll both continue to rise, and the draconian measures that the Chinese have taken to contain the outbreak have slowed the Chinese economy to a crawl. The following is how Zero Hedge summarized the recent economic data that we have seen come out of China…

While not perfect, and certainly not a comprehensive view of what is really taking place “on the ground”, the above data is a useful real-time indicator of how the people in China perceive the threat of the coronavirus pandemic, and one thing is abundantly clear: as the pandemic spreads further without containment, and as the charts above flatline, so will China’s economy, which means that while Goldman’s draconian view of what happens to Q1 GDP is spot on, the expectation for a V-shaped recovery in Q2 and onward will vaporize faster than a vial of ultra-biohazardaous viruses in a Wuhan virology lab.

Of course many in the financial world are still hoping that things won’t be too bad.

For example, Dun and Bradstreet is hoping that the crisis in China will only “cause a drag of approximately one percentage point on global GDP”…

China, the world’s second largest economy after US, contributes about 20 percent to the world’s gross domestic product (GDP). However, according to a report by Dun and Bradstreet, the Chinese economy might cause a drag of approximately one percentage point on global GDP if prevention of Coronavirus gets delayed beyond the summer of 2020.

That is a wildly optimistic projection, but hopefully they are right.

Hopefully the coronavirus will fizzle out with the arrival of warmer weather and the global economy can start to get back to normal.

Unfortunately, a return to “normal” is probably not in the cards.

Even before this coronavirus outbreak, the global economy was really starting to slow down. Economic numbers were absolutely dismal all over the world, and many experts were warning that we were right on the verge of the next global recession.

Now that this outbreak has erupted, we definitely have much more momentum in a downward direction. Very challenging times are ahead, although most people in the western world still don’t understand what is happening.

As far as the coronavirus is concerned, the key will be what happens to the number of confirmed cases outside of China. Over the past week that number has roughly doubled, and if that keeps happening every week we will soon have a full-blown global pandemic on our hands.

There are now 75 confirmed cases in Singapore, 59 confirmed cases in Japan and 57 confirmed cases in Hong Kong. It is becoming increasingly difficult to keep this virus contained, and we are rapidly approaching a major tipping point.

About the Author: I am a voice crying out for change in a society that generally seems content to stay asleep. My name is Michael Snyder and I am the publisher of The Economic Collapse Blog, End Of The American Dream and The Most Important News, and the articles that I publish on those sites are republished on dozens of other prominent websites all over the globe. I have written four books that are available on Amazon.com including The Beginning Of The End, Get Prepared Now, and Living A Life That Really Matters. (#CommissionsEarned) By purchasing those books you help to support my work. I always freely and happily allow others to republish my articles on their own websites, but due to government regulations I need those that republish my articles to include this “About the Author” section with each article. In order to comply with those government regulations, I need to tell you that the controversial opinions in this article are mine alone and do not necessarily reflect the views of the websites where my work is republished. This article may contain opinions on political matters, but it is not intended to promote the candidacy of any particular political candidate. The material contained in this article is for general information purposes only, and readers should consult licensed professionals before making any legal, business, financial or health decisions. Those responding to this article by making comments are solely responsible for their viewpoints, and those viewpoints do not necessarily represent the viewpoints of Michael Snyder or the operators of the websites where my work is republished. I encourage you to follow me on social media on Facebook and Twitter, and any way that you can share these articles with others is a great help.

{kind=link}