Since the end of the last recession, the outlook for the U.S. economy has never been as dire as it is right now. Everywhere you look, economic red flags are popping up, and the mainstream media is suddenly full of stories about “the coming recession”. After several years of relative economic stability, things appear to be changing dramatically for the U.S. economy and the global economy as a whole. Over and over again, we are seeing things happen that we have not witnessed since the last recession, and many analysts expect our troubles to accelerate as we head into the final months of 2019.

Since the end of the last recession, the outlook for the U.S. economy has never been as dire as it is right now. Everywhere you look, economic red flags are popping up, and the mainstream media is suddenly full of stories about “the coming recession”. After several years of relative economic stability, things appear to be changing dramatically for the U.S. economy and the global economy as a whole. Over and over again, we are seeing things happen that we have not witnessed since the last recession, and many analysts expect our troubles to accelerate as we head into the final months of 2019.

We should certainly hope that things will soon turn around, but at this point that does not appear likely. The following are 28 signs of economic doom as the pivotal month of September begins…

#1 The U.S. and China just slapped painful new tariffs on one another, thus escalating the trade war to an entirely new level.

#2 JPMorgan Chase is projecting that the trade war will cost “the average U.S. household” $1,000 per year.

#3 Yield curve inversions have preceded every single U.S. recession since the 1950s, and the fact that it has happened again is one of the big reasons why Wall Street is freaking out so much lately.

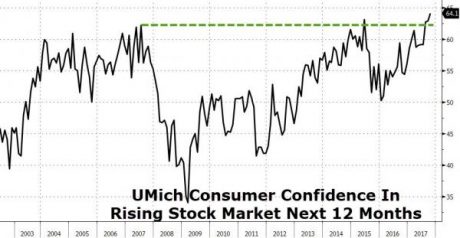

#4 We just witnessed the largest decline in U.S. consumer sentiment in 7 years.

#5 Mortgage defaults are rising at the fastest pace that we have seen since the last financial crisis.

#6 Sales of luxury homes valued at $1.5 million or higher were down five percent during the second quarter of 2019.

#7 The U.S. manufacturing sector has contracted for the very first time since September 2009.

#8 The Cass Freight Index has been falling for a number of months. According to CNBC, it fell “5.9% in July, following a 5.3% decline in June and a 6% drop in May.”

#9 Gross private domestic investment in the United States was down 5.5 percent during the second quarter of 2019.

#10 Crude oil processing at U.S. refiners has fallen by the most that we have seen since the last recession.

#11 The price of copper often gives us a clear indication of where the economy is heading, and it is now down 13 percent over the last six months.

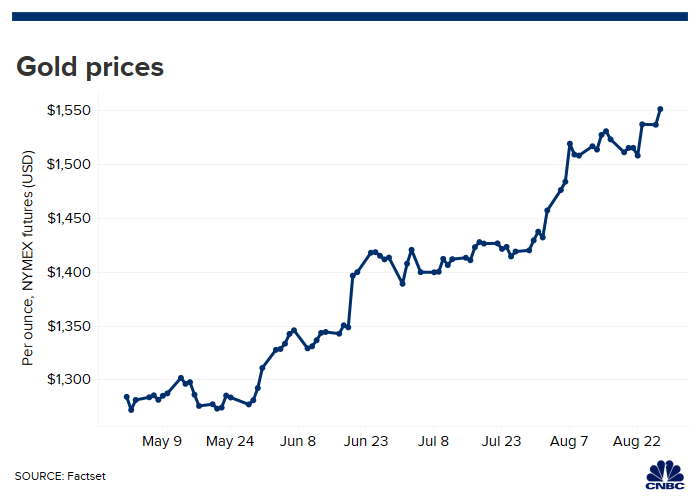

#12 When it looks like an economic crisis is coming, investors often flock to precious metals. So it is very interesting to note that the price of gold is up more than 20 percent since May.

#13 Women’s clothing retailer Forever 21 “is reportedly close to filing for bankruptcy protection”.

#14 We just learned that Sears and Kmart will close “nearly 100 additional stores” by the end of this year.

#15 Domestic shipments of RVs have fallen an astounding 20 percent so far in 2019.

#16 The Labor Department has admitted that the U.S. economy actually has 501,000 less jobs than they previously thought.

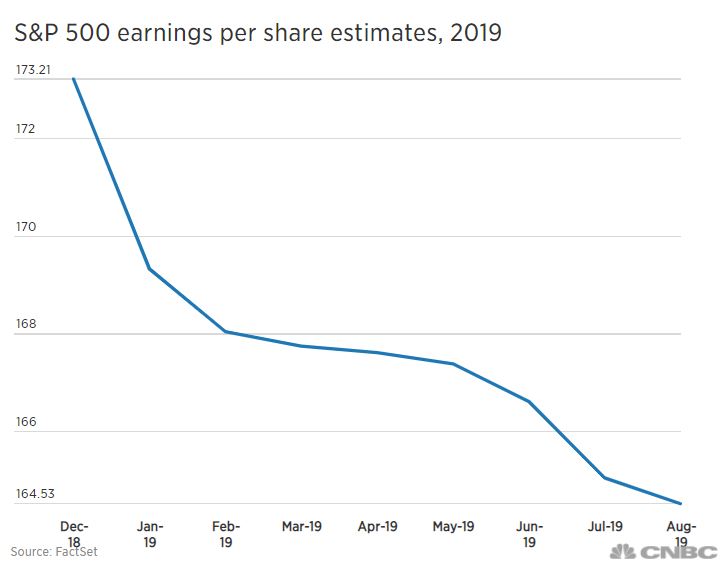

#17 S&P 500 earnings per share estimates have been steadily falling all year long.

#18 Morgan Stanley says that the possibility that we will see a global recession “is high and rising”.

#19 Global trade fell 1.4 percent in June from a year earlier, and that was the biggest drop that we have seen since the last recession.

#20 The German economy contracted during the second quarter, and the German central bank “is predicting the third quarter will also post a decline”.

#21 According to CNBC, the S&P 500 “just sent a screaming sell signal” to U.S. investors.

#22 Masanari Takada is warning that we could soon see a “Lehman-like” plunge in the stock market.

#23 Corporate insiders are dumping stocks at a pace that we haven’t seen in more than a decade.

#24 Apple CEO Tim Cook has been dumping millions of dollars worth of Apple stock.

#25 Instead of pumping his company’s funds into the stock market, Warren Buffett has decided to hoard 122 billion dollars in cash. This appears to be a clear indication that he believes that a crisis is coming.

#26 Investors are selling their shares in emerging markets funds at a pace that we have never seen before.

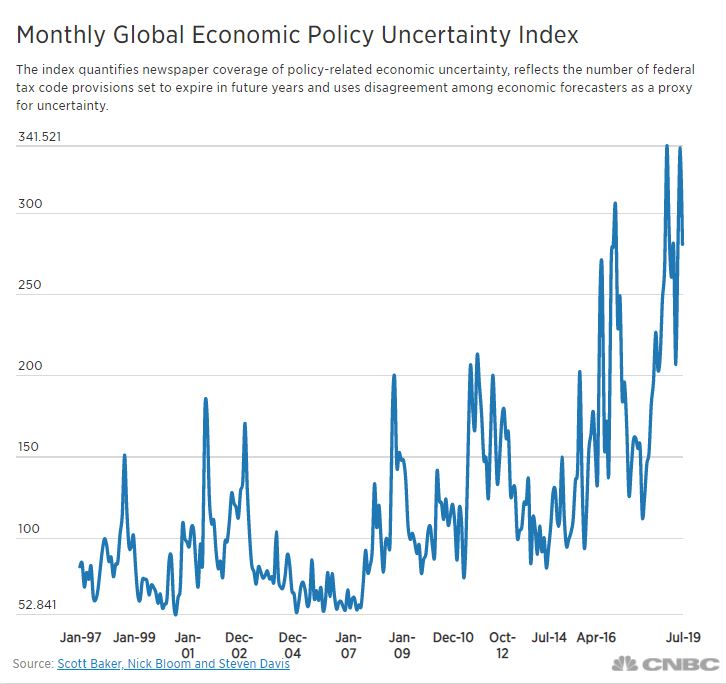

#27 The Economic Policy Uncertainty Index hit the highest level that we have ever seen in the month of June.

#28 Americans are searching Google for the term “recession” more frequently than we have seen at any time since 2009.

The signs are very clear, but unfortunately we live at a time when “normalcy bias” is rampant in our society.

If you are not familiar with “normalcy bias”, the following is how Wikipedia defines it…

The normalcy bias, or normality bias, is a belief people hold when considering the possibility of a disaster. It causes people to underestimate both the likelihood of a disaster and its possible effects, because people believe that things will always function the way things normally have functioned. This may result in situations where people fail to adequately prepare themselves for disasters, and on a larger scale, the failure of governments to include the populace in its disaster preparations. About 70% of people reportedly display normalcy bias in disasters.[1]

For most Americans, the crisis of 2008 and 2009 is now a distant memory, and the vast majority of the population seems confident that brighter days are ahead even if we must weather a short-term economic recession first. As a result, most people are not preparing for a major economic crisis, and that makes us extremely vulnerable.

In 2008 and 2009, the horrible financial crisis and the bitter recession that followed took most Americans completely by surprise.

It will be the same this time around, even though the warning signs are there for all to see.

About the author: Michael Snyder is a nationally-syndicated writer, media personality and political activist. He is the author of four books including Get Prepared Now, The Beginning Of The End and Living A Life That Really Matters. His articles are originally published on The Economic Collapse Blog, End Of The American Dream and The Most Important News. From there, his articles are republished on dozens of other prominent websites. If you would like to republish his articles, please feel free to do so. The more people that see this information the better, and we need to wake more people up while there is still time.

About the author: Michael Snyder is a nationally-syndicated writer, media personality and political activist. He is the author of four books including Get Prepared Now, The Beginning Of The End and Living A Life That Really Matters. His articles are originally published on The Economic Collapse Blog, End Of The American Dream and The Most Important News. From there, his articles are republished on dozens of other prominent websites. If you would like to republish his articles, please feel free to do so. The more people that see this information the better, and we need to wake more people up while there is still time.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}