Is America really “the land of the free”? Most people think of money as simply a medium of exchange that makes economic transactions more convenient, but the truth is that it is much more than that. Money is also a form of social control. Just think about it. What did you do this morning? Well, if you are like most Americans, you either got up and went to work (to make money) or to school (to learn the skills that you will need to make money). We spend a great deal of our lives pursuing the almighty dollar, and there are literally millions of laws, rules and regulations about how we earn our money, about how we spend our money and about how much of our money the government gets to take from us. Not that money is a bad thing in itself. Without money, it would be really hard to have a modern society. Unfortunately, our money is based on debt, and debt levels in the United States have exploded to absolutely unprecedented levels in recent years. The borrower is the servant of the lender, and if you are like most Americans, nearly every major purchase that you make in your life is going to involve debt. Do you want to get a college education so that you can get a “good job”? You are told to get a student loan. Do you want a car? You are encouraged to get an auto loan and to stretch out the payments for as long as possible. Do you want a home? You are probably going to end up with a big fat mortgage. And of course I could go on and on and on. The cold, hard truth of the matter is that most Americans are debt slaves. Most of us spend our entire lives trapped in an endless cycle of debt that we never escape until we die, and meanwhile our years of hard labor are greatly enriching those that own our debts.

Is America really “the land of the free”? Most people think of money as simply a medium of exchange that makes economic transactions more convenient, but the truth is that it is much more than that. Money is also a form of social control. Just think about it. What did you do this morning? Well, if you are like most Americans, you either got up and went to work (to make money) or to school (to learn the skills that you will need to make money). We spend a great deal of our lives pursuing the almighty dollar, and there are literally millions of laws, rules and regulations about how we earn our money, about how we spend our money and about how much of our money the government gets to take from us. Not that money is a bad thing in itself. Without money, it would be really hard to have a modern society. Unfortunately, our money is based on debt, and debt levels in the United States have exploded to absolutely unprecedented levels in recent years. The borrower is the servant of the lender, and if you are like most Americans, nearly every major purchase that you make in your life is going to involve debt. Do you want to get a college education so that you can get a “good job”? You are told to get a student loan. Do you want a car? You are encouraged to get an auto loan and to stretch out the payments for as long as possible. Do you want a home? You are probably going to end up with a big fat mortgage. And of course I could go on and on and on. The cold, hard truth of the matter is that most Americans are debt slaves. Most of us spend our entire lives trapped in an endless cycle of debt that we never escape until we die, and meanwhile our years of hard labor are greatly enriching those that own our debts.

Have you ever found yourself wondering why you can never seem to get ahead financially no matter how hard you work?

Well, it is probably because you have gotten yourself enslaved to debt.

Just consider the following example about credit card debt from a former Goldman Sachs banker…

On the debt side of things, how much does your credit card company earn if you carry just an average of a $5,000 credit card balance, paying, say, 22% annual interest rate (compounding monthly) for the next 10 years?

In your mind you owe a balance of only $5,000, which is not a huge amount, especially for someone gainfully employed. After all, $5,000 is just a quick Disney trip, or a moderately priced ski-trip, or that week in Hawaii. You think to yourself, “how bad could it be?”

The answer, including the cost of monthly compounding, is $44,235, or about 9 times what it appears to cost you at face value.

But a large percentage of Americans never pay off their credit cards at all. They make small payments each month, but then they just keep on adding to their balances.

In the end, that is financial suicide.

If you carry an “average balance” on your credit cards each month, and those credit cards have an “average” interest rate, you could end up paying millions of dollars to the credit card companies by the end of your life…

Let’s say you are an average American household, and you carry an average balance of $15,956 in credit card debt.

Also, as an average American household, let’s assume you pay an average current rate of 12.83%.

Finally, let’s assume you carry this average balance for 40 years, between ages 25 and 65. How much did your credit card company make off of you and your extreme averageness?

Answer: $2,629,618.64

Sadly, approximately 46% of all Americans carry a credit card balance from month to month.

How stupid can we be as a nation?

When you become enslaved to the credit card companies, your toil and sweat makes them much wealthier. It is a form of slavery that does not require anyone pointing a gun at you.

But we never seem to learn. Incredibly, 43 percent of all American families spend more than they earn each year.

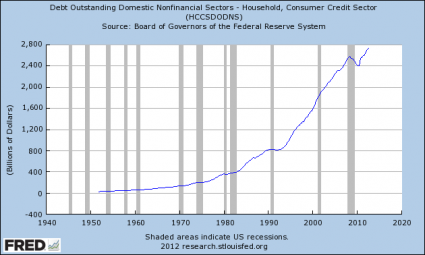

As the chart below demonstrates, consumer credit actually declined for a short while during the last recession, but now it has turned around and the growth of consumer credit is on the same trajectory as it was before the last economic crisis…

Today, the total amount of consumer credit in the United States is 15 times larger than it was 40 years ago.

And every major “milestone” in our lives typically involves even more debt.

-The total amount of student loan debt in the United States recently passed a trillion dollars, and approximately two-thirds of all college students graduate with student loan debt at this point.

-Total home mortgage debt in the United States is now about 5 times larger than it was just 20 years ago, and mortgage debt as a percentage of GDP has more than tripled since 1955.

-Car loans just keep getting longer and longer, and approximately 70 percent of all car purchases in the United States now involve an auto loan.

-Want to get married? That average cost of a wedding is now $26,989 which is probably going to mean even more debt unless you have wealthy parents.

-Do you have a serious medical problem? According to a report published in The American Journal of Medicine, medical bills are a major factor in more than 60 percent of the personal bankruptcies in the United States.

Are you starting to understand why approximately half of all Americans die broke?

And I have not even begun to talk about our collective debts yet.

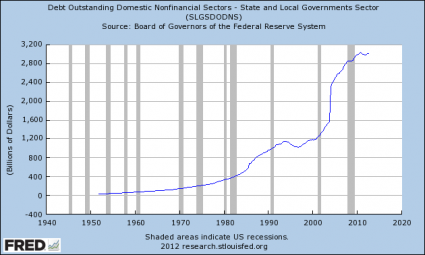

Government debt is a collective form of debt. You may not have voted for any of the politicians that have been racking up debt in your name, but part of it still belongs to you.

Since the year 2000, state and local government debt has more than doubled. These are collective debts for which we are all responsible…

And of course the biggest collective debt of all is the U.S. national debt.

In a previous article, I discussed how the national debt has exploded out of control in recent years. If you can believe it, the U.S. debt to GDP ratio has increased from 66.6 percent to 103 percent since 2007, and the U.S. government accumulated more new debt during Barack Obama’s first term than it did under the first 42 U.S. presidents combined.

When you break things down by household, the numbers look even more frightening.

During Barack Obama’s first four years in the White House, the amount of new debt accumulated by the federal government breaks down to approximately $50,521 for every single household in the United States.

And as I have mentioned previously, if you started paying off just the new debt that the federal government has accumulated during the Obama administration at the rate of one dollar per second, it would take more than 184,000 years to pay it off.

Well, you might argue, none of that debt will ever be paid off in our lifetimes.

And you would be right.

But what we are doing is consigning our children, our grandchildren and all future generations of Americans to a lifetime of debt slavery.

How nice of us, eh?

Over the past 10 years, the U.S. national debt has grown by an average of 9.3 percent per year, but the overall U.S. economy has only grown by an average of just 1.8 percent per year.

How do we expect to continue doing this?

Fortunately, more Americans are starting to wake up to how foolish all of this is.

For example, the following is what Home Depot Founder Kenneth Langone told CNBC on Tuesday…

“The fundamentals haven’t changed … And we don’t know when the storm is going to hit,” he predicted. “It has to happen.If you look at our debt to GDP, eventually you reach a point where there’s no turning back.”

He used an analogy to make his point. “If you had one meal left, and you had your grandchild with you, would you eat if or give it to your grandchild?”

He said all people would say “give it to my grandchild.”

But pursuing the president’s vision, he argued, “[Is] eating the grandchildren’s breakfast, lunch and dinner right now. And the [grandchildren] haven’t been born yet.”

What we are doing to our children and our grandchildren is beyond criminal. We are selling away their futures in order to make our lives more pleasant.

Right now, we are stealing more than 100 million dollars from our children and our grandchildren every single hour of every single day.

So where is the outrage over this theft?

Sadly, most Americans don’t even realize that all of this is by design. When the Federal Reserve system was created back in 1913, it was designed to get the U.S. government trapped in an endless spiral of debt.

And it worked. Today, the U.S. national debt is now more than 5000 times larger than it was when the Federal Reserve was first created.

Our society has become addicted to debt, and that means that we have become addicted to slavery.

We are not the “land of the free”. The truth is that we are now the “land of the servants”.

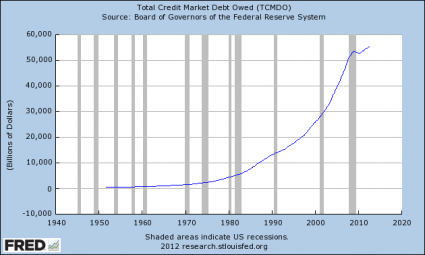

Over the past 40 years, the total amount of debt owed in the United States (government, business, consumer, etc.) has grown from less than 2 trillion dollars to more than 55 trillion dollars…

So who benefits from all of this?

I talked about this in a previous article. The ultra-wealthy and the international bankers make enormous profits by lending money to all the rest of us.

According to a stunning report that was released last summer, the global elite have up to 32 trillion dollars stashed away in offshore tax havens around the globe.

How did they get so much money?

The borrower is the servant of the lender. They have gotten rich at our expense.

But most people live their entire lives without ever understanding how the game is being played.

Today, most Americans see that the Dow is back above 14,000 and they hear the mainstream media telling them that happy days are here again and so they just believe that things are going to turn out okay somehow.

And it certainly does not help that most people seem to let others do their thinking for them. In fact, about 23% of all Americans can’t even read at this point.

So is there any hope for us?

Please feel free to post a comment with your opinion below…