The mainstream media would have us believe that the U.S. economy must be in great shape since the stock market has been setting new all-time record highs this month. But is that really true? Yes, surging stock prices have enabled sales of beach homes in the Hamptons to hit a brand new record high. However, the reality is that stock prices have not risen dramatically in recent years because corporations are doing so much better than before. In fact, the growth in stock prices has been far, far greater than the growth of corporate revenues. The only reason that stock prices have been climbing so much is because the Federal Reserve has been flooding the financial system with hundreds of billions of dollars that it has created out of thin air. The Fed has created an artificial stock market bubble that is completely and totally divorced from economic reality.

The mainstream media would have us believe that the U.S. economy must be in great shape since the stock market has been setting new all-time record highs this month. But is that really true? Yes, surging stock prices have enabled sales of beach homes in the Hamptons to hit a brand new record high. However, the reality is that stock prices have not risen dramatically in recent years because corporations are doing so much better than before. In fact, the growth in stock prices has been far, far greater than the growth of corporate revenues. The only reason that stock prices have been climbing so much is because the Federal Reserve has been flooding the financial system with hundreds of billions of dollars that it has created out of thin air. The Fed has created an artificial stock market bubble that is completely and totally divorced from economic reality.

Meanwhile, everything is not so fine for the rest of the U.S. economy. Economic growth projections have been steadily declining over the past two years, and the growth rate of personal income in the United States has been on a huge downward trend since 2008. The U.S. economy actually lost 240,000 full-time jobs last month, and the middle class continues to shrink.

So welcome to the “new normal” where most Americans struggle at least part of the time. According to one recent survey, “four out of 5 U.S. adults struggle with joblessness, near poverty or reliance on welfare for at least parts of their lives”. Things are tough out there, and they are steadily getting tougher.

Yes, the boys and girls up on Wall Street are doing great (for the moment), but most of the rest of the country is really struggling. We have never even come close to recovering from the last major economic crisis, and now another one is rapidly approaching.

The other day, Chartist Friend from Pittsburgh sent me an email and told me that he had some charts that he wanted to share with me and asked if I wanted to see them. I said sure, send them over right away. These charts show very clearly that the stock market has become completely divorced from reality.

In a normal market, stock prices would only rise dramatically if the overall economy was healthy and growing. Unfortunately, our economy is far from healthy and has been declining for a very long time. If the financial markets were not being pumped up by so much money printing and so much debt, there is no way that stock prices would be this high.

If we truly did have a free market financial system, stock prices should be a reflection of the overall economy. Instead, we have a very sick economy and financial markets that have been very highly manipulated.

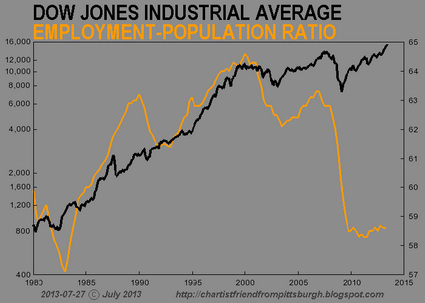

For example, just check out the first chart that I have posted below. If the economy was actually getting better, the percentage of working age Americans with a job should be increasing. Sadly, that is not happening…

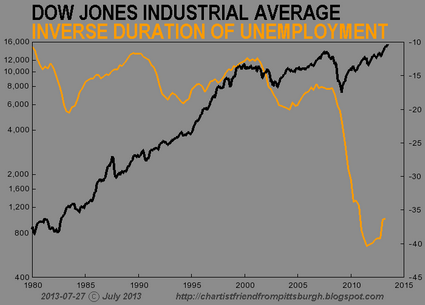

This next chart shows how the average duration of unemployment has absolutely skyrocketed in recent years. Yes, the duration of unemployment has improved slightly in recent months, but we are still very far from where we used to be. Meanwhile, the stock market has been soaring to new all-time record highs…

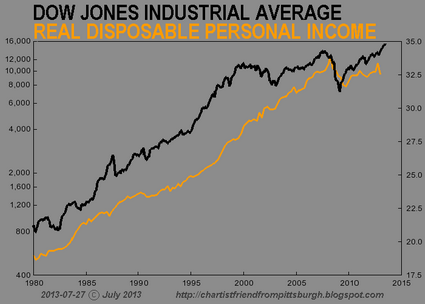

Traditionally, there has been a high degree of correlation between stock prices and real disposable personal income. From the chart below, you can see that this relationship held up quite well through the end of the last recession, and then it started breaking down. This is especially true at the very end of the chart. Real Disposable income has started to decline sharply but stock prices just continue to soar…

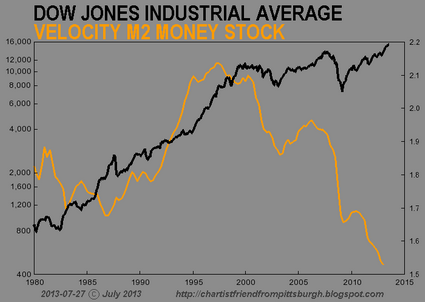

When an economy is healthy, money tends to circulate through that economy at a healthy pace. That is why the chart below is so alarming. The velocity of money is the lowest that it has been in modern times, and this indicates that economic activity should be slowing down. But the Federal Reserve has enabled the bankers to thrive by pumping massive amounts of money into the financial system…

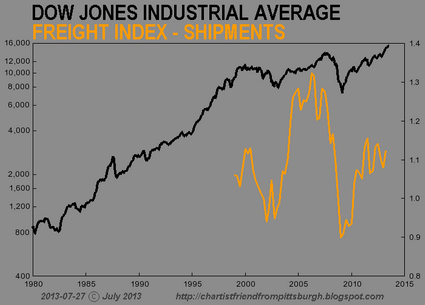

When an economy goes into recession, freight shipments tend to go down. In the chart below, you can see that this happened during the past two recessions. Unfortunately, we have never even come close to returning to the level that we were at before the last recession, and yet the stock market has been able to soar to unprecedented heights…

When an economy is growing and people are able to get good jobs, they tend to go out and buy new homes. Yes, we have seen a bit of an increase in the number of new homes sold recently, but we are still a vast distance away from the level we were at before the last recession. And now mortgage rates are starting to rise steadily, and this is likely going to cause the number of new homes sold to start going back down. The chart below clearly shows us that the real estate market is far from healthy at this point…

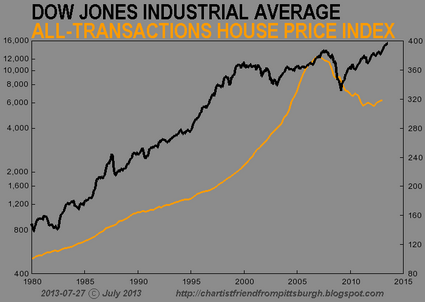

For most middle class Americans, their homes are their primary financial assets. So the fact that home prices have declined so much is absolutely devastating for many families. But stocks are primarily held by the top 5 percent of all Americans, and as the chart below shows, they have benefited greatly from the antics of the Federal Reserve in recent years…

There is no way in the world that the stock market should be this high. The economic fundamentals simply do not justify it. As a society, we consume far more than we produce, our debt is growing at an exponential pace, our economic infrastructure is being absolutely gutted and our financial system is a giant Ponzi scheme that could collapse at any time.

And no market can stay divorced from reality forever. At some point this bubble is going to burst, and when financial bubbles burst they tend to do so very rapidly.

As Marc Faber recently said, “one day, this financial bubble will have to adjust on the downside.”

When it does “adjust”, we are likely going to see a financial panic even worse than we witnessed back in 2008. Credit will freeze up, economic activity will grind to a standstill and millions of Americans will lose their jobs.

Don’t assume that the bubble of false prosperity that we are enjoying right now will last forever.

It won’t.

Use the time that you have right now to prepare for what is ahead.

A great storm is rapidly approaching, and I don’t see any way that it is going to be averted.