Do you want to know the primary reason why rapidly rising interest rates could take down the entire global financial system? Most people might think that it would be because the U.S. government would have to pay much more interest on the national debt. And yes, if the average rate of interest on U.S. government debt rose to just 6 percent (and it has actually been much higher in the past), the federal government would be paying out about a trillion dollars a year just in interest on the national debt. But that isn’t it. Nor does the primary reason have to do with the fact that rapidly rising interest rates would impose massive losses on bond investors. At this point, it is being projected that if U.S. bond yields rise by an average of 3 percentage points, it will cause investors to lose a trillion dollars. Yes, that is a 1 with 12 zeroes after it ($1,000,000,000,000). But that is not the number one danger posed by rapidly rising interest rates either. Rather, the number one reason why rapidly rising interest rates could cause the entire global financial system to crash is because there are more than 441 TRILLION dollars worth of interest rate derivatives sitting out there. This number comes directly from the Bank for International Settlements – the central bank of central banks. In other words, more than $441,000,000,000,000 has been bet on the movement of interest rates. Normally these bets do not cause a major problem because rates tend to move very slowly and the system stays balanced. But now rates are starting to skyrocket, and the sophisticated financial models used by derivatives traders do not account for this kind of movement.

Do you want to know the primary reason why rapidly rising interest rates could take down the entire global financial system? Most people might think that it would be because the U.S. government would have to pay much more interest on the national debt. And yes, if the average rate of interest on U.S. government debt rose to just 6 percent (and it has actually been much higher in the past), the federal government would be paying out about a trillion dollars a year just in interest on the national debt. But that isn’t it. Nor does the primary reason have to do with the fact that rapidly rising interest rates would impose massive losses on bond investors. At this point, it is being projected that if U.S. bond yields rise by an average of 3 percentage points, it will cause investors to lose a trillion dollars. Yes, that is a 1 with 12 zeroes after it ($1,000,000,000,000). But that is not the number one danger posed by rapidly rising interest rates either. Rather, the number one reason why rapidly rising interest rates could cause the entire global financial system to crash is because there are more than 441 TRILLION dollars worth of interest rate derivatives sitting out there. This number comes directly from the Bank for International Settlements – the central bank of central banks. In other words, more than $441,000,000,000,000 has been bet on the movement of interest rates. Normally these bets do not cause a major problem because rates tend to move very slowly and the system stays balanced. But now rates are starting to skyrocket, and the sophisticated financial models used by derivatives traders do not account for this kind of movement.

So what does all of this mean?

It means that the global financial system is potentially heading for massive amounts of trouble if interest rates continue to soar.

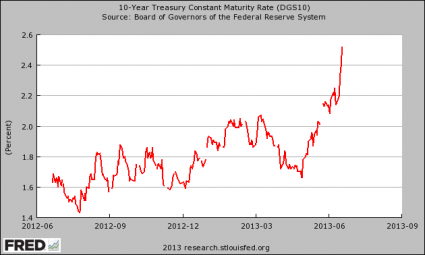

Today, the yield on 10 year U.S. Treasury bonds rocketed up to 2.66% before settling back to 2.55%. The chart posted below shows how dramatically the yield on 10 year U.S. Treasuries has moved in recent days…

Right now, the yield on 10 year U.S. Treasuries is about 30 percent above its 50 day moving average. That is the most that it has been above its 50 day moving average in 50 years.

Like I mentioned above, we are moving into uncharted territory and this data doesn’t really fit into the models used by derivatives traders.

The yield on 5 year U.S. Treasuries has been moving even more dramatically…

Last week, the yield on 5 year U.S. Treasuries rose by an astounding 37 percent. That was the largest increase in 50 years.

Once again, this is uncharted territory.

If rates continue to shoot up, there are going to be some financial institutions out there that are going to start losing absolutely massive amounts of money on interest rate derivative contracts.

So exactly what is an interest rate derivative?

The following is how Investopedia defines interest rate derivatives…

A financial instrument based on an underlying financial security whose value is affected by changes in interest rates. Interest-rate derivatives are hedges used by institutional investors such as banks to combat the changes in market interest rates. Individual investors are more likely to use interest-rate derivatives as a speculative tool – they hope to profit from their guesses about which direction market interest rates will move.

They can be very complicated, but I prefer to think of them in very simple terms. Just imagine walking into a casino and placing a bet that the yield on 10 year U.S. Treasuries will hit 2.75% in July. If it does reach that level, you win. If it doesn’t, you lose. That is a very simplistic example, but I think that it is a helpful one. At the heart of it, the 441 TRILLION dollar derivatives market is just a bunch of people making bets about which way interest rates will go.

And normally the betting stays very balanced and our financial system is not threatened. The people that run this betting use models that are far more sophisticated than anything that Las Vegas uses. But all models are based on human assumptions, and wild swings in interest rates could break their models and potentially start causing financial losses on a scale that our financial system has never seen before.

We are potentially talking about a financial collapse far worse than anything that we saw back in 2008.

Remember, the U.S. national debt is just now approaching 17 trillion dollars. So when you are talking about 441 trillion dollars you are talking about an amount of money that is almost unimaginable.

Meanwhile, China appears to be on the verge of another financial crisis as well. The following is from a recent article by Graham Summers…

China is on the verge of a “Lehman” moment as its shadow banking system implodes. China had pumped roughly $1.6 trillion in new credit (that’s 21% of GDP) into its economy in the last two quarters… and China GDP growth is in fact slowing.

This is what a credit bubble bursting looks like: the pumping becomes more and more frantic with less and less returns.

And Chinese stocks just experienced their largest decline since 2009. The second largest economy on earth is starting to have significant financial problems at the same time that our markets are starting to crumble.

Not good.

And don’t forget about Europe. European stocks have had a very, very rough month so far…

The narrow EuroStoxx 50 index is now at its lowest in over seven months (-5.4% year-to-date and -12.5% from its highs in May) and the broader EuroStoxx 600 is also flailing lower. The European bank stocks pushed down to their lowest in almost 10 months and are now in bear market territory – down 22.5% from their highs. Spain and Italy are now testing their lowest level in 9 months.

So are the central banks of the world going to swoop in and rescue the financial markets from the brink of disaster?

At this point it does not appear likely.

As I have written about previously, the Bank for International Settlements is the central bank for central banks, and it has a tremendous amount of influence over central bank policy all over the planet.

The other day, the general manager of the Bank for International Settlements, Jaime Caruana, gave a speech entitled “Making the most of borrowed time“. In that speech, he made it clear that the era of extraordinary central bank intervention was coming to an end. The following is one short excerpt from that speech…

“Ours is a call for acting responsibly now to strengthen growth and avoid even costlier adjustment down the road. And it is a call for recognizing that returning to stability and prosperity is a shared responsibility. Monetary policy has done its part. Recovery now calls for a different policy mix – with more emphasis on strengthening economic flexibility and dynamism and stabilizing public finances.”

Monetary policy has done its part?

That sounds pretty firm.

And if you read the entire speech, you will see that Caruana makes it clear that he believes that it is time for the financial markets to stand on their own.

But will they be able to?

As I wrote about yesterday, the U.S. financial system is a massive Ponzi scheme that is on the verge of imploding. Unprecedented intervention by the Federal Reserve has helped to prop it up for the last couple of years, and there is a lot of fear in the financial world about what is going to happen once that unprecedented intervention is gone.

So what happens next?

Well, nobody knows for sure, but one thing seems certain. The last half of 2013 is shaping up to be very, very interesting.