If this is what “the good times” look like, how nightmarish are “the bad times” going to be? In America today, more than 500,000 of us are homeless, about 40 million of us are living in poverty, 50 percent of all workers make less than $33,000 a year, and 70 percent of us have cried about money. But at least the economy has been “growing”, right? Well, in this article I would like to address that. Even if you believe that the highly manipulated economic growth numbers that the government puts out are legitimate, they still show that we are in one of the worst economic stretches in all of U.S. history.

If this is what “the good times” look like, how nightmarish are “the bad times” going to be? In America today, more than 500,000 of us are homeless, about 40 million of us are living in poverty, 50 percent of all workers make less than $33,000 a year, and 70 percent of us have cried about money. But at least the economy has been “growing”, right? Well, in this article I would like to address that. Even if you believe that the highly manipulated economic growth numbers that the government puts out are legitimate, they still show that we are in one of the worst economic stretches in all of U.S. history.

From 1930 to 1933, the U.S. economy experienced four years in a row during which GDP growth each year was under 3 percent.

Up until this current stretch, that was the longest streak in our entire history.

Of course we have absolutely shattered that old record, and now that 2019 is over we can add one more year to our growing total. At this point, you have to go back to 2005 to find the last year in which the U.S. economy grew by at least 3 percent.

That means that the U.S. economy has not actually had a “good year” since the middle of the Bush administration.

14 years in a row of economic growth below 3 percent is not anything to cheer about. In fact, it is downright abysmal.

But the good news is that stock prices have been steadily rising over the past decade. Just check out the numbers that David Wessel recently shared with PBS…

So, look, the stock market had a terrific decade. The S&P 500 rose nine out of 10 years. The S&P 500 is up nearly 30 percent this year, just this year alone. And half the stock market wealth in America is held by the top 1 percent of people.

The Federal Reserve created trillions of dollars out of thin air and pumped that money into the financial markets, and of course that was going to be good for stock prices. And pushing interest rates to the floor also helped inflate the massive bubble that we now see on Wall Street. The following bit of analysis comes from CNBC…

The Fed has kept borrowing rates low throughout the decade, gradually raising them from the end of 2015 through 2018, only to cut quickly again in 2019 to try to fend off any uncertainty in the economy. The central bank’s balance sheet sits at roughly $4 trillion, quadruple its size in 2008.

Needless to say, there is going to be a great price to pay in the long-term for such manipulation, but as long as stock prices keep rising most people don’t seem to care.

Unfortunately, these high stock prices do not represent any sort of permanent wealth. They are simply a snapshot of what people are willing to pay at this moment in time, and a major disaster could come along which could cut those prices in half by next month.

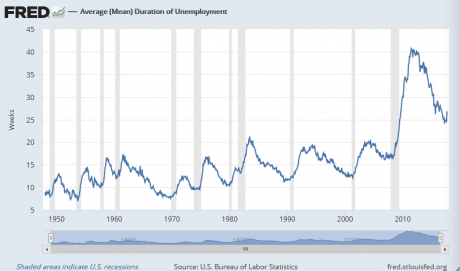

Economic optimists also like to point to the employment numbers as evidence that the economy is doing well, but those numbers are so manipulated that they are essentially meaningless at this point.

In fact, most of the people that are transitioning from not having a job to having a job each month did not even count as “unemployed” the month previously…

This year, the portion of people who got jobs each month who wouldn’t even have been counted among the unemployed the month before reached 75 percent. That’s by far the highest it’s been in the last three decades. The percentage of working-age Americans who have jobs only returned to its pre-Great Recession peak in the last few months. (It still has a ways to go before it returns to its previous peak, just before the 2001 recession.)

Today, more than 100 million working age Americans do not have a job, and John Williams has calculated that if honest numbers were being used that the real unemployment rate would be above 20 percent.

The truth is that we still have an employment crisis in this country, and anyone that suggests otherwise is not being straight with you.

Meanwhile, productivity growth has been absolutely terrible over the past decade, an increasing share of the economy has become concentrated in corporate hands, and small business creation has continued to collapse. The following comes from an excellent article by Annie Lowrey…

In many ways, the American economy became more sclerotic. Corporate concentration increased, with more industry sectors dominated by a small handful of firms. All the stories about the furious innovation coming from Silicon Valley and other tech-dominated regions aside, the start-up economy continued its long, slow collapse. The number of IPOs has fallen, and there are now half as many publicly listed businesses as there were in the late 1990s. Our cultural obsession with start-ups peaked at a time when companies under a year old were half as common as they were 40 years ago.

At the same time, the cost of living for average American families has been skyrocketing but our paychecks have not. As a result, more Americans are being squeezed out of the middle class with each passing month. Here is more from Lowrey…

Millions of young families who tried to save for a home were unable to purchase one, sapped by the toxic combination of high rents and a lack of stock. Throw in sky-high child-care prices, spiraling out-of-pocket health-care fees, and heavy educational-debt loads, and the 2010s crushed a whole generation as it entered its prime earning years. The Millennials are on track to be the first generation in contemporary history to end up poorer than their parents—unless Gen X beats them to it.

The only thing that has saved our economy from plunging into a horrific depression has been the greatest debt binge in all of human history.

Over the last ten years we have added more than 10 trillion dollars to the national debt, state and local government debt has soared to record highs all over the nation, corporate debt has risen more than 50 percent, student loan debt has more than doubled and the total amount of U.S. household debt is now nearing 14 trillion dollars.

By stealing from the future, we have been able to stabilize the present, but the long-term cost will be more than we can bear.

It is only a matter of time before our mistakes catch up with us, and the clock is ticking.

So please don’t try to tell me that the U.S. economy is in good shape.

The last decade was one of the worst stretches for economic growth in our history, and a day of reckoning awaits us during the decade that is directly ahead.

About the Author: I am a voice crying out for change in a society that generally seems content to stay asleep. My name is Michael Snyder and I am the publisher of The Economic Collapse Blog, End Of The American Dream and The Most Important News, and the articles that I publish on those sites are republished on dozens of other prominent websites all over the globe. I have written four books that are available on Amazon.com including The Beginning Of The End, Get Prepared Now, and Living A Life That Really Matters. (#CommissionsEarned) By purchasing those books you help to support my work. I always freely and happily allow others to republish my articles on their own websites, but due to government regulations I need those that republish my articles to include this “About the Author” section with each article. In order to comply with those government regulations, I need to tell you that the controversial opinions in this article are mine alone and do not necessarily reflect the views of the websites where my work is republished. This article may contain opinions on political matters, but it is not intended to promote the candidacy of any particular political candidate. The material contained in this article is for general information purposes only, and readers should consult licensed professionals before making any legal, business, financial or health decisions. Those responding to this article by making comments are solely responsible for their viewpoints, and those viewpoints do not necessarily represent the viewpoints of Michael Snyder or the operators of the websites where my work is republished. I encourage you to follow me on social media on Facebook and Twitter, and any way that you can share these articles with others is a great help.

America’s long-term “balance sheet numbers” just continue to get progressively worse. Unfortunately, since the stock market has been soaring and the GDP numbers look okay, most Americans assume that the U.S. economy is doing just fine. But the stock market was soaring and the GDP numbers looked okay just prior to the great financial crisis of 2008 as well, and we saw how that turned out. The truth is that GDP is not the best measure for the health of the economy. Judging the U.S. economy by GDP is basically like measuring the financial health of an individual by how much money he or she spends, and I will attempt to illustrate that in this article.

America’s long-term “balance sheet numbers” just continue to get progressively worse. Unfortunately, since the stock market has been soaring and the GDP numbers look okay, most Americans assume that the U.S. economy is doing just fine. But the stock market was soaring and the GDP numbers looked okay just prior to the great financial crisis of 2008 as well, and we saw how that turned out. The truth is that GDP is not the best measure for the health of the economy. Judging the U.S. economy by GDP is basically like measuring the financial health of an individual by how much money he or she spends, and I will attempt to illustrate that in this article.