Is the U.S. economy about to get slammed by a major recession? According to Gallup, U.S. economic confidence has soared to the highest level ever recorded, but meanwhile a whole host of key economic indicators are absolutely screaming that a new recession is beginning. And if the U.S. economy does officially enter recession territory in 2017, it certainly won’t be a shock, because the truth is that we are well overdue for one. Donald Trump has inherited quite an economic mess from Barack Obama, and it was probably inevitable that we were headed for a significant economic downturn no matter who won the election.

Is the U.S. economy about to get slammed by a major recession? According to Gallup, U.S. economic confidence has soared to the highest level ever recorded, but meanwhile a whole host of key economic indicators are absolutely screaming that a new recession is beginning. And if the U.S. economy does officially enter recession territory in 2017, it certainly won’t be a shock, because the truth is that we are well overdue for one. Donald Trump has inherited quite an economic mess from Barack Obama, and it was probably inevitable that we were headed for a significant economic downturn no matter who won the election.

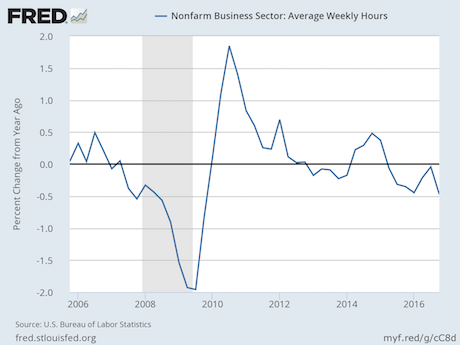

One of the key indicators to watch is average weekly hours. When the economy shifts into recession mode, employers tend to start cutting back hours, and that is happening right now. In fact, as Graham Summers has pointed out, we just witnessed the largest percentage decline in average weekly hours since the recession of 2008…

In addition to the decline in hours, Summers has suggested that there are a number of other reasons to believe that a new recession is here…

The fact is that the GDP growth of 4%-5% is not just around the corner. The US most likely slid into recession in the last three months. GDP growth collapsed in 4Q16, with a large portion of the “growth” coming from accounting gimmicks.

Consider the following:

- Tax receipts indicate the US is in recession.

- Gross private domestic investment indicates were are in a recession.

- Retailers are showing that the US consumer is tapped out (see AMZN’s recent miss).

- UPS, another economic bellweather, dramatically lowered 2017 forecasts.

To me, even more alarming is the tightening of lending standards. In our debt-based economy, the flow of credit is absolutely critical to economic growth, and when credit starts to get tight that almost always leads to a recession.

So the fact that lending standards have now tightened for medium and large sized firms for six quarters in a row is very bad news. The following comes from Business Insider…

“Although modest over the past couple of quarters, it is still worth noting that this is now the sixth quarter in succession that standards have tightened for large and medium sized firms,” Deutsche Bank economist Jim Reid wrote in a research note to clients.

“This usually only happens in recessions.”

Reid is 100 percent correct on this point. This is precisely the kind of thing that we would expect to see if a new recession was beginning, and if this trend continues it is hard to imagine that the U.S. economy will be able to continue to grow.

And it is interesting to note that job growth at S&P 500 companies has gone negative for the first time since the last recession, and so large firms are definitely starting to feel the pressure.

Simultaneously, lending standards are also tightening up for consumers…

“The most notable tightening in standards though was in consumer loans,” the Fed said. “During the quarter, banks reported an 8.3% net tightening in credit standards for credit cards and 11.6% net tightening for auto loans.”

US consumer spending accounts for more than two-thirds of economic activity and is thus a key driver of growth in the world’s largest economy.

Those numbers for credit cards and auto loans are major red flags.

It is very simple. Tighter credit means less economic activity which means slower economic growth. The U.S. economy grew at a dismal 1.9 percent annual rate during the 4th quarter of 2016, and it would be absolutely no surprise if we end up with a negative number for the first quarter of 2017.

One of the big reasons why lending standards are tightening is because bankruptcies are rising.

As I reported the other day, consumer bankruptcies just rose on a year-over-year basis in back to back months for the first time in almost seven years. Commercial bankruptcies had already been rising on a year-over-year basis throughout 2016, and so the fact that consumer bankruptcies have now joined the party is a very bad sign.

And we have also just learned that real median household income declined in 2016…

Its official! The spectacular Obama/Fed “recovery” produced no increase in real medin household income in 2016 (the last year of Obama’s reign of [economic] error). In fact, real median annual household income in December 2016 ($57,827) was 0.9 percent lower than in December 2015 ($58,356).

Yes, I understand that there is a tremendous amount of optimism out there right now because of Donald Trump.

But the truth is that it is literally going to take some sort of an economic miracle to avoid a recession.

And if a recession is going to happen anyway, the Trump administration should want it to occur as quickly as possible.

You see, if a recession starts a year from now, it will be much more difficult for Trump to blame it on Obama. But if a recession starts right now, he will definitely be able to argue that it happened because of the mess that he inherited from the last administration.

In addition, the sooner the next recession ends the sooner the next recovery can begin. If a recession is still going on during the 2020 campaign, that would be really bad for Trump, but if a recovery is well underway by then that would be really good for his chances.

If you doubt this, just go back and look at the 1984 campaign. After a very difficult recession, the U.S. economy bounced back strongly and Ronald Reagan was able to ride that momentum to an easy victory.

So this may sound very strange to many of you, but the truth is that if a new recession is coming Trump supporters should want it to happen as rapidly as possible.

Unfortunately, once a new recession begins it may not play out like recessions normally do. The U.S. government is 20 trillion dollars in debt, we are in the midst of one of the biggest stock market bubbles in history, and our planet is becoming more unstable with each passing day. So even though Trump is in the White House and Obama is gone, let there be no doubt that a catastrophic economic crisis could literally erupt at any moment. I continue to encourage my readers to do all that they can to get prepared, because those that are prepared in advance will have the best chance of successfully getting through what is coming.

Unfortunately, a lot of people out there seem to believe that all of our problems have somehow evaporated just because Donald Trump is now living in the White House.

That is simply not true, and we all need to be praying for guidance and wisdom for Trump and his team as they prepare to deal with the great challenges that are ahead for our nation.