In an age of “belt tightening” and “budget cuts”, you would think that government officials would be trying to spend our money wisely. Unfortunately, when it comes time to cut spending our politicians tend to do everything that they can to protect their own interests and their own pet projects, but they don’t seem to mind implementing cuts that deeply hurt military families, the poor and the elderly. The facts that you are about to read will likely upset you very much. The federal government and our state governments are wasting money in some of the most ridiculous ways imaginable. Meanwhile, we are being told that we don’t have any money for a lot of really important things. Our hard-earned tax dollars are being horribly mismanaged, and the American people deserve to hear the truth about this gross negligence.

In an age of “belt tightening” and “budget cuts”, you would think that government officials would be trying to spend our money wisely. Unfortunately, when it comes time to cut spending our politicians tend to do everything that they can to protect their own interests and their own pet projects, but they don’t seem to mind implementing cuts that deeply hurt military families, the poor and the elderly. The facts that you are about to read will likely upset you very much. The federal government and our state governments are wasting money in some of the most ridiculous ways imaginable. Meanwhile, we are being told that we don’t have any money for a lot of really important things. Our hard-earned tax dollars are being horribly mismanaged, and the American people deserve to hear the truth about this gross negligence.

Now before I go any further, I want to make it very clear that I believe that the federal government and our state governments are already taking in more than enough money. They should be able to do everything that they need to do on the money that they are already extracting from all of us. And if we had been living within our means all this time, we would not be drowning in debt as a nation today.

Unfortunately, our politicians did choose to go into tremendous amounts of debt, and the American people did not stop them. So now we are rapidly heading toward a debt crisis unlike anything the world has ever seen before.

And our politicians should be reducing spending. There is no question about that. But what this article is about is priorities, and right now our politicians really seem to have their priorities messed up. What follows are some examples of this…

The city of Detroit says that it is totally broke and has no money for pensions…

…but somehow the city has 444 million dollars to spend on a new hockey arena for the Detroit Red Wings.

Large numbers of federal employees have been hit with mandatory furloughs in 2013 due to the sequester…

…but somehow the federal government is able to spend tens of millions of dollars to fill our skies with surveillance drones.

The U.S. government is so broke that it has had to borrow more than a trillion dollars from China…

…but somehow we have plenty of money to help “modernize China’s energy grid“.

The U.S. Congress has cut $60,000,000 for schools on Indian reservations across the country…

…but somehow the IRS is able to pay out $70,000,000 in bonuses to their workers.

It is being projected that federal budget cuts will cost the U.S. economy 1.6 million jobs through the end of 2014…

…but somehow the federal government has plenty of money to provide many former members of Congress with six-figure annual incomes for life…

Members of Congress receive retirement benefits that are far more generous than those earned by the average worker, according to a recent Bankrate analysis.

Not only do congressional representatives and senators earn the guarantee of a monthly pension check — a benefit that has become increasingly rare for most U.S. workers — they also receive Social Security payments and can opt to pay into the federal Thrift Savings Plan, a 401(k) style-plan with fees that are far lower than most retirement plans.

As a result, longtime members of Congress can easily retire with six-figure annual incomes for life.

The Obama administration is forcing the U.S. Army to reduce the number of active combat brigades from 45 to 33…

…but the Obama administration has no problem finding millions of dollars to send to radical jihadist Syrian rebels that are beheading innocent Christians over in Syria.

Barack Obama says that there simply is not any money available for White House tours…

…but the Obamas are able to spend hundreds of millions of dollars on exotic vacations. In August, Obama and his family will be spending 8 days in a beautiful home on the Massachusetts island of Martha’s Vineyard.

The federal government says that there was not enough money for the traditional 4th of July fireworks at many military bases around the country this year…

…but somehow the National Institutes of Health has $509,840 to spend on “a study that will send text messages in ‘gay lingo’ to methamphetamine addicts to try to persuade them to use fewer drugs and more condoms.”

Due to “budget cuts”, swimming pools for military families are being shut down all over the country…

…but Barack Obama felt that it was so important to send $500,000,000 to the Palestinian Authority that he signed a national security executive order last Friday that enabled him to get around an act of Congress that was intended to prevent him from sending that money to them.

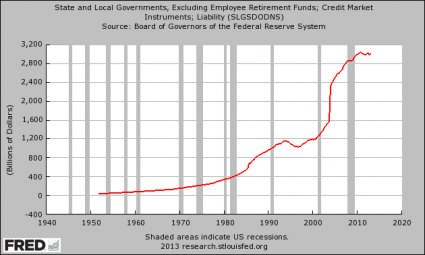

The state of California is so strapped for cash that it may have to release thousands of violent criminals back on to the streets…

…but somehow the state of California has plenty of money to provide a multitude of welfare benefits for illegal immigrants.

A total of about 38 million dollars is being cut from “meals on wheels” programs around the nation due to the sequester…

…but somehow the federal government has plenty of money to hassle ordinary citizens with ridiculous amounts of red tape. For example, a small-time magician out in Missouri that does magic shows for kids was recently forced to submit a 32 page “disaster plan” for the rabbit that he uses in his shows.

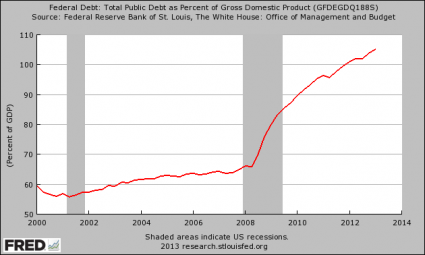

With priorities like this, is it any wonder that our national debt is completely and totally out of control?

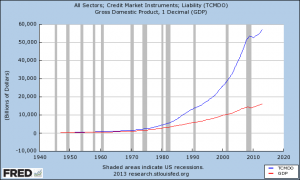

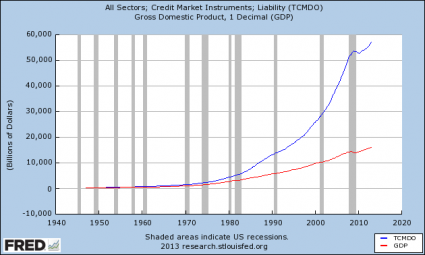

If the U.S. national debt was reduced to a stack of one dollar bills, it would stretch from the earth to the moon five times. It would circle the earth at the equator 45 times.

If our politicians would have been spending our money wisely all of these years, we would have enough money to do the essential things that the government should be doing.

But instead, our money has been wasted in some of the most bizarre ways imaginable, and yet the American people just continue to sit back and allow our politicians to flush our money down the toilet.

So what do you think about all of this? Are there any additional examples that you would add to the list above? Please feel free to share what you think by posting a comment below…