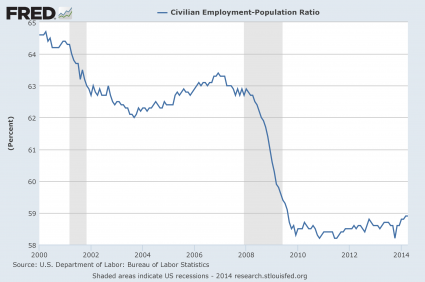

Those that were hoping for an “economic renaissance” in the United States got some more bad news this week. It turns out that the U.S. economy is in significantly worse shape than the experts were projecting. Retail sales unexpectedly declined in March, total business sales have fallen again, and the inventory to sales ratio has hit the highest level since the last financial crisis. When you add these three classic recession signals to the 19 troubling numbers about the U.S. economy that I wrote about last week, it paints a very disturbing picture. Virtually all of the signs that we would expect to pop up during the early chapters of a major economic crisis have now appeared, and yet most Americans still appear to be clueless about what is happening.

Those that were hoping for an “economic renaissance” in the United States got some more bad news this week. It turns out that the U.S. economy is in significantly worse shape than the experts were projecting. Retail sales unexpectedly declined in March, total business sales have fallen again, and the inventory to sales ratio has hit the highest level since the last financial crisis. When you add these three classic recession signals to the 19 troubling numbers about the U.S. economy that I wrote about last week, it paints a very disturbing picture. Virtually all of the signs that we would expect to pop up during the early chapters of a major economic crisis have now appeared, and yet most Americans still appear to be clueless about what is happening.

Even I was surprised when the government reported that retail sales had actually fallen in March. Consumer spending is a very large part of our economy, and so if consumer spending is slowing down already that certainly does not bode well for the rest of 2016. The following comes from highly respected author Jim Quinn…

The Ivy League educated “expert” economists expected March retail sales to increase by 0.1%. They only missed by $6 billion, as retail sales FELL by 0.3%. They have fallen for three straight months. At least gasoline sales were strong, as prices have risen 22% since mid-February. That should do wonders for the finances of American households. If you exclude gasoline sales, retail sales fell by 0.4%. As the chart below reveals, the year over year change in retail sales has been at or near recessionary levels for most of 2015, and into 2016.

You can view the chart that he was referring to right here. In addition to a decline in retail sales, total business sales have also been falling, and this is another classic recession signal. The following comes from Wolf Richter…

Total business sales fell again in February, the Commerce Department reported today. They include sales by manufacturers, retailers, and wholesalers of all sizes across the US economy. This measure is far broader than the aggregate sales by publicly traded companies, which too have been falling.

At $1.284 trillion in February, total business sales were down an estimated 0.4% from January, adjusted for seasonal and trading-day differences but not for price changes. And they were down 1.4% from the already beaten-down levels of February last year. They’re back where they’d first been in November 2012!

Yes, the stock market has been on quite a run for the past several weeks, but that temporary rebound is not based on the economic fundamentals.

The truth is that the real economy is definitely starting to slow down substantially. If you want to break it down very simply, less stuff is being bought and sold and shipped around the country, and that tells us far more about what is coming in the months ahead than the temporary ups and downs of stock prices.

Another huge red flag is the fact that the inventory to sales ratio in the U.S. has hit the highest level that we have seen since the last financial crisis…

The crucial inventory-to-sales ratio, which tracks how long unsold inventory sits around in relationship to sales, is now at a mind-bending 1.41. That’s the level the ratio spiked to in November 2008, after the Lehman bankruptcy in September had put the freeze on the economy.

Inventories represent prior sales by suppliers. When companies try to reduce their inventories, they cut their orders. Suppliers see these orders as sales. As their sales slump, suppliers adjust by cutting their own orders, thus causing the sales slump to propagate up the supply chain. They all react by cutting their expenses. And if it lasts, they’ll cut jobs. Inventory corrections have a nasty impact on the overall economy.

Because sales have slowed down, inventories are starting to pile up to alarmingly high levels. And when companies see that business is slowing down, they start to let people go.

In a previous article, I told my readers that Challenger, Gray & Christmas is reporting that job cut announcements at major firms in the United States are up 32 percent during the first quarter of 2016 compared to the first quarter of 2015.

Somehow, most of the talking heads on television don’t seem too alarmed by this.

But ordinary Americans are beginning to become alarmed about what is happening. In fact, the percentage of Americans that believe that the U.S. economy is “getting worse” is now the highest it has been since last August…

One of the more glaring examples of how strong pessimism has become is Gallup’s U.S. Economic Confidence Index. The measure gauges the difference between respondents who say the economy is improving or declining. The most recent results are not good.

Fully 59 percent say the economy is “getting worse” against just 37 percent who say it is “getting better.” That gap of 22 percentage points is the worst since August, according to Gallup, which polled 3,542 adults.

Personally, I thought that we would be a little further down the road by now, but without a doubt a new economic downturn has begun in America.

So far, it is less severe than what most of the rest of the planet is experiencing. Japan’s GDP is officially shrinking, major banks are failing all over Europe, and even CNN admits that what is going on down in Brazil is an “economic collapse”.

It’s funny – yesterday I took time out to write an article about the horrible suffering that ISIS sex slaves are enduring, and a few of my critics took that as a sign that there must not be enough bad economic news to write about.

Well, the truth is that this isn’t the case at all. The global economic meltdown is steaming along, even if it is moving just a little bit slower than many of us had originally anticipated. We are moving in the exact direction that myself and many others had warned about, and the rest of 2016 is looking quite ominous for the global economy.

So hopefully everyone (including the critics) is using whatever time we have left wisely. Because I definitely wish the very best for everyone during the exceedingly hard times that are coming.

*About the author: Michael Snyder is the founder and publisher of The Economic Collapse Blog. Michael’s controversial new book about Bible prophecy entitled “The Rapture Verdict” is available in paperback and for the Kindle on Amazon.com.*