Corporations, individuals and the federal government continue to rack up debt at a rate that is far faster than the overall rate of economic growth. We are literally drowning in red ink from sea to shining sea, and yet we just can’t help ourselves. Consumer credit has doubled since the year 2000. Student loan debt has doubled over the course of the past decade. Business debt has doubled since 2006. And of course the debt of the federal government has doubled since 2007. Anyone that believes that this is “sustainable” in any way, shape or form is crazy. We have accumulated the greatest mountain of debt that the world has ever seen, and yet despite all of the warnings we just continue to race forward into financial oblivion. There is no possible way that this is going to end well.

Corporations, individuals and the federal government continue to rack up debt at a rate that is far faster than the overall rate of economic growth. We are literally drowning in red ink from sea to shining sea, and yet we just can’t help ourselves. Consumer credit has doubled since the year 2000. Student loan debt has doubled over the course of the past decade. Business debt has doubled since 2006. And of course the debt of the federal government has doubled since 2007. Anyone that believes that this is “sustainable” in any way, shape or form is crazy. We have accumulated the greatest mountain of debt that the world has ever seen, and yet despite all of the warnings we just continue to race forward into financial oblivion. There is no possible way that this is going to end well.

Just the other day, a financial story that USA Today posted really got my attention. It contained charts and graphs that showed that business debt in the U.S. had doubled since 2006. I knew that things were bad, but I didn’t know that they were this bad. Back in 2006, just prior to the last major economic downturn, U.S. nonfinancial companies had a total of about 2.6 trillion dollars of debt. Now, that total has skyrocketed to 5.8 trillion…

Companies are sitting on a record $1.82 trillion in cash. That might sound impressive until you hear companies owe three times more – $5.8 trillion, according to a new report from Standard & Poor’s Ratings Services.

Debt levels are soaring at U.S. non-financial companies so quickly – total debt outstanding rose $650 billion in 2014, which is six times faster than the $100 billion in added cash.

So are we in better condition to handle an economic crisis than we were the last time, or are we in worse shape?

Let’s look at another category of debt. According to new data that just came out, the total amount of student loan debt in the U.S. is up to a staggering 1.2 trillion dollars. That total has more than doubled over the past decade…

New data released by The Associated Press shows student loan debt is over $1.2 trillion, which is more than double the amount of a decade ago.

Students are facing an average of $35,000 in debt, that’s the highest of any graduating class in U.S. history. A senior at University of Colorado, Colorado Springs, Jon Cheek, knows the struggle first hand.

“It’s been a pretty big concern, I work while I go to school. I applied for a bunch of scholarships and done everything I can to try and keep it low,” said Cheek.

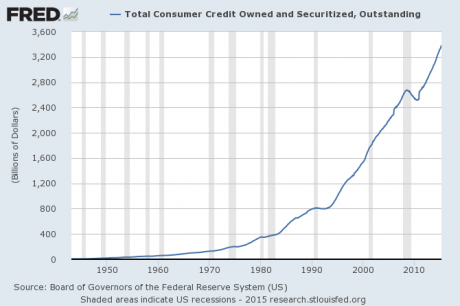

And of course it isn’t just student loan debt. American consumers have had a love affair with debt that stretches back for decades. As the chart below demonstrates, overall consumer credit has more than doubled since the year 2000…

If our paychecks were increasing at this same pace, that would be one thing. But they aren’t. In fact, real median household income is actually lower today than it was just prior to the last economic crisis.

So American households should actually be cutting back on debt. But instead, they are just piling on more debt, and the financial predators are becoming even more creative. In a previous article, I discussed how many auto loans are now being stretched out for seven years. At this point, the number of auto loans that exceed 72 months is at an all-time high…

The average new car loan has reached a record 67 months, reports Experian, the Ireland-based information-services company. The percentage of loans with terms of 73 to 84 months also reached a new high of 29.5% in the first quarter of 2015, up from 24.9% a year earlier.

Long-term used-vehicle loans also broke records with loan terms of 73 to 84 months reaching 16% in the first quarter 2015, up from 12.94% — also the highest on record.

When will we learn?

The crash of 2008 should have been a wake up call.

We should have acknowledged our mistakes and we should have started doing things very differently.

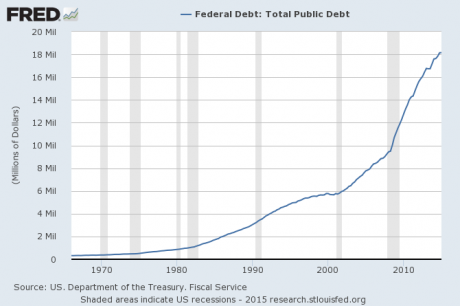

But instead, we just kept on making the exact same mistakes. In fact, our long-term financial problems have continued to accelerate since the last recession. Just look at what has happened to our national debt. Just prior to the last recession, the U.S. national debt was sitting at approximately 9 trillion dollars. Today, it is over 18 trillion dollars…

Our debt has grown so large that we will never be able to get out from under it. This is something that I covered in my recent article entitled “It Is Mathematically Impossible To Pay Off All Of Our Debt“. Because of our recklessness, our children, our grandchildren and all future generations of Americans are consigned to a lifetime of debt slavery. What we have done to them is beyond criminal. If we lived in a just society, a whole bunch of people would be going to prison for the rest of their lives over this.

During fiscal year 2014, the debt of the federal government increased by more than a trillion dollars. But in addition to that, the federal government has more than seven trillion dollars of debt that must be “rolled over” every year. In other words, the government must issue more than seven trillion dollars of new debt just to pay off old debts that are coming due.

As long as the rest of the world continues to lend us enormous mountains of money at ridiculously low interest rates, we can continue to keep our heads above the water. But this can change at any time. And once it does, interest rates will rise. If the average rate of interest on U.S. government debt was to return to the long-term average, we would very quickly find ourselves spending more than a trillion dollars a year just on interest on the national debt.

The debt-fueled prosperity that we are enjoying now is not real. It is a false prosperity that has been purchased by selling future generations into debt slavery. We have mortgaged the future to make our own lives better.

We are addicts. We are addicted to debt, and no matter how many warnings we receive, we just can’t help ourselves.

Shame on you America.