Did you know that the greatest period of economic growth in American history was during a time when there was absolutely no federal income tax? Between the end of the Civil War and 1913, there was an explosion of economic activity in the United States unlike anything ever seen before or since. Unfortunately, a federal income tax was instituted in 1913, and this year it turned 100 years old. But there was no fanfare, was there? There was no celebration because the federal income tax is universally hated. Sadly, most Americans just assume that there is no other option to an income tax. Most Americans just assume that it has always been with us and that it will always be with us. This year, the American people will shell out approximately $4.22 trillion in state and federal income taxes. That amount is equivalent to approximately 29.4 percent of all income that Americans will bring in this year, and that does not even take into account the dozens of other taxes that Americans pay each year. At this point, the U.S. tax code is about 13 miles long, and those that are honest and pay their taxes every year are being absolutely shredded by this system. But wouldn’t the federal government go broke if we didn’t have a federal income tax? No, actually the truth is that the federal government did just fine before there was an income tax. In fact, the U.S. national debt has gotten more than 5000 times larger since the federal income tax and the Federal Reserve were created by Congress back in 1913. As I have written about previously, the Federal Reserve system was actually designed to trap the United States in a debt spiral from which it could never possibly escape, and the federal income tax was needed to greatly expand the size of the federal government and to soak the American people of the funds necessary to service that debt. But it doesn’t have to be this way. America was once much better off before the income tax and the Federal Reserve were created, and we could easily go to such a system again.

Did you know that the greatest period of economic growth in American history was during a time when there was absolutely no federal income tax? Between the end of the Civil War and 1913, there was an explosion of economic activity in the United States unlike anything ever seen before or since. Unfortunately, a federal income tax was instituted in 1913, and this year it turned 100 years old. But there was no fanfare, was there? There was no celebration because the federal income tax is universally hated. Sadly, most Americans just assume that there is no other option to an income tax. Most Americans just assume that it has always been with us and that it will always be with us. This year, the American people will shell out approximately $4.22 trillion in state and federal income taxes. That amount is equivalent to approximately 29.4 percent of all income that Americans will bring in this year, and that does not even take into account the dozens of other taxes that Americans pay each year. At this point, the U.S. tax code is about 13 miles long, and those that are honest and pay their taxes every year are being absolutely shredded by this system. But wouldn’t the federal government go broke if we didn’t have a federal income tax? No, actually the truth is that the federal government did just fine before there was an income tax. In fact, the U.S. national debt has gotten more than 5000 times larger since the federal income tax and the Federal Reserve were created by Congress back in 1913. As I have written about previously, the Federal Reserve system was actually designed to trap the United States in a debt spiral from which it could never possibly escape, and the federal income tax was needed to greatly expand the size of the federal government and to soak the American people of the funds necessary to service that debt. But it doesn’t have to be this way. America was once much better off before the income tax and the Federal Reserve were created, and we could easily go to such a system again.

What we desperately need to do is to teach the American people a little history lesson. The truth is that the greatest period of economic growth in U.S. history was between the Civil War and 1913 when there was no federal income tax at all. The following is from Wikipedia…

The Gilded Age saw the greatest period of economic growth in American history. After the short-lived panic of 1873, the economy recovered with the advent of hard money policies and industrialization. From 1869 to 1879, the US economy grew at a rate of 6.8% for real GDP and 4.5% for real GDP per capita, despite the panic of 1873. The economy repeated this period of growth in the 1880s, in which the wealth of the nation grew at an annual rate of 3.8%, while the GDP was also doubled.

Sadly, most Americans cannot even conceive of an economy like that. Most Americans cannot even imagine having a nation without a massively bloated federal government and without an unelected central bank centrally planning our financial system.

But you know what?

It worked. In fact, it worked fantastically well.

The period between the Civil War and 1913 propelled the United States to greatness. Just check out all of the good things that Wikipedia says happened for the U.S. economy during those years…

The rapid economic development following the Civil War laid the groundwork for the modern U.S. industrial economy. By 1890, the USA leaped ahead of Britain for first place in manufacturing output.

An explosion of new discoveries and inventions took place, a process called the “Second Industrial Revolution.” Railroads greatly expanded the mileage and built stronger tracks and bridges that handled heavier cars and locomotives, carrying far more goods and people at lower rates. Refrigeration railroad cars came into use. The telephone, phonograph, typewriter and electric light were invented. By the dawn of the 20th century, cars had begun to replace horse-drawn carriages.

Parallel to these achievements was the development of the nation’s industrial infrastructure. Coal was found in abundance in the Appalachian Mountains from Pennsylvania south to Kentucky. Oil was discovered in western Pennsylvania; it was mainly used for lubricants and for kerosene for lamps. Large iron ore mines opened in the Lake Superior region of the upper Midwest. Steel mills thrived in places where these coal and iron ore could be brought together to produce steel. Large copper and silver mines opened, followed by lead mines and cement factories.

In 1913 Henry Ford introduced the assembly line, a step in the process that became known as mass-production.

But if we didn’t have an income tax, how did we fund the government? Well, we mostly did it with tariffs and excise taxes. The following is from a recent article by Thomas R. Eddlem…

Prior to ratification of the 16th (income tax) Amendment in February 1913, the federal government managed its few constitutional responsibilities without an income tax, except during the Civil War period. During peacetime, it did so largely — or even entirely — on import taxes called “tariffs.” Congress could afford to run the federal government on tariffs alone because federal responsibilities did not include welfare programs, agricultural subsidies, or social insurance programs like Social Security or Medicare. After the Civil War, tariff revenues sometimes suffered under a protectionist policy ushered in by the Republican Party that supplemented federal income via excises on alcohol, tobacco, and inheritances. But before the war, the need for tariff revenue to finance the federal government generally kept the tariff at reasonable levels. During wartime throughout early American history, the Founding Fathers were able to raise additional revenue employing a different method of direct taxation authorized by the U.S. Constitution prior to the 16th Amendment. These alternative taxing methods gave the young American nation embarrassing peacetime budget surpluses that several times came close to paying off the national debt.

So why didn’t we stick with that system?

Well, early in the 20th century the “progressives” and the social planners started to take control in Washington.

And one of the things that “progressives” and social planners love is an income tax. In fact, the second plank of the Communist Manifesto is a “heavy progressive or graduated income tax”.

Of course they promised us that income tax rates would always remain low. And at first they were quite low. The following is from an article by Adam Young…

The presidential election of 1912 was contested between three advocates of an income tax. The winner, Woodrow Wilson, after the ratification of the Sixteenth Amendment, called a special session of Congress in April 1913, which proceeded to pass an income tax of 1% on incomes above $3,000 and applied surcharges between 2% and 7% on income from $20,000 to $500,000.

But once the “progressives” and the social planners get their feet in the door, they always want more.

And we have seen how things have worked out. Today, the American people are being taxed into oblivion.

In a previous article entitled “Show This To Anyone That Believes That Taxes Are Too Low“, I listed dozens of other taxes that the American people pay each year in addition to federal and state income taxes…

#1 Building Permit Taxes

#2 Capital Gains Taxes

#3 Cigarette Taxes

#4 Court Fines (indirect taxes)

#5 Dog License Taxes

#6 Drivers License Fees (another form of taxation)

#7 Federal Unemployment Taxes

#8 Fishing License Taxes

#9 Food License Taxes

#10 Gasoline Taxes

#11 Gift Taxes

#12 Hunting License Taxes

#13 Inheritance Taxes

#14 Inventory Taxes

#15 IRS Interest Charges (tax on top of tax)

#16 IRS Penalties (tax on top of tax)

#17 Liquor Taxes

#18 Luxury Taxes

#19 Marriage License Taxes

#20 Medicare Taxes

#21 Medicare Tax Surcharge On High Earning Americans Under Obamacare

#22 Obamacare Individual Mandate Excise Tax (if you don’t buy “qualifying” health insurance under Obamacare you will have to pay an additional tax)

#23 Obamacare Surtax On Investment Income (a new 3.8% surtax on investment income that goes into effect next year)

#24 Property Taxes

#25 Recreational Vehicle Taxes

#26 Toll Booth Taxes

#27 Sales Taxes

#28 Self-Employment Taxes

#29 School Taxes

#30 Septic Permit Taxes

#31 Service Charge Taxes

#32 Social Security Taxes

#33 State Unemployment Taxes (SUTA)

#34 Tanning Tax (a new Obamacare tax on tanning services)

#35 Telephone Federal Excise Taxes

#36 Telephone Federal Universal Service Fee Taxes

#37 Telephone Minimum Usage Surcharge Taxes

#38 Telephone State And Local Taxes

#39 Tire Taxes

#40 Tolls (another form of taxation)

#41 Traffic Fines (indirect taxation)

#42 Utility Taxes

#43 Vehicle Registration Taxes

#44 Workers Compensation Taxes

Yet even with all of these taxes, our local governments, our state governments and our federal government are all absolutely drowning in debt.

In another previous article entitled “24 Outrageous Facts About Taxes In The United States That Will Blow Your Mind“, I listed a number of reasons why our federal income tax system has become a complete and utter abomination that can never be fixed…

1 – The U.S. tax code is now 3.8 million words long. If you took all of William Shakespeare’s works and collected them together, the entire collection would only be about 900,000 words long.

2 – According to the National Taxpayers Union, U.S. taxpayers spend more than 7.6 billion hours complying with federal tax requirements. Imagine what our society would look like if all that time was spent on more economically profitable activities.

3 – 75 years ago, the instructions for Form 1040 were two pages long. Today, they are 189 pages long.

4 – There have been 4,428 changes to the tax code over the last decade. It is incredibly costly to change tax software, tax manuals and tax instruction booklets for all of those changes.

5 – According to the National Taxpayers Union, the IRS currently has 1,999 different publications, forms, and instruction sheets that you can download from the IRS website.

6 – Our tax system has become so complicated that it is almost impossible to file your taxes correctly. For example, back in 1998 Money Magazine had 46 different tax professionals complete a tax return for a hypothetical household. All 46 of them came up with a different result.

7 – In 2009, PC World had five of the most popular tax preparation software websites prepare a tax return for a hypothetical household. All five of them came up with a different result.

8 – The IRS spends $2.45 for every $100 that it collects in taxes.

9 – According to The Tax Foundation, the average American has to work until April 17th just to pay federal, state, and local taxes. Back in 1900, “Tax Freedom Day” came on January 22nd.

10 – When the U.S. government first implemented a personal income tax back in 1913, the vast majority of the population paid a rate of just 1 percent, and the highest marginal tax rate was just 7 percent.

11 – Residents of New Jersey pay $1.64 in taxes for every $1.00 of federal spending that they get back.

12 – The United States is the only nation on the planet that tries to tax citizens on what they earn in foreign countries.

13 – According to Forbes, the 400 highest earning Americans pay an average federal income tax rate of just 18 percent.

14 – Warren Buffett had an effective tax rate of just 17.4 percent for 2010.

15 – The top 20 percent of all income earners in the United States pay approximately 86 percent of all federal income taxes.

16 – Sadly, as Bill Whittle has shown, you could take every single penny that every American earns above $250,000 and it would only fund about 38 percent of the federal budget.

17 – The United States has the highest corporate tax rate in the world (35 percent). In Ireland, the corporate tax rate is only 12.5 percent. This is causing thousands of corporations to move operations out of the United States and into other countries.

18 – Some tax havens are doing a booming business in setting up sham headquarters for U.S. corporations. For example, the city of Zug, Switzerland only has a population of 26,000 people but it is the headquarters for 30,000 companies.

19 – In 1950, corporate taxes accounted for about 30 percent of all federal revenue. In 2012, corporate taxes will account for less than 7 percent of all federal revenue.

The wealthy have become absolute masters at avoiding taxes, and the poor are not able to pay much.

So who always gets squeezed?

The middle class does.

No matter what our politicians promise us, the hammer is always brought down on the middle class.

And now, according to The Huffington Post, the IRS says that it can even read our old emails without a warrant to make sure that we are paying all of the taxes that we should be…

The IRS apparently interprets that authority very broadly, the documents show: as long as you’ve stored your email in a cloud service like Google Mail, and as long as those emails haven’t been deleted after a few months, the agency thinks it doesn’t need a warrant to read them.

The idea of IRS agents poking through your email account might sound at the very least creepy, and maybe unconstitutional. But the IRS does have a legal leg to stand on: the Electronic Communications Privacy Act of 1986 allows government agencies to in many cases obtain emails older than 180 days without a warrant.

That’s why an internal 2009 IRS document claimed that “the government may obtain the contents of electronic communication that has been in storage for more than 180 days” without a warrant.

It should be noted that the IRS is claiming that it does not use emails “to target” specific taxpayers, but notice that they are not promising not to use old emails against taxpayers once they are officially being audited or investigated…

“Contrary to some suggestions, the IRS does not use emails to target taxpayers. Any suggestion to the contrary is wrong.”

In any event, the truth is that we have one of the most complicated and one of the most intrusive tax systems in the history of the world.

Don’t the American people deserve better?

What do you think?

Should America go back to a system where there is no income tax and no Federal Reserve?

Please feel free to share what you think by leaving a comment below…

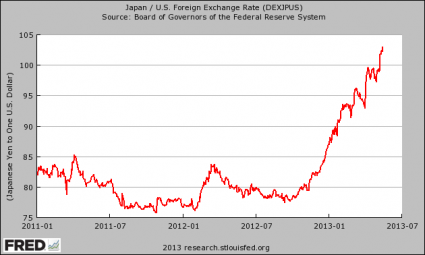

How much is 1,000,000,000,000,000 yen worth? Well, a quadrillion yen is worth approximately 10.5 trillion dollars. It is an amount of money that is larger than the “the economies of Germany, France and the U.K. combined“. It is such an astounding amount of debt that it is hard to even get your mind around it. The government debt to GDP ratio in Japan will reach 247 percent this year, and the Japanese currently spend about 50 percent of all central government tax revenue on debt service. Realistically, there are only two ways out of this overwhelming debt trap for the Japanese. Either they default or they try to inflate the debt away. At this point, the Japanese have chosen to try to inflate the debt away. They have initiated the greatest quantitative easing experiment that a major industrialized nation has attempted since the days of the Weimar Republic. Over the next two years, the Bank of Japan plans to zap 60 trillion yen into existence out of thin air and use it to buy government bonds. By the time this program is over, the monetary base in Japan will have approximately doubled. But authorities in Japan are desperate. They know that the Japanese debt bomb could set off global panic at any time, and they are trying to find a way out that will not cause too much pain.

How much is 1,000,000,000,000,000 yen worth? Well, a quadrillion yen is worth approximately 10.5 trillion dollars. It is an amount of money that is larger than the “the economies of Germany, France and the U.K. combined“. It is such an astounding amount of debt that it is hard to even get your mind around it. The government debt to GDP ratio in Japan will reach 247 percent this year, and the Japanese currently spend about 50 percent of all central government tax revenue on debt service. Realistically, there are only two ways out of this overwhelming debt trap for the Japanese. Either they default or they try to inflate the debt away. At this point, the Japanese have chosen to try to inflate the debt away. They have initiated the greatest quantitative easing experiment that a major industrialized nation has attempted since the days of the Weimar Republic. Over the next two years, the Bank of Japan plans to zap 60 trillion yen into existence out of thin air and use it to buy government bonds. By the time this program is over, the monetary base in Japan will have approximately doubled. But authorities in Japan are desperate. They know that the Japanese debt bomb could set off global panic at any time, and they are trying to find a way out that will not cause too much pain.