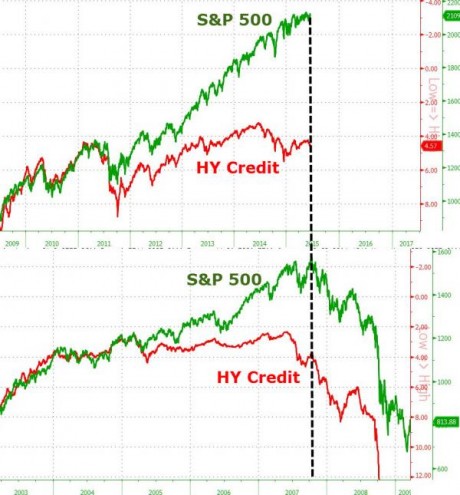

Are we right on the verge of one of the greatest financial collapses in American history? I have been repeatedly warning that our ridiculously over-inflated stock market bubble could burst at any time, but former Federal Reserve Chairman Alan Greenspan believes that the bond bubble actually presents an even greater danger. When you look at the long-term charts, you will see that an epic bond bubble has been growing since the early 1980s, and when it finally collapses the financial carnage is going to be unlike anything we have ever seen before.

Are we right on the verge of one of the greatest financial collapses in American history? I have been repeatedly warning that our ridiculously over-inflated stock market bubble could burst at any time, but former Federal Reserve Chairman Alan Greenspan believes that the bond bubble actually presents an even greater danger. When you look at the long-term charts, you will see that an epic bond bubble has been growing since the early 1980s, and when it finally collapses the financial carnage is going to be unlike anything we have ever seen before.

Since the last financial crisis, global central banks have purchased trillions of dollars worth of bonds, and this has pushed interest rates to absurdly low levels. But of course this state of affairs cannot go on indefinitely, and Greenspan is extremely concerned about what will happen when interest rates start going in the other direction…

Former Federal Reserve Chairman Alan Greenspan issued a bold warning Friday that the bond market is on the cusp of a collapse that also will threaten stock prices.

In a CNBC interview, the longtime central bank chief said the prolonged period of low interest rates is about to end and, with it, a bull market in fixed income that has lasted more than three decades.

“The current level of interest rates is abnormally low and there’s only one direction in which they can go, and when they start they will be rather rapid,” Greenspan said on “Squawk Box.”

And of course Greenspan is far from alone. In recent months there have been a whole host of prominent voices warning about the devastation that will take place when the bond market begins to shift. For example, the following comes from Nasdaq.com…

Advisors and investors beware, the long-swelling bubble in the bond market looks set to pop. Major bond investors are as worried as they have ever been, mostly because of the reduction in easing that is finally coming to markets. Central banks are letting off the gas pedal for the first time in almost a decade, which could have a devastating effect on the bond market. According to the head of fixed income at JP Morgan Asset Management, who oversees almost half a trillion in AUM, “The next 18 months are going to be incredibly challenging. I am not an equity investor, but I can just imagine how equity investors felt in 1999, during the dotcom bubble”. He continued, “Right now, central banks are printing money at a rate of around $1.5tn per year. That is a lot of money going into bonds. By this time next year, we think this will turn negative”.

So how will we know when a crisis is imminent?

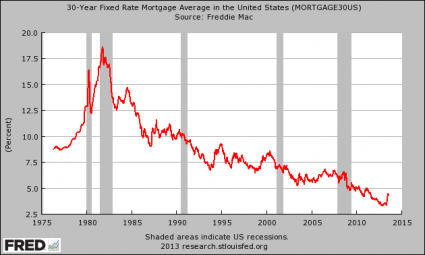

Some analysts are telling us to watch the 30-year yield. When it finally moves above its “mega moving average” and stays there, that will be a major red flag…

It’s still too soon to tell, but this could be the beginning of a realignment with both rates getting in sync again. This will not be confirmed, however, until the 30-year yield rises and stays above its mega moving average, currently at 3.18%.

As you know, this moving average is super important.

It’s identified and confirmed the mega downtrend in long-term interest rates ever since the 1980s. In other words, it doesn’t change often. So, if this trend were to change and turn up, it would be a huge deal.

Today, the 30-year yield moved up to 2.83 percent, and so we aren’t too far away.

There are so many prominent voices that are warning of imminent financial disaster, but there are others that believe that we have absolutely nothing to be concerned about. In fact, Jim Paulsen just told CNBC that he believes that this current bull market “could continue to forever”…

The stock market “has an awful good gig going,” with the economic recovery reaching all corners of the globe and U.S. inflation and interest rates still at historic lows, Leuthold Chief Investment Strategist Jim Paulsen told CNBC on Friday.

“We’ve got a fully employed economy, rising real wages. We restarted the corporate earnings cycle. We’ve got strong confidence among business and consumers,” he said on “Squawk Box.”

“The kick is we can do all of this without aggravating inflation and interest rates,” he said. “If that’s going to continue, I think the bull market could continue to forever.”

I think that Paulsen will end up deeply regretting those words.

No bull market lasts forever, and analysts at Goldman Sachs are warning that there is a 99 percent chance that stock market returns will be sub-optimal over the next decade.

But most people believe what they want to believe no matter what the facts may say, and Paulsen apparently wants to believe that things will never be bad for the financial markets ever again.

In the aftermath of the financial crisis of 2008, the powers that be decided to patch the old system up. Instead of addressing the root causes of the crisis, they chose to paper over our problems instead, and now we are in the terminal phase of the biggest financial bubble in history.

This time around, it is absolutely imperative that we do things differently. The Federal Reserve is the primary reason why our economy is on an endless roller coaster ride. We have had 18 distinct recessions or depressions since 1913, and now another one is about to begin. By endlessly manipulating the system, they have caused these cycles of booms and busts, and it is time to get off of this roller coaster once and for all.

Like Ron Paul, I believe that we need to shut down the Federal Reserve and get our banks under control. I also believe that we should abolish the federal income tax and go to a much fairer system. From 1872 to 1913, there was no central bank and no federal income tax, and it was the greatest period of economic growth in U.S. history. If we rebuild our financial system on sound principles, we could actually have a shot at a prosperous future. If not, the long-term future for our economy looks exceedingly bleak.

If you believe in what I am trying to do, I would like to ask for your help. I am running for Congress in Idaho’s First Congressional District, and since there is no incumbent running for this seat the race is completely wide open. Every time I share my message, more voters are coming over to my side, and if I am able to get my message out to every voter in this district I will win.

And I would like to encourage like-minded people to run for positions all over the country on the federal, state and local levels. Individually, there is a limit to what we can do, but if we work together we can build a movement which could turn this nation completely upside down.

Michael Snyder is a Republican candidate for Congress in Idaho’s First Congressional District, and you can learn how you can get involved in the campaign on his official website. His new book entitled “Living A Life That Really Matters” is available in paperback and for the Kindle on Amazon.com.