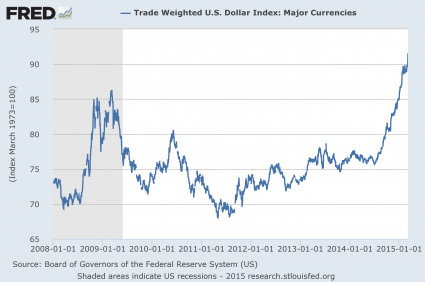

Are we on the verge of an unprecedented global currency crisis? On Tuesday, the euro briefly fell below $1.07 for the first time in almost a dozen years. And the U.S. dollar continues to surge against almost every other major global currency. The U.S. dollar index has now risen an astounding 23 percent in just the last eight months. That is the fastest pace that the U.S. dollar has risen since 1981. You might be tempted to think that a stronger U.S. dollar is good news, but it isn’t. A strong U.S. dollar hurts U.S. exports, thus harming our economy. In addition, a weak U.S. dollar has fueled tremendous expansion in emerging markets around the planet over the past decade or so. When the dollar becomes a lot stronger, it becomes much more difficult for those countries to borrow more money and repay old debts. In other words, the emerging market “boom” is about to become a bust. Not only that, it is important to keep in mind that global financial institutions bet a tremendous amount of money on currency movements. According to the Bank for International Settlements, 74 trillion dollars in derivatives are tied to the value of the U.S. dollar, the value of the euro and the value of other global currencies. When currency rates start flying around all over the place, you can rest assured that someone out there is losing an enormous amount of money. If this derivatives bubble ends up imploding, there won’t be enough money in the entire world to bail everyone out.

Are we on the verge of an unprecedented global currency crisis? On Tuesday, the euro briefly fell below $1.07 for the first time in almost a dozen years. And the U.S. dollar continues to surge against almost every other major global currency. The U.S. dollar index has now risen an astounding 23 percent in just the last eight months. That is the fastest pace that the U.S. dollar has risen since 1981. You might be tempted to think that a stronger U.S. dollar is good news, but it isn’t. A strong U.S. dollar hurts U.S. exports, thus harming our economy. In addition, a weak U.S. dollar has fueled tremendous expansion in emerging markets around the planet over the past decade or so. When the dollar becomes a lot stronger, it becomes much more difficult for those countries to borrow more money and repay old debts. In other words, the emerging market “boom” is about to become a bust. Not only that, it is important to keep in mind that global financial institutions bet a tremendous amount of money on currency movements. According to the Bank for International Settlements, 74 trillion dollars in derivatives are tied to the value of the U.S. dollar, the value of the euro and the value of other global currencies. When currency rates start flying around all over the place, you can rest assured that someone out there is losing an enormous amount of money. If this derivatives bubble ends up imploding, there won’t be enough money in the entire world to bail everyone out.

Do you remember what happened the last time the U.S. dollar went on a great run like this?

As you can see from the chart below, it was in mid-2008, and what followed was the worst financial crisis since the Great Depression…

A rapidly rising U.S. dollar is extremely deflationary for the overall global economy.

This is a huge red flag, and yet hardly anyone is talking about it.

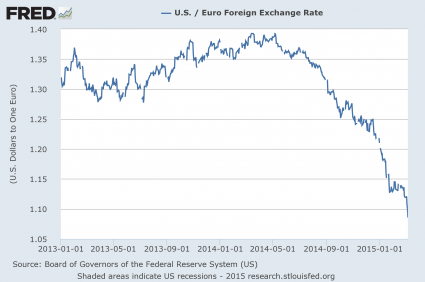

Meanwhile, the euro continues to spiral into oblivion…

How many times have I said it? The euro is heading to all-time lows. It is going to go to parity with the U.S. dollar, and then it is eventually going to go below parity.

This is going to cause massive headaches in the financial world.

The Europeans are attempting to cure their economic problems by creating tremendous amounts of new money. It is the European version of quantitative easing, but it is having some very nasty side effects.

The markets are starting to realize that if the value of the U.S. dollar continues to surge, it is ultimately going to be very bad for stocks. In fact, the strength of the U.S. dollar is being cited as the primary reason for the Dow’s 332 point decline on Tuesday…

The Dow Jones industrial average fell more than 300 points to below the index’s 50-day moving average, wiping out gains for the year. The S&P 500 also closed in the red for the year and breached its 50-day moving average, which is an indicator of the market trend. Only the Nasdaq held onto gains of 2.61 percent for the year.

There’s “concern that energy and the strength in the dollar will somehow be negative for the equities,” said Art Hogan, chief market strategist at Wunderlich Securities. He noted that the speed of the dollar’s surge was the greatest market driver, amid mixed economic data and concerns about the Federal Reserve raising interest rates.

And as I noted above, when the U.S. dollar rises the things that we export to other nations become more expensive and that hurts our businesses.

This is so basic that even the White House understands it…

Despite reassurance from The Fed that a strengthening dollar is positive for US jobs, The White House has now issued a statement that a “strengthening USD is a headwind for US growth.”

But even more important, a surging U.S. dollar makes it more difficult for emerging markets all over the world to borrow new money and to repay old debts. This is especially true for nations that heavily rely on exporting commodities…

It becomes especially ugly for emerging market economies that produce commodities. Many emerging market countries rely on their natural resources for growth and haven’t yet developed more advanced industries. As the products of their principal industries decline in value, foreign investors remove available credit while their currency is declining against the U.S. dollar. They don’t just find it difficult to pay their debt – it is impossible.

It has been estimated that emerging markets have borrowed more than 3 trillion dollars since the last financial crisis.

But now the process that created the emerging markets “boom” is starting to go into reverse.

The global economy is fueled by cheap dollars. So if the U.S. dollar continues to rise, that is not going to be good news for anyone.

And of course the biggest potential threat of all is the 74 trillion dollar currency derivatives bubble which could end up bursting at any time.

The sophisticated computer algorithms that financial institutions use to trade currency derivatives are ultimately based on human assumptions. When currencies move very little and the waters are calm in global financial markets, those algorithms tend to work really, really well.

But when the unexpected happens, some of the largest financial firms in the world can implode seemingly overnight.

Just remember what happened to Lehman Brothers back in 2008. Unexpected events can cripple financial giants in just a matter of hours.

Today, there are five U.S. banks that each have more than 40 trillion dollars of total exposure to derivatives of all types. Those five banks are JPMorgan Chase, Bank of America, Goldman Sachs, Citibank and Morgan Stanley.

By transforming Wall Street into a gigantic casino, those banks have been able to make enormous amounts of money.

But they are constantly performing a high wire act. One of these days, their reckless gambling is going to come back to haunt them, and the entire global financial system is going to be severely harmed as a result.

As I have said so many times before, derivatives are going to be at the heart of the next great global financial crisis.

And thanks to the wild movement of global currencies in recent months, there are now more than 74 trillion dollars in currency derivatives at risk.

Anyone that cannot see trouble on the horizon at this point is being willingly blind.