The next great economic crisis is rapidly approaching, and most people are going to be totally blindsided by it. Even though the warning signs are glaringly obvious, most Americans continue to believe that our “leaders” know what they are doing and that everything will be just fine. But what will happen when the next great financial crash happens and trillions of dollars of “paper wealth” disappear into thin air? What will happen when the coming credit crunch causes economic activity to dramatically slow down and millions upon millions of people lose their jobs? This shouldn’t sound far-fetched to you. Remember, this is exactly the kind of thing that we saw back in 2008, and the next great financial crisis is likely going to be significantly worse. Our economy is in far worse shape than it was back in 2008, and government dependence is now at an all-time high even though most Americans are still enjoying debt-fueled false prosperity. We are living in the largest debt bubble in the history of the planet, and when it bursts we are going to experience a crippling “adjustment” to our standard of loving. Some people understand this and are busy preparing for what is ahead. It has been estimated that there are approximately 3 million “preppers” in the United States, and that number is growing all the time. Unfortunately, most Americans are not preparing for the coming economic depression and they are going to bitterly regret it.

The next great economic crisis is rapidly approaching, and most people are going to be totally blindsided by it. Even though the warning signs are glaringly obvious, most Americans continue to believe that our “leaders” know what they are doing and that everything will be just fine. But what will happen when the next great financial crash happens and trillions of dollars of “paper wealth” disappear into thin air? What will happen when the coming credit crunch causes economic activity to dramatically slow down and millions upon millions of people lose their jobs? This shouldn’t sound far-fetched to you. Remember, this is exactly the kind of thing that we saw back in 2008, and the next great financial crisis is likely going to be significantly worse. Our economy is in far worse shape than it was back in 2008, and government dependence is now at an all-time high even though most Americans are still enjoying debt-fueled false prosperity. We are living in the largest debt bubble in the history of the planet, and when it bursts we are going to experience a crippling “adjustment” to our standard of loving. Some people understand this and are busy preparing for what is ahead. It has been estimated that there are approximately 3 million “preppers” in the United States, and that number is growing all the time. Unfortunately, most Americans are not preparing for the coming economic depression and they are going to bitterly regret it.

So what does preparing for the coming economic depression look like?

Well, it doesn’t have to be complicated. Most of the things that you should do are just common sense.

But there are some people that take things to extremes. For example, a new National Geographic series is featuring a family that is actually constructing a “Doomsday Castle“. The former U.S. Army officer that is building this unusual home is trying to prepare for virtually every type of disaster that he can imagine…

Meet Brent Sr., the leader of the six-person family. Brent is a former Army Infantry Training Officer who is heading up the project to build an “EMP (electromagnetic pulse)-proof medieval castle in the woods of the Carolinas.”

According to National Geographic, Brent is teaching five of his 10 children survival skills.

The unfinished, fortified castle that Brent Sr. is building — an idea he got during the Y2K prep craze — will be able to sustain an EMP-event that could wipe out a power grid, but will also survive natural disasters like hurricanes.

He even plans to train his family members to use crossbows and a catapult to defend against potential home invaders.

Not many people out there are going to take “prepping” to such extremes.

But even if you don’t plan to build a “Doomsday Castle”, that doesn’t mean that you should be doing nothing.

Sadly, most Americans are quite ill-prepared for a major economic downturn at this point. In fact, most Americans seem to be doing almost nothing to prepare.

Just consider the following statistics. Most of these numbers come from one of my previous articles…

-According to a survey that was recently released, 76 percent of all Americans are living paycheck to paycheck.

–46 percent of all Americans have less than $800 in savings.

–27 percent of all Americans do not have even a single penny saved up.

-Less than one out of every four Americans has enough money stored away to cover six months of expenses.

-Each year, 12 million Americans take out high interest payday loans.

-In 1989, the debt to income ratio of the average American family was about 58 percent. Today it is up to 154 percent.

-It is estimated that less than 10 percent of the U.S. population owns any gold or silver for investment purposes.

–44 percent of all Americans do not have first-aid kits in their homes.

–48 percent of all Americans do not have any emergency supplies stored up.

–53 percent of all Americans do not have a 3 day supply of nonperishable food and water in their homes.

–One survey asked Americans how long they thought they would survive if the electrical grid went down for an extended period of time. Incredibly, 21 percent said that they would survive for less than a week, an additional 28 percent said that they would survive for less than two weeks, and nearly 75 percent said that they would be dead before the two month mark.

Those numbers are absolutely appalling.

When the system fails, most people are going to be completely blindsided by it and millions upon millions of people are going to absolutely freak out.

Don’t let that happen to you.

So what are some basic things that you can do to get prepared for the great economic storm that is coming?

The following are a few of the things that Nicole Foss suggests…

1) Hold no debt (for most people this means renting)

2) Hold cash and cash equivalents (short term treasuries) under your own control

3) Don’t trust the banking system, deposit insurance or no deposit insurance

4) Sell equities, real estate, most bonds, commodities, collectibles (or short if you can afford to gamble)

5) Gain some control over the necessities of your own existence if you can afford it

6) Be prepared to work with others as that will give you far greater scope for resilience and security

7) If you have done all that and still have spare resources, consider precious metals as an insurance policy

8) Be worth more to your employer than he is paying you

9) Look after your health!

I think all of those are great pieces of advice.

In addition, below I have posted some of the things that I personally recommend. The following is an excerpt from one of my previous articles entitled “25 Things That You Should Do To Get Prepared For The Coming Economic Collapse“…

#1 An Emergency Fund

Do you remember what happened when the financial system almost collapsed back in 2008? Millions of Americans suddenly lost their jobs, and because many of them were living paycheck to paycheck, many of them also got behind on their mortgages and lost their homes. You don’t want to lose everything that you have worked for during this next major economic downturn. It is imperative that you have an emergency fund. It should be enough to cover all of your expenses for at least six months, but I would encourage you to have an emergency fund that is even larger than that.

#2 Don’t Put All Of Your Eggs Into One Basket

If the wealth confiscation in Cyprus has taught us anything, it is that we should not put all of our eggs in one basket. If all of your money is in one single bank account, it would be easy to wipe out. But if you have your money scattered around a number of different places it will give you a little bit more security.

#3 Keep Some Cash At Home

This goes along with the previous point. While it is not wise to keep all of your money at home, you do want to keep some cash on hand. If there is an extended bank holiday or if a giant burst from the sun causes the ATM machines to go down, you want to be able to have enough cash to buy the things that your family needs. Just ask the people of Cyprus how crippling a bank holiday can be. One way to keep your cash secure at home is by storing it in a concealed safe.

#4 Get Out Of Debt

A lot of people seem to assume that an economic collapse would wipe out all debts, but that will probably not be the case. In fact, if you are in a tremendous amount of debt you will be very vulnerable if the economy collapses and you are not able to find a job. Just ask the people who were overextended and lost their jobs during the last recession. So please get out of debt. Many debt collectors are becoming increasingly ruthless. In many areas of the country they are now routinely putting debtors into prison. You do not want to be a slave to debt when the next wave of the economic collapse strikes.

#5 Gold And Silver

In the long-term, the U.S. dollar is going to lose a tremendous amount of value and inflation is going to absolutely skyrocket. That is one reason why so many people are investing very heavily in gold, silver and other precious metals. All over the globe, the central banks of the world are recklessly printing money. Everyone knows that this is going to end very badly. In fact, there is already a push in more than a dozen U.S. states to allow gold and silver coins to be used as legal tender. Someday you will be glad that you invested in gold and silver now while their prices were still low.

#6 Reduce Your Expenses

A lot of people claim that they can’t put any money toward prepping, but the truth is that we all have room to reduce our expenses. We all spend money on things that we do not really need. Those that are “lean and mean” will tend to do much better during the times that are coming.

#7 Start A Side Business

If you do not have much money, a great way to increase your income is by starting a side business. And it does not take a lot of money – there are many side businesses that you can start for next to nothing. And starting a side business will allow you to become less dependent on your job. In this economic environment, a job could disappear at literally any time.

#8 Move Away From The Big Cities If Possible

For many people, this is simply not possible. Many Americans are still completely and totally dependent on their jobs. But if you are able, now is a good time to move away from the big cities. When the next major economic downturn strikes, there will be rioting and a dramatic rise in crime in the major cities. If you are able to move to a more rural area you will probably be in much better shape.

#9 Store Food

Global food reserves have reached their lowest level in nearly 40 years. As the economy gets even worse and global weather patterns become even more unstable, the price of food will go much higher and global food supplies will become much tighter. In the long run, you will be glad for the money that you put into long-term food storage now.

#10 Learn To Grow Your Own Food

This is a skill that most Americans possessed in the past, but that most Americans today have forgotten. Growing your own food is a way to become more independent of the system, and it is a way to get prepared for what is ahead.

#11 Nobody Can Survive Without Water

Without water, you would not even make it a few days in an emergency situation. It is imperative that you have a plan to provide clean drinking water for your family when disaster strikes.

#12 Have A Plan For When The Grid Goes Down

What would you do if the grid went down and you suddenly did not have power for an extended period of time? Anyone that has spent more than a few hours without power knows how frustrating this can be. You need to have a plan for how you are going to provide power to your home that is independent of the power company.

#13 Have Blankets And Warm Clothing On Hand

This is more for emergency situations or for a complete meltdown of society. During any major crisis, blankets and warm clothing are in great demand. They also could potentially make great barter items.

#14 Store Personal Hygiene Supplies

A lot of preppers store up huge amounts of food, but they forget all about personal hygiene supplies. During a long crisis, these are items that you would greatly miss if you do not have them stored up. These types of supplies would also be great for barter.

#15 Store Medicine And Medical Supplies

You will also want to store up medical supplies and any medicine that you may need. In an emergency situation, you definitely would not want to be without bandages and a first-aid kit. Over the course of a long crisis, you do not want to run out of any medicines that are critical for your health.

#16 Stock Up On Vitamins

A lot of preppers do not think about this either, but it is very important. These days, it is becoming increasingly difficult to get adequate nutrition from the foods that we eat. That is why it is very important to have an adequate store of vitamins and other supplements.

#17 Make A List Of Other Supplies That You Will Need

During any crisis, there will be a lot of other things that you will need in addition to food and water. The following are just a few basic things that it would be wise to have on hand…

– an axe

– a can opener

– flashlights

– battery-powered radio

– extra batteries

– lighters or matches

– fire extinguisher

– sewing kit

– tools

This list could be much, much longer, but hopefully this will get you started.

#18 Don’t Forget The Special Needs Of Your Babies And Your Pets

Young children and pets have special needs. As you store supplies, don’t forget about the things that they will need as well.

#19 Entertainment

This may sound trivial, but the truth is that our entertainment-addicted society would become very bored and very frustrated if the grid suddenly went down for an extended period of time. Card games and other basic forms of entertainment can make enduring a crisis much easier.

#20 Self-Defense

In the years ahead, being able to defend your home and your family is going to become increasingly important. When the economy crashes, people are going to start to become very desperate. And desperate people do desperate things.

#21 Get Your Ammunition While You Still Can

Your firearms will not do you much good if you do not have ammunition for them. Already there are widespread reports of huge ammunition shortages. The following is from a recent CNS News article…

“The run on ammunition has manufacturers scrambling to accommodate demand and reassure customers, as many new and seasoned gun owners stock up over fears of new firearms regulations at both the state and federal levels.”

Don’t just assume that you will always be able to purchase large amounts of ammunition whenever you want. Get it now while you still can.

#22 If You Have To Go…

Have a plan for what you and your family will do if you are forced to leave your home. If you do have to go, the following are some items that you will want to have on hand…

– a map of the area

– a compass

– backpacks for every member of the family

– sleeping bags

– warm clothing

– comfortable shoes or hiking boots

#23 Community

One of the most important assets in any crisis situation is community. If you have friends or neighbors that you can depend upon, that is invaluable. The time spent building those bonds now will pay off greatly during a major crisis.

#24 Have A Back-Up Plan And Be Flexible

Mike Tyson once said the following…

“Everyone has a plan until they get punched in the mouth.”

No plan ever unfolds perfectly. When your plan is disrupted, what will you do?

It will be imperative for all of us to have a back-up plan and to be flexible during the years ahead.

#25 Keep Your Prepping To Yourself

Do not go around and tell everyone in the area where you live about your prepping. If you do, then you may find yourself overwhelmed with “visitors” when everything falls apart.

And please do not go on television and brag about your prepping to a national audience.

Prepping is something that you want to keep to yourself, unless you want hordes of desperate people banging on your door in the future.

*****

For much more on prepping, I would encourage you to check out the dozens of excellent websites out there that teach people advanced prepping techniques for free.

So what do you think about all of this?

Are you getting prepared for the coming economic depression?

Please feel free to share your perspective on prepping by posting a comment below…

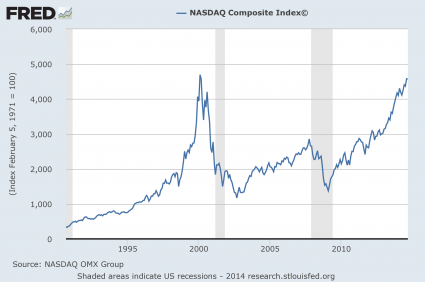

People have such short memories. Even though we are repeating so many of the same patterns that we witnessed in 2000-2001 and 2007-2008, most people do not think that another financial crash is coming. In fact, with the stock market setting record high after record high lately, I have been taking quite a bit of criticism for my relentless warnings about the coming financial storm. Many of the comments go something like this: “Snyder you are a moron! Nothing you say ever comes true. The stock market is going to keep on rocking and Obama is going to lead this country back to greatness. I hope that you choke on all of your doom and gloom.” Of course these critics never offer any hard evidence that I have been wrong about anything. They just assume that since the stock market has soared to unprecedented heights that all of us “bears” must have been wrong.

People have such short memories. Even though we are repeating so many of the same patterns that we witnessed in 2000-2001 and 2007-2008, most people do not think that another financial crash is coming. In fact, with the stock market setting record high after record high lately, I have been taking quite a bit of criticism for my relentless warnings about the coming financial storm. Many of the comments go something like this: “Snyder you are a moron! Nothing you say ever comes true. The stock market is going to keep on rocking and Obama is going to lead this country back to greatness. I hope that you choke on all of your doom and gloom.” Of course these critics never offer any hard evidence that I have been wrong about anything. They just assume that since the stock market has soared to unprecedented heights that all of us “bears” must have been wrong.

{kind=link}

{kind=link}