If the American people truly understood how the Federal Reserve system works and what it has done to us, they would be screaming for it to be abolished immediately. It is a system that was designed by international bankers for the benefit of international bankers, and it is systematically impoverishing the American people. The Federal Reserve system is the primary reason why our currency has declined in value by well over 95 percent and our national debt has gotten more than 5000 times larger over the past 100 years. The Fed creates our “booms” and our “busts”, and they have done an absolutely miserable job of managing our economy. But why do we need a bunch of unelected private bankers to manage our economy and print our money for us in the first place? Wouldn’t our economy function much more efficiently if we allowed the free market to set interest rates? And according to Article I, Section 8 of the U.S. Constitution, the U.S. Congress is the one that is supposed to have the authority to “coin Money, regulate the Value thereof, and of foreign Coin, and fix the Standard of Weights and Measures”. So why is the Federal Reserve doing it? Sadly, this is the way it works all over the globe today. In fact, all 187 nations that belong to the IMF have a central bank. But the truth is that there are much better alternatives. We just need to get people educated.

If the American people truly understood how the Federal Reserve system works and what it has done to us, they would be screaming for it to be abolished immediately. It is a system that was designed by international bankers for the benefit of international bankers, and it is systematically impoverishing the American people. The Federal Reserve system is the primary reason why our currency has declined in value by well over 95 percent and our national debt has gotten more than 5000 times larger over the past 100 years. The Fed creates our “booms” and our “busts”, and they have done an absolutely miserable job of managing our economy. But why do we need a bunch of unelected private bankers to manage our economy and print our money for us in the first place? Wouldn’t our economy function much more efficiently if we allowed the free market to set interest rates? And according to Article I, Section 8 of the U.S. Constitution, the U.S. Congress is the one that is supposed to have the authority to “coin Money, regulate the Value thereof, and of foreign Coin, and fix the Standard of Weights and Measures”. So why is the Federal Reserve doing it? Sadly, this is the way it works all over the globe today. In fact, all 187 nations that belong to the IMF have a central bank. But the truth is that there are much better alternatives. We just need to get people educated.

The following are 11 reasons why the Federal Reserve should be abolished…

#1 The Greatest Period Of Economic Growth In The History Of The United States Happened When There Was No Central Bank

Did you know that the greatest period of economic growth in U.S. history was between the Civil War and 1913? And guess what? That was a period when there was no central bank in the United States at all. The following is from Wikipedia…

The Gilded Age saw the greatest period of economic growth in American history. After the short-lived panic of 1873, the economy recovered with the advent of hard money policies and industrialization. From 1869 to 1879, the US economy grew at a rate of 6.8% for real GDP and 4.5% for real GDP per capita, despite the panic of 1873. The economy repeated this period of growth in the 1880s, in which the wealth of the nation grew at an annual rate of 3.8%, while the GDP was also doubled.

So if our greatest period of economic prosperity was during a time when there was no Federal Reserve, then why shouldn’t we try such a system again?

#2 The Federal Reserve Is Systematically Destroying The Value Of The U.S. Dollar

The United States never had a persistent, ongoing problem with inflation until the Federal Reserve was created in 1913.

If you do not believe this, just check out the inflation chart in this article.

The Federal Reserve systematically penalizes those that try to save their money. Inflation is a tax, and the value of each one of our dollars goes down a little bit more every single day.

But over time, it really adds up. In fact, the value of the U.S. dollar has fallen by 83 percent since 1970.

Anyone that goes to the grocery store on a regular basis knows how painful inflation can be. The following is a list that shows how prices for many of the things that we buy on a regular basis absolutely skyrocketed between 2002 and 2012…

Eggs: 73%

Coffee: 90%

Peanut Butter: 40%

Milk: 26%

A Loaf Of White Bread: 39%

Spaghetti And Macaroni: 44%

Orange Juice: 46%

Red Delicious Apples: 43%

Beer: 25%

Wine: 60%

Electricity: 42%

Margarine: 143%

Tomatoes: 22%

Turkey: 56%

Ground Beef: 61%

Chocolate Chip Cookies: 39%

Gasoline: 158%

Even the price of water has absolutely soared in recent years. According to USA Today, water bills have actually tripled over the past 12 years in some areas of the country.

So how can the Federal Reserve get away with claiming that we are in a “low inflation” environment?

Well, what Ben Bernanke never tells you is that the way that the government calculates inflation has changed more than 20 times since 1978.

The truth is that the real rate of inflation is somewhere between five and ten percent right now, but you will never hear about this on the mainstream news.

#3 The Federal Reserve Is A Perpetual Debt Machine

The Federal Reserve system was designed to be a trap. The intent of the bankers was to trap the U.S. government in an endless debt spiral from which it could never possibly escape.

But most Americans don’t understand this. In fact, most Americans don’t even understand where money comes from.

If you don’t believe this, just go out on the street and ask regular people where money comes from. The responses will be something like this…

“Duh – I don’t know. I’ve got to get home to watch American Idol.”

This is why it is so important to get people educated. I think that most Americans would be horrified to learn that the creation of more money in our system also involves the creation of more debt.

The following is a summary of money creation that comes from one of my previous articles…

When the U.S. government decides that it wants to spend another billion dollars that it does not have, it does not print up a billion dollars.

Rather, the U.S. government creates a bunch of U.S. Treasury bonds (debt) and takes them over to the Federal Reserve.

The Federal Reserve creates a billion dollars out of thin air and exchanges them for the U.S. Treasury bonds.

So what does the Federal Reserve do with those Treasury bonds? I went on to explain what happens…

The U.S. Treasury bonds that the Federal Reserve receives in exchange for the money it has created out of nothing are auctioned off through the Federal Reserve system.

But wait.

There is a problem.

Because the U.S. government must pay interest on the Treasury bonds, the amount of debt that has been created by this transaction is greater than the amount of money that has been created.

So where will the U.S. government get the money to pay that debt?

Well, the theory is that we can get money to circulate through the economy really, really fast and tax it at a high enough rate that the government will be able to collect enough taxes to pay the debt.

But that never actually happens, does it?

And the creators of the Federal Reserve understood this as well. They understood that the U.S. government would not have enough money to both run the government and service the national debt. They knew that the U.S. government would have to keep borrowing even more money in an attempt to keep up with the game.

Men like Thomas Edison and Henry Ford could not understand why we would adopt such a foolish system. For example, Thomas Edison was once quoted in the New York Times as saying the following…

That is to say, under the old way any time we wish to add to the national wealth we are compelled to add to the national debt.

Now, that is what Henry Ford wants to prevent. He thinks it is stupid, and so do I, that for the loan of $30,000,000 of their own money the people of the United States should be compelled to pay $66,000,000 — that is what it amounts to, with interest. People who will not turn a shovelful of dirt nor contribute a pound of material will collect more money from the United States than will the people who supply the material and do the work. That is the terrible thing about interest. In all our great bond issues the interest is always greater than the principal. All of the great public works cost more than twice the actual cost, on that account. Under the present system of doing business we simply add 120 to 150 per cent, to the stated cost.

But here is the point: If our nation can issue a dollar bond, it can issue a dollar bill. The element that makes the bond good makes the bill good.

Unfortunately, today most Americans don’t even understand how the system works. They just assume that we have the best system in the entire world.

Sadly, the reality is that the system is working just as the international bankers that designed it had hoped. The United States has the largest national debt in the history of the world, and we are stealing more than 100 million dollars from our children and our grandchildren every single hour of every single day in a desperate attempt to keep the debt spiral going.

#4 The Federal Reserve Is A Centrally-Planned Financial System That Is The Antithesis Of What A Free Market System Should Be

Why do we need someone to centrally-plan our financial system?

Isn’t that the kind of thing they do in communist China?

Why do we need someone to tell us what interest rates are going to be?

Why do we need someone to determine what “the target rate of inflation” should be?

If we actually had a free market system, the free market would be the one “managing” our economy.

But instead, we have become so accustomed to central planning that any alternatives seem to be absolutely unthinkable.

For example, CNBC cannot possibly imagine a world where the Fed (or some similar institution) was not running things…

But suppose the law were taken off the books? The Fed’s job—in simple terms—is to manage the nation’s money supply and achieve the sometimes-conflicting tasks of full employment, stable prices while fighting inflation or deflation.

How would the U.S. economy then function? Something has to take its place, right?

Global markets would also need some sort of economic direction from the U.S. The Fed manages the dollar — and as the world’s leading currency, a void left by a Fed-less America could throw those markets into chaos with uncertainty about who’s managing U.S. interest rates and the American economy.

I’ve got an idea – let’s let the free market “manage” U.S. interest rates and the American economy.

I know, it’s a crazy idea, but I have a sneaking suspicion that it just might work beautifully.

#5 The Federal Reserve Creates Bubbles And Busts

Do you remember the Dotcom bubble?

Or what about the housing bubble?

By dramatically distorting interest rates and financial behavior, the Federal Reserve creates economic bubbles and the corresponding economic busts.

And guess what?

Now it is happening again.

When will the American people decide that they have had enough?

If you can believe it, there have been 10 different economic recessions since 1950. And of course the Federal Reserve even admits that it helped create the Great Depression of the 1930s.

Perhaps it is time to try something different.

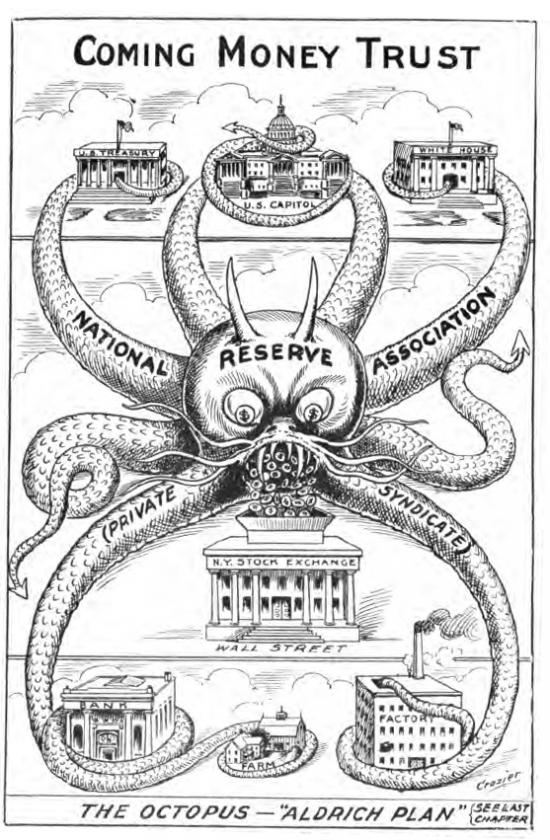

#6 The Federal Reserve Is Privately Owned

It has been said that the Federal Reserve is about as “federal” as Federal Express is.

Most Americans still believe that the Federal Reserve is a “federal agency”, but that is simply not true. The following comes from factcheck.org…

The stockholders in the 12 regional Federal Reserve Banks are the privately owned banks that fall under the Federal Reserve System. These include all national banks (chartered by the federal government) and those state-chartered banks that wish to join and meet certain requirements. About 38 percent of the nation’s more than 8,000 banks are members of the system, and thus own the Fed banks.

And even the Federal Reserve itself has argued that it is “not an agency” of the federal government in court.

So why is there still so much confusion about this?

We should not be allowing a private entity that is owned and dominated by the banks to make decisions that dramatically affect the daily lives of all the rest of us.

#7 The Federal Reserve Greatly Favors The “Too Big To Fail” Banks

Since the Federal Reserve is owned by the banks, should we be surprised that it serves the interests of the banks?

In particular, the Fed has been extremely good to the “too big to fail” banks.

Over the past several decades, those banks have grown tremendously in both size and power.

Back in 1970, the five largest U.S. banks held 17 percent of all U.S. banking industry assets.

Today, the five largest U.S. banks hold 52 percent of all U.S. banking industry assets.

#8 The Federal Reserve Gives Secret Bailouts To Their Friends

The Federal Reserve is the only institution in America that can print money out of thin air and loan it to their friends any time they want to.

For example, did you know that the Federal Reserve made 16 trillion dollars in secret loans to their friends during the last financial crisis?

The following list is taken directly from page 131 of a GAO audit report, and it shows which banks received secret loans from the Fed…

Citigroup – $2.513 trillion

Morgan Stanley – $2.041 trillion

Merrill Lynch – $1.949 trillion

Bank of America – $1.344 trillion

Barclays PLC – $868 billion

Bear Sterns – $853 billion

Goldman Sachs – $814 billion

Royal Bank of Scotland – $541 billion

JP Morgan Chase – $391 billion

Deutsche Bank – $354 billion

UBS – $287 billion

Credit Suisse – $262 billion

Lehman Brothers – $183 billion

Bank of Scotland – $181 billion

BNP Paribas – $175 billion

Wells Fargo – $159 billion

Dexia – $159 billion

Wachovia – $142 billion

Dresdner Bank – $135 billion

Societe Generale – $124 billion

“All Other Borrowers” – $2.639 trillion

If you will notice, a number of the banks listed above are foreign banks.

Why is the Fed allowed to print money out of thin air and lend it to foreign banks?

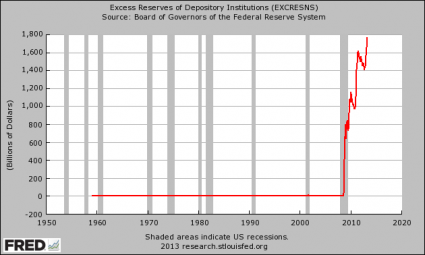

#9 The Federal Reserve Is Paying Banks Not To Lend Money

Did you know that the Federal Reserve is actually paying U.S. banks not to lend money?

That doesn’t make sense. Our economy is based on credit, and small businesses desperately need loans in order to operate.

But the Fed has decided to pay banks not to risk their money. Section 128 of the Emergency Economic Stabilization Act of 2008 allows the Federal Reserve to pay interest on “excess reserves” that U.S. banks park at the Fed.

So the big banks can just send their cash to the Fed and watch the money come rolling in risk-free.

As the chart below demonstrates, the banks have taken great advantage of this tremendous deal…

#10 The Federal Reserve Has An Astounding Track Record Of Failure

Over the past ten years, the Federal Reserve has been an abysmal failure when it comes to running the economy.

But despite a track record of failure that would make the Chicago Cubs look like a roaring success, Barack Obama actually decided to nominate Ben Bernanke for a second term as the Chairman of the Federal Reserve.

What a mistake.

Just check out some of the things that Bernanke said prior to the last financial crisis. The following is an extended excerpt from an article that I published previously…

*****

In 2005, Bernanke said that we shouldn’t worry because housing prices had never declined on a nationwide basis before and he said that he believed that the U.S. would continue to experience close to “full employment”….

“We’ve never had a decline in house prices on a nationwide basis. So, what I think what is more likely is that house prices will slow, maybe stabilize, might slow consumption spending a bit. I don’t think it’s gonna drive the economy too far from its full employment path, though.”

In 2005, Bernanke also said that he believed that derivatives were perfectly safe and posed no danger to financial markets….

“With respect to their safety, derivatives, for the most part, are traded among very sophisticated financial institutions and individuals who have considerable incentive to understand them and to use them properly.”

In 2006, Bernanke said that housing prices would probably keep rising….

“Housing markets are cooling a bit. Our expectation is that the decline in activity or the slowing in activity will be moderate, that house prices will probably continue to rise.”

In 2007, Bernanke insisted that there was not a problem with subprime mortgages….

“At this juncture, however, the impact on the broader economy and financial markets of the problems in the subprime market seems likely to be contained. In particular, mortgages to prime borrowers and fixed-rate mortgages to all classes of borrowers continue to perform well, with low rates of delinquency.”

In 2008, Bernanke said that a recession was not coming….

“The Federal Reserve is not currently forecasting a recession.”

A few months before Fannie Mae and Freddie Mac collapsed, Bernanke insisted that they were totally secure….

“The GSEs are adequately capitalized. They are in no danger of failing.”

*****

There are many, many more examples that could be listed, but hopefully you get the point.

And now it is happening again. Bernanke is telling the American people that everything is going to be just fine and that no major problems are ahead.

Do you believe him this time?

#11 The Federal Reserve Is Unaccountable To The American People

What is the most important political issue to most Americans?

Survey after survey has shown that the American people care about the economy more than anything else.

So why do we allow an unelected, unaccountable entity that is privately-owned to make our economic decisions for us?

The Federal Reserve has become so powerful that it has been called “the fourth branch of government”. Every four years, presidential candidates argue about who will be best at managing the economy, but the truth is that it is the Fed that manages our economy.

We are told that the “independence” of the Federal Reserve is absolutely critical, but don’t the American people deserve to have a say in the running of the economy?

Our system is broken. It is a system that will continue to create more bubbles and more debt until the entire thing finally collapses for good.

Thomas Jefferson once stated that if he could add just one more amendment to the U.S. Constitution it would be a ban on all government borrowing….

I wish it were possible to obtain a single amendment to our Constitution. I would be willing to depend on that alone for the reduction of the administration of our government to the genuine principles of its Constitution; I mean an additional article, taking from the federal government the power of borrowing.

But instead of banning government borrowing, we have allowed ourselves to become enslaved to a system where government borrowing actually creates our money.

We do not need to have a central bank. There are much better alternatives. We just need to get people educated.

Please share this article with as many people as you possibly can. These are things that every American should know about the Fed, and we need to educate the American people about the Federal Reserve while there is still time.

Did you know that there are 5 “too big to fail” banks in the United States that each have exposure to derivatives contracts that is in excess of 30 trillion dollars? Overall, the biggest U.S. banks collectively have more than 247 trillion dollars of exposure to derivatives contracts. That is an amount of money that is more than 13 times the size of the U.S. national debt, and it is a ticking time bomb that could set off financial Armageddon at any moment. Globally, the notional value of all outstanding derivatives contracts is a staggering 552.9 trillion dollars according to the Bank for International Settlements. The bankers assure us that these financial instruments are far less risky than they sound, and that they have spread the risk around enough so that there is no way they could bring the entire system down. But that is the thing about risk – you can try to spread it around as many ways as you can, but you can never eliminate it. And when this derivatives bubble finally implodes, there won’t be enough money on the entire planet to fix it.

Did you know that there are 5 “too big to fail” banks in the United States that each have exposure to derivatives contracts that is in excess of 30 trillion dollars? Overall, the biggest U.S. banks collectively have more than 247 trillion dollars of exposure to derivatives contracts. That is an amount of money that is more than 13 times the size of the U.S. national debt, and it is a ticking time bomb that could set off financial Armageddon at any moment. Globally, the notional value of all outstanding derivatives contracts is a staggering 552.9 trillion dollars according to the Bank for International Settlements. The bankers assure us that these financial instruments are far less risky than they sound, and that they have spread the risk around enough so that there is no way they could bring the entire system down. But that is the thing about risk – you can try to spread it around as many ways as you can, but you can never eliminate it. And when this derivatives bubble finally implodes, there won’t be enough money on the entire planet to fix it.

{kind=link}