Barack Obama is warning that if he does not get everything that he wants that he will force the U.S. government into a devastating debt default which will cripple the entire global economy. In essence, Obama has become so power mad that he is actually willing to take the entire planet hostage in order to achieve his goals. A lot of people are blaming the government shutdown on the Republicans, but they have already voted to fund the entire government except for Obamacare. The U.S. Constitution requires that all spending bills originate in the House of Representatives, and the House did their duty by passing a spending bill. If the Senate or the President do not like the bill that the House has passed, then negotiations need to take place. That is how our system works. And the weak-kneed Republicans have already indicated that they are willing to give up virtually all of their prior demands. In fact, if Obama offered all of them 20 dollar gift certificates to Denny’s to end this crisis they would probably jump at that deal. But that is not good enough for Obama. He has made it clear that he will settle for nothing less than the complete and unconditional surrender of the Republican Party.

Barack Obama is warning that if he does not get everything that he wants that he will force the U.S. government into a devastating debt default which will cripple the entire global economy. In essence, Obama has become so power mad that he is actually willing to take the entire planet hostage in order to achieve his goals. A lot of people are blaming the government shutdown on the Republicans, but they have already voted to fund the entire government except for Obamacare. The U.S. Constitution requires that all spending bills originate in the House of Representatives, and the House did their duty by passing a spending bill. If the Senate or the President do not like the bill that the House has passed, then negotiations need to take place. That is how our system works. And the weak-kneed Republicans have already indicated that they are willing to give up virtually all of their prior demands. In fact, if Obama offered all of them 20 dollar gift certificates to Denny’s to end this crisis they would probably jump at that deal. But that is not good enough for Obama. He has made it clear that he will settle for nothing less than the complete and unconditional surrender of the Republican Party.

Why is Obama doing this? Why is Obama willing to bring the country to the brink of financial disaster?

It isn’t hard to figure out. Just check out what one senior Obama administration official said last week…

“We are winning…. It doesn’t really matter to us” how long the shutdown lasts “because what matters is the end result,” a senior Obama Administration official told the Wall Street Journal last week.

This is all about a political victory and crushing the Republicans. Obama doesn’t really care how long this crisis lasts because he believes that he is getting the end result that he wants.

According to Obama, the Republican Party is just supposed to roll over and give him the exact spending bill that he wants and also give him another trillion dollar increase in the debt limit.

If the Republicans do not give him that, he is willing to plunge us into financial oblivion.

The funny thing is that most Americans do not want the debt limit increased. According to one new poll, 58 percent of all Americans do not even want the debt ceiling to be increased by a single penny.

And recent polls show that Americans are against Obamacare by an average margin of about 10 percent.

But the pathetic Republican Party is actually willing to hand Obama a trillion dollar debt ceiling increase and fully fund Obamacare if Obama will at least give them something.

Unfortunately, Obama won’t even give them the time of day.

So don’t blame the Republicans for what is happening. The Republicans have already compromised themselves to the point of utter disgrace. If Obama had been willing to even compromise a couple of inches this entire crisis would already be over.

And nobody should be claiming that the Republicans won’t vote to end this shutdown. They have already voted to end it. The following is from a recent article by Thomas Sowell…

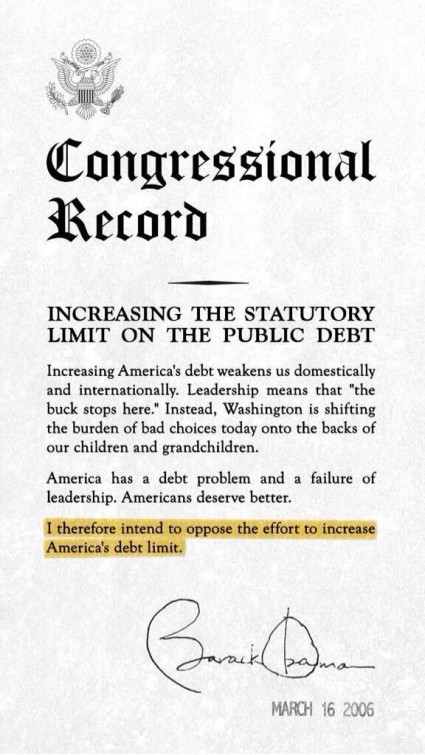

There is really nothing complicated about the facts. The Republican-controlled House of Representatives voted all the money required to keep all government activities going — except for ObamaCare.

This is not a matter of opinion. You can check the Congressional Record.

As for the House of Representatives’ right to grant or withhold money, that is not a matter of opinion either. You can check the Constitution of the United States. All spending bills must originate in the House of Representatives, which means that Congressmen there have a right to decide whether or not they want to spend money on a particular government activity.

Whether ObamaCare is good, bad or indifferent is a matter of opinion. But it is a matter of fact that members of the House of Representatives have a right to make spending decisions based on their opinion.

Once again, the Republicans have already indicated that they are willing to fund Obamacare. They just want Obama to throw them a bone.

And Obama will not do it.

So either the Republicans are going to cave in completely (a very real possibility) or we are going to pass the “debt ceiling deadline”.

What happens then?

Well, we would have more of a “real government shutdown” than the fake shutdown that we are having right now.

Once the federal government cannot borrow any more money, it will only be able to spend what it actually has on hand. That means that a lot more government functions will have to shut down.

Money will still be coming in to the government, but it won’t be enough to fund everything. According to the Wall Street Journal, the federal government will still have enough money to pay interest on the debt, make Social Security payments, make Medicare payments, make Medicaid payments, provide food stamp benefits and pay the military if they cut almost everything else out.

The other day, I suggested that the federal government could potentially start defaulting on interest payments on the debt as early as November. But that would only happen if the federal government manages their money foolishly.

If the federal government managed their money smartly and saved cash for the interest payments as they came due, they would not have to miss any.

But when was the last time the federal government ever did anything “smartly”?

For the sake of argument, however, let’s assume that the federal government can manage money wisely and can save up enough cash ahead of time for large interest payments as they come due.

If that could somehow be managed, then according to Paul Mampilly the government would never need to actually default…

The U.S. Treasury always has money coming into its accounts. So its always got some amount of cash that it can use to pay interest on bonds. That’s especially true right now because the government is partially shutdown and there’s no cash going out from its accounts.

In fact, when you look at it the U.S. Treasury should simply have no trouble making interest payments on bonds that it has issued.

And there’s no restriction on the U.S. Treasury prioritizing interest payments. Why?

The obligation to pay interest is set by the 1917 Second Liberty Bond Act and laws that commanded the Treasury to pay interest on the debt. You can look this up in section 3123 of Title 31 of the U.S. Code and section 4 of the 14th Amendment of the Constitution and in Supreme Court precedent (Perry v. United States). It’s all there in black and white.

So the only possible way the U.S. defaults on its debt is if Barack Obama, President of the United States, instructs his Treasury secretary Jack Lew to default on the debt.

And according to the Washington Post, Moody’s has just issued a memo that also indicates that the federal government should be able to make all interest payments even if the debt limit is not increased…

In a memo being circulated on Capitol Hill Wednesday, Moody’s Investors Service offers “answers to frequently asked questions” about the government shutdown, now in its second week, and the federal debt limit. President Obama has said that, unless Congress acts to raise the $16.7 trillion limit by next Thursday, the nation will be at risk of default.

Not so, Moody’s says in the memo dated Oct. 7.

“We believe the government would continue to pay interest and principal on its debt even in the event that the debt limit is not raised, leaving its creditworthiness intact,” the memo says. “The debt limit restricts government expenditures to the amount of its incoming revenues; it does not prohibit the government from servicing its debt. There is no direct connection between the debt limit (actually the exhaustion of the Treasury’s extraordinary measures to raise funds) and a default.”

Of course the federal government would have to stop throwing money around like a drunk gambler at a casino in Las Vegas in order for this to work.

On the very first day of the government shutdown, the feds gave $445 million to the Corporation for Public Broadcasting. Apparently Elmo is considered to be “essential personnel” by the Obama administration.

And according to CNS News, the U.S. Army has committed more than $47,000 to buy a mechanical bull during this “shutdown”…

The government shutdown may be keeping furloughed federal workers at home, but on Monday the U.S. Army contracted to buy a mechanical bull.

The $47,174 contract was awarded on Oct. 7 to Mechanical Bull Sales Inc. of State College, Penn.

So needless to say, there is some serious doubt about whether the federal government would be able to manage their money effectively in the event that the debt ceiling deadline passes.

And if the U.S. did start defaulting on debt payments, it would be absolutely disastrous for the global economy as I discussed in a previous article…

“A U.S. debt default would cause stocks to crash, would cause bonds to crash, would cause interest rates to soar wildly out of control, would cause a massive credit crunch, and would cause a derivatives panic that would be absolutely unprecedented. And that would just be for starters.”

Other nations that we depend upon to lend us money would stop lending to us and would start dumping U.S. debt instead.

Could you imagine what would happen if China started dumping a large portion of the 1.3 trillion dollars in U.S. debt that they are holding?

It would be a total nightmare. The collapse of Lehman Brothers would pale in comparison.

And already some banks are stuffing their ATM machines with extra cash just in case the general public starts to panic.

But none of this has to happen.

If Obama decides to negotiate with the Republicans, this crisis will likely end very rapidly.

If not, and we pass the “debt ceiling deadline”, the federal government will still have enough money to make interest payments on the debt as long as they manage their money correctly.

Unfortunately, Obama seems far more interested in playing political games than he is in solving our problems.

In fact, Park Service rangers have been ordered to “make life as difficult for people as we can” during this government shutdown. Obama has apparently decided to punish the American people in order to get leverage on the Republicans. Just check out the following example from a new Weekly Standard article…

There’s a cute little historic site just outside of the capital in McLean, Virginia, called the Claude Moore Colonial Farm. They do historical reenactments, and once upon a time the National Park Service helped run the place. But in 1980, the NPS cut the farm out of its budget. A group of private citizens set up an endowment to take care of the farm’s expenses. Ever since, the site has operated independently through a combination of private donations and volunteer workers.

The Park Service told Claude Moore Colonial Farm to shut down.

The farm’s administrators appealed this directive—they explained that the Park Service doesn’t actually do anything for the historic site. The folks at the NPS were unmoved. And so, last week, the National Park Service found the scratch to send officers to the park to forcibly remove both volunteer workers and visitors.

Think about that for a minute. The Park Service, which is supposed to serve the public by administering parks, is now in the business of forcing parks they don’t administer to close. As Homer Simpson famously asked, did we lose a war?

The hypocrisy that Obama has demonstrated during this “government shutdown” has been astounding.

He has barricaded open air war memorials to keep military veterans from visiting them, but he temporarily reopened the National Mall so that a huge pro-immigration rally that would benefit him politically could be held.

He has continued to fund al-Qaeda rebels in Syria that are trying to overthrow the Syrian government, but he has been withholding death benefits from families of fallen U.S. soldiers.

The conduct of the Obama administration during this shutdown has been so egregious that is hard to put into words. Obama has chosen to purposely harm the American people in order to score political points.

But this is how our politicians view us these days. As Monty Pelerin recently explained, most of our politicians have absolutely no problem with exploiting us for their own purposes…

The concept of political service has been replaced by that of masked exploitation. The public is no longer viewed as clients or constituents to be served. Instead they have become political prey. Politicians see the public as a collection of wallets and votes, fair game to be hunted as the means to expand power and wealth. Constituents are now the Soylent Green of the political food chain.

The political class assumes the public exists to serve them, not the other way around. Public participation beyond the lightening of wallets or the provision of votes is unwelcome. It is considered “interference” that must be deterred by the ruling class.

The political class is now a huge, voracious parasite. Like the plant in the Little Shop of Horrors, its needs have grown to the point where it threatens anything productive. Its needs now exceed the willingness for continued sacrifice on the part of the productive. The parasite threatens the very existence of the host.

The political Ponzi scheme of tax, borrow and spend has reached its limit. Either it will die when citizens turn on it or it will kill the productive, ensuring its own destruction.

It perishes in the end. Whether it takes civilization with it is the bigger question.

Is there anyone out there that still does not believe that our system is broken?

Hopefully cooler heads will prevail and power mad Obama will decide to toss the Republicans a few crumbs and this crisis will be resolved.

Because if this crisis is not resolved soon, it could have consequences that are far beyond what any of us could possibly imagine.

As we enter the second half of 2015, financial panic has gripped most of the globe. Stock prices are crashing in China, in Europe and in the United States. Greece is on the verge of a historic default, and now Puerto Rico and Ukraine are both threatening to default on their debts if they do not receive concessions from their creditors. Not since the financial crisis of 2008 has so much financial chaos been unleashed all at once. Could it be possible that the great financial crisis of 2015 has begun? The following are 16 facts about the tremendous financial devastation that is happening all over the world right now…

As we enter the second half of 2015, financial panic has gripped most of the globe. Stock prices are crashing in China, in Europe and in the United States. Greece is on the verge of a historic default, and now Puerto Rico and Ukraine are both threatening to default on their debts if they do not receive concessions from their creditors. Not since the financial crisis of 2008 has so much financial chaos been unleashed all at once. Could it be possible that the great financial crisis of 2015 has begun? The following are 16 facts about the tremendous financial devastation that is happening all over the world right now…