We haven’t seen anything like this since the financial crisis of 2008. Investors are taking money out of global stock funds at a pace that we haven’t seen in 10 years, and many believe that this is a harbinger of tough times ahead. Global stocks lost about 10 trillion dollars in value during the first half of 2018, and an even worse performance during the second half of the year will almost certainly push the global financial system into panic mode. U.S. stocks have been relatively stable, and so most Americans are not too alarmed about what is happening just yet. But if you look back throughout history, emerging market chaos is often an early warning signal that a major global crisis is on the horizon, and that is precisely what is happening right now. Financial markets in emerging markets all over the planet are in the process of melting down, and the losses are becoming quite dramatic.

We haven’t seen anything like this since the financial crisis of 2008. Investors are taking money out of global stock funds at a pace that we haven’t seen in 10 years, and many believe that this is a harbinger of tough times ahead. Global stocks lost about 10 trillion dollars in value during the first half of 2018, and an even worse performance during the second half of the year will almost certainly push the global financial system into panic mode. U.S. stocks have been relatively stable, and so most Americans are not too alarmed about what is happening just yet. But if you look back throughout history, emerging market chaos is often an early warning signal that a major global crisis is on the horizon, and that is precisely what is happening right now. Financial markets in emerging markets all over the planet are in the process of melting down, and the losses are becoming quite dramatic.

As stock prices around the planet start to plummet, investors are pulling money out of global stock funds very, very rapidly. The following comes from CNBC…

Investor money is hemorrhaging out of global stock funds at a pace not seen since just after the financial crisis exploded.

Global equity funds have seen outflows of $12.4 billion in June, a level not seen since October 2008, according to market research firm TrimTabs. Lehman Brothers collapsed in September of that year, triggering the worst economic downturn since the Great Depression and helping fuel a bear market that would see major indexes lose more than 60 percent of their value.

Does this automatically mean that another major financial crisis is on the way in the United States?

No, but it is definitely not a good sign.

As CNBC also noted, investors have been taking tremendous amounts of money out of one emerging market ETF in particular…

The iShares emerging market ETF has seen $5.4 billion in outflows in June, the most of any fund, according to ETF.com.

“U.S. dollar strength and persistent underperformance seem to be driving fund investors away from non-U.S. equities,” TrimTabs said in a note.

The list of emerging market economies that are in crisis mode is beginning to get really long. Argentina, Venezuela, Turkey, Brazil and South Africa are some of the more prominent examples.

If the chaos in emerging markets continues to intensify, the rush for the exits is going to become a stampede. Not too long ago, I discussed the fact that the “smart money” was getting out of stocks at a pace that we haven’t seen since just before the last financial crisis, and it isn’t going to take too much to set off a full-blown financial avalanche.

In the general population, most people still seem to think that the financial system is in good shape. But in many ways, the first half of 2018 was the worst half of a year for the global financial system since the financial crisis of 2008. The following summary of the carnage that we have witnessed over the last 6 months comes from Zero Hedge…

- Bitcoin Worst Start To A Year Ever

- German Banks At Lowest Since 1988

- Onshore Yuan Worst Quarter Since 1994

- Argentine Peso Worst Start To A Year Since 2002

- US Financial Conditions Tightened The Most To Start A Year Since 2002

- Global Systemically Important Banks Worst Start To A Year Since 2008

- Global Stocks Worst Start To A Year Since 2010

- China Stocks Worst Start To A Year Since 2010

- German Stocks Worst Start (In USD Terms) Since 2010

- Global Economic Data Disappointments Worst Since 2012

- Emerging Markets, Gold, Silver Worst Start To A Year Since 2013

- High Yield Bonds Worst Start To A Year Since 2013

- Offshore Yuan Worst Month Since Aug 2015

- Global Bonds Worst Start To A Year Since 2015

- Treasury Yield Curve Down Record 16 Of Last 18 Quarters

And as I mentioned above, global stocks lost about 10 trillion dollars in value over the last 6 months.

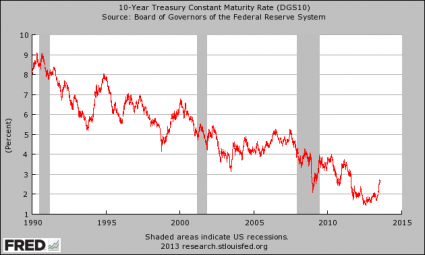

When the Federal Reserve hikes interest rates, it puts a lot of financial stress on emerging markets. It becomes much more expensive to take out dollar-denominated loans, and it also becomes much more expensive to pay back existing dollar-denominated debts.

But the Fed has not listened to appeals from the rest of the world, and has decided to accelerate the pace of rate hikes instead.

Meanwhile, the trade wars that the United States has started with other nations continue to escalate. Here are the latest developments…

U.S. farmers and food producers are in the cross-hairs of a global trade conflict that shows no signs of abating anytime soon — and things are about to escalate in a big way on Sunday.

New tariffs will be imposed by Canada on beef, and more retaliation will come this week when China and Mexico take aim at pork. China’s also planning a 25 percent tariff on soybeans on July 6 in addition to hikes on pork duties, and Mexico’s 20 percent levy on “the other white meat” is set to begin July 5.

Meanwhile, the European Union’s initial duties worth $3.2 billion took effect June 22. Most of the duties amount to 25 percent, and include a variety of U.S. products, including motorcycles, boats, whiskey and peanut butter.

If nobody gives in, economic activity will start to slow down substantially. This is what CNN says that we should expect…

Here’s how the dominoes could fall: First, businesses would be hit with higher costs triggered by tariffs. Then, companies won’t be able to figure out how to get the materials they need. Eventually, confidence among executives and households would drop. Businesses would respond by drastically scaling back spending.

A perfect storm is starting to emerge, and investors are getting spooked.

If financial problems continue to get worse in emerging markets, and if the Federal Reserve continues to raise interest rates, and if these trade wars continue to grow, it is only a matter of time before we have a major market catastrophe in the United States.

The storm clouds on the horizon have just kept getting darker and darker, and many analysts all over the nation agree that this is the gloomiest that things have looked since 2008.

Hopefully a way can be found to turn things around, but I wouldn’t count on it…

Michael Snyder is a nationally syndicated writer, media personality and political activist. He is the author of four books including The Beginning Of The End and Living A Life That Really Matters.

{kind=link}