The higher financial markets rise, the harder they fall. By any objective measurement, the stock market is currently well into bubble territory. Anyone should be able to see this – all you have to do is look at the charts. Sadly, most of us never seem to learn from history. Most of us want to believe that somehow “things are different this time”. Well, about the only thing that is different this time is that our economy is in far worse shape than it was just prior to the last major financial crisis. That means that we are more vulnerable and will almost certainly endure even more damage this time around. It would be one thing if stocks were soaring because the U.S. economy as a whole was doing extremely well. But we all know that isn’t true. Instead, what we have been experiencing is clearly artificial market behavior that has nothing to do with economic reality. In other words, we are dealing with an irrational financial bubble, and all irrational financial bubbles eventually burst. And as I wrote about yesterday, the way that stocks have moved so far this year is eerily reminiscent of the way that stocks moved in early 2008. The warning signs are there – if you are willing to look at them.

The higher financial markets rise, the harder they fall. By any objective measurement, the stock market is currently well into bubble territory. Anyone should be able to see this – all you have to do is look at the charts. Sadly, most of us never seem to learn from history. Most of us want to believe that somehow “things are different this time”. Well, about the only thing that is different this time is that our economy is in far worse shape than it was just prior to the last major financial crisis. That means that we are more vulnerable and will almost certainly endure even more damage this time around. It would be one thing if stocks were soaring because the U.S. economy as a whole was doing extremely well. But we all know that isn’t true. Instead, what we have been experiencing is clearly artificial market behavior that has nothing to do with economic reality. In other words, we are dealing with an irrational financial bubble, and all irrational financial bubbles eventually burst. And as I wrote about yesterday, the way that stocks have moved so far this year is eerily reminiscent of the way that stocks moved in early 2008. The warning signs are there – if you are willing to look at them.

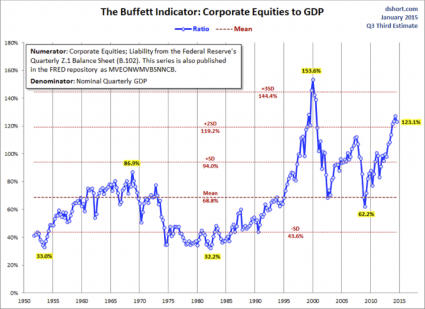

The first chart that I want to share with you today comes from Doug Short. It is a chart that shows that the ratio of corporate equities (stocks) to GDP is the second highest that it has been since 1950. The only other time it has been higher was just before the dotcom bubble burst…

Does that look like a bubble to you?

It sure looks like a bubble to me.

In order for the corporate equities to GDP ratio to get back to the mean (average) level, stock prices would have to fall nearly 50 percent.

If that happens, people will be calling it a crash, but in truth it would just be a return to normalcy.

This next chart comes from Phoenix Capital Research. The CAPE ratio (cyclically adjusted price-to-earnings ratio) is considered to be an extremely accurate measure of the true value of stocks…

As I’ve noted before, the single best predictor of stock market performance is the cyclically adjusted price-to-earnings ratio or CAPE ratio.

Corporate earnings are heavily influenced by the business cycle. Typically the US experiences a boom and bust once every ten years or so. As such, companies will naturally have higher P/E’s at some points and lower P/E’s at other. This is based solely on the business cycle and nothing else.

CAPE adjusts for this by measuring the price of stocks against the average of ten years’ worth of earnings, adjusted for inflation. By doing this, it presents you with a clearer, more objective picture of a company’s ability to produce cash in any economic environment.

Based on a study completed Vanguard, CAPE was the single best metric for measuring future stock returns.

When the CAPE ratio is too high, that means that stocks are overpriced and are not a good value. And right now the CAPE ratio is the 3rd highest that it has been since 1890. That only times it has been higher than this were in 1929 (we all remember what happened then) and just before the dotcom bubble burst…

The funny thing is that stocks have continued to rise even as corporate revenues have begun to fall.

According to Wolf Richter, in the first quarter of 2015 corporate revenues are projected to decline at the fastest pace that we have seen since the depths of the last recession…

Week after week, corporations and analysts have been whittling down their estimates. By now, revenues of the S&P 500 companies are expected to decline 2.8% in Q1 from a year ago – the worst year-over-year decline since Q3 of crisis year 2009.

This next chart I want to share with you shows how the Nasdaq has performed over the past decade. Looking at this chart alone, you would think that the U.S. economy must have been absolutely roaring since the end of the last recession. But what is really going on is rampant speculation. Some of the tech companies that make up the Nasdaq are not making any profits at all and yet they are supposedly worth billions of dollars. If you cannot see a bubble in this chart, you need to get your vision checked…

And this kind of irrational euphoria is not just happening in the United States.

For example, Chinese stocks are up nearly 80 percent over the past nine months.

Meanwhile, the overall Chinese economy is growing at the slowest pace that we have seen in about 20 years.

Right now, we are in the calm before the storm. We are right at the door of the next great financial crisis, and most of the people that work in the industry know this.

And once in a while they let the cat out of the bag.

For example, consider what Hans-Jörg Vetter, the CEO of Landesbank Baden-Württemberg in Germany, had to say during one recent press conference…

“Risk is no longer priced in,” he said. And these investors aren’t paid for the risks they’re taking. This applies to all asset classes, he said. The stock and the bond markets, he said, are now both seeing “the mother of all bubbles.”

This can’t go on forever. Or for very long. But he couldn’t see the future either and pin down a date, which is what everyone wants to know so that they can all get out in time. “I cannot tell you when it will rumble,” he said, “but eventually it will rumble again.”

By “again” he meant the sort of thing that had taken the bank down last time, the Financial Crisis. It had been triggered by horrendous risk-taking, where risks hadn’t been priced into all kinds of securities. When those securities – mortgage-backed securities, for example, that were hiding the inherent risks under a triple-A rating – blew up, banks toppled.

What Vetter is telling us is what I have been warning about for a long time.

Another great stock market crash is coming.

It is just a matter of time.