Eventually the money runs out. Much of America was shocked when the city of Detroit defaulted on a $39.7 million debt payment and announced that it was suspending payments on $2.5 billion of unsecured debt, but those who visit my site on a regular basis were probably not too surprised. Anyone with half a brain and a calculator could see this coming from a mile away. But people kept foolishly lending money to the city of Detroit, and now many of them are going to get hit really hard. Detroit Emergency Manager Kevyn Orr has submitted a proposal that would pay unsecured creditors about 10 cents on the dollar. Similar haircuts would be made to underfunded pension and health benefits for retirees. Orr is hoping that the creditors and the unions that he will be negotiating with will accept this package, but he concedes that there is still a “50-50 chance” that the city of Detroit will be forced to formally file for bankruptcy. But what Detroit is facing is not really that unique. In fact, Detroit is a perfect example of what the future of America is going to look like. We live in a nation that is rotting, decaying, drowning in debt and racing toward insolvency. Already there are dozens of other cities across the nation that are poverty-ridden, crime-infested hellholes just like Detroit is, and hundreds of other communities are rapidly heading in that direction. So don’t look down on Detroit. They just got there before the rest of us.

Eventually the money runs out. Much of America was shocked when the city of Detroit defaulted on a $39.7 million debt payment and announced that it was suspending payments on $2.5 billion of unsecured debt, but those who visit my site on a regular basis were probably not too surprised. Anyone with half a brain and a calculator could see this coming from a mile away. But people kept foolishly lending money to the city of Detroit, and now many of them are going to get hit really hard. Detroit Emergency Manager Kevyn Orr has submitted a proposal that would pay unsecured creditors about 10 cents on the dollar. Similar haircuts would be made to underfunded pension and health benefits for retirees. Orr is hoping that the creditors and the unions that he will be negotiating with will accept this package, but he concedes that there is still a “50-50 chance” that the city of Detroit will be forced to formally file for bankruptcy. But what Detroit is facing is not really that unique. In fact, Detroit is a perfect example of what the future of America is going to look like. We live in a nation that is rotting, decaying, drowning in debt and racing toward insolvency. Already there are dozens of other cities across the nation that are poverty-ridden, crime-infested hellholes just like Detroit is, and hundreds of other communities are rapidly heading in that direction. So don’t look down on Detroit. They just got there before the rest of us.

The following are some facts about Detroit that are absolutely mind-blowing…

1 – Detroit was once the fourth-largest city in the United States, and in 1960 Detroit had the highest per-capita income in the entire nation.

2 – Over the past 60 years, the population of Detroit has fallen by 63 percent.

3 – At this point, approximately 40 percent of all the streetlights in the city don’t work.

4 – Some ambulances in the city of Detroit have been used for so long that they have more than 250,000 miles on them.

5 – 210 of the 317 public parks in the city of Detroit have been permanently closed down.

6 – According to the New York Times, there are now approximately 70,000 abandoned buildings in Detroit.

7 – Approximately one-third of Detroit’s 140 square miles is either vacant or derelict.

8 – Less than half of the residents of Detroit over the age of 16 are working at this point.

9 – If you can believe it, 60 percent of all children in the city of Detroit are living in poverty.

10 – According to one very shocking report, 47 percent of the residents of Detroit are functionally illiterate.

11 – Today, police solve less than 10 percent of the crimes that are committed in Detroit.

12 – Ten years ago, there were approximately 5,000 police officers in the city of Detroit. Today, there are only about 2,500 and another 100 are scheduled to be eliminated from the force soon.

13 – Due to budget cutbacks, most police stations in Detroit are now closed to the public for 16 hours a day.

14 – The murder rate in Detroit is 11 times higher than it is in New York City.

15 – Crime has gotten so bad in Detroit that even the police are telling people to “enter Detroit at your own risk“.

16 – Right now, the city of Detroit is facing $20 billion in debt and unfunded liabilities. That breaks down to more than $25,000 per resident.

As Detroit Emergency Manager Kevyn Orr noted last week, it took a very long time for Detroit to get into this condition…

“What the average Detroiter needs to understand is that where we are right now is a culmination of years and years and years of kicking the can down the road,” said Orr, adding that his proposal should not be seen as a “hostile act” but as a step in the right direction.

Does that sound familiar?

It should.

U.S. politicians have also been kicking the can down the road for “years and years and years”.

But eventually you can’t kick the can down the road anymore.

Sometimes it is helpful to step back and look at what we have done to ourselves over the past several decades.

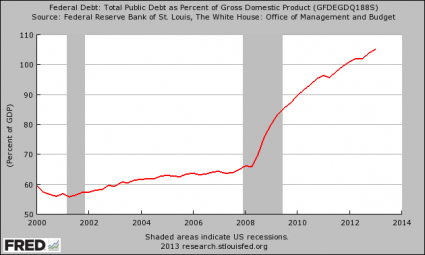

For example, back in 1980 the U.S. national debt was less than one trillion dollars. Today, it is rapidly approaching 17 trillion dollars.

And our debt binge has greatly accelerated under Barack Obama.

During Barack Obama’s first term, the federal government accumulated more debt than it did under the first 42 U.S presidents combined.

Isn’t that insane?

In fact, if you started paying off just the new debt that the U.S. has accumulated during the Obama administration at the rate of one dollar per second, it would take more than 184,000 years to pay it off.

The following are a lot more facts about our exploding national debt from one of my previous articles entitled “55 Facts About The Debt And U.S. Government Finances That Every American Voter Should Know“…

#1 While Barack Obama has been president, the U.S. government has spent about 11 dollars for every 7 dollars of revenue that it has actually brought in.

#2 During the fiscal year that just ended, the U.S. government took in 2.449 trillion dollars but it spent 3.538 trillion dollars.

#3 During fiscal year 2011, over a trillion dollars of government money was spent on 83 different welfare programs, and those numbers do not even include Social Security or Medicare.

#4 Over the past four years, welfare spending has increased by 32 percent. In inflation-adjusted dollars, spending on those programs has risen by 378 percent over the past 30 years. At this point, more than 100 million Americans are enrolled in at least one welfare program run by the federal government. Once again, these figures do not even include Social Security or Medicare.

#5 Over the past year, the number of Americans getting a free cell phone from the federal government has grown by 43 percent. Now more than 16 million Americans are enjoying what has come to be known as an “Obamaphone”.

#6 When Barack Obama first entered the White House, about 32 million Americans were on food stamps. Now, 47 million Americans are on food stamps. And this has happened during what Obama refers to as “an economic recovery”.

#7 The U.S. government recently spent 27 million dollars on pottery classes in Morocco.

#8 The U.S. Department of Agriculture recently spent $300,000 to encourage Americans to eat caviar at a time when more families than ever are having a really hard time just trying to put any food on the table at all.

#9 During 2012, the National Science Foundation spent $516,000 to support the creation of a video game called “Prom Week”, which apparently simulates “all the social interactions of the event.”

#10 The U.S. Department of Agriculture gave the largest snack food maker in the world (PepsiCo Inc.) a total of 1.3 million dollars in corporate welfare that was used to help build “a Greek yogurt factory in New York.”

#11 The National Science Foundation recently gave researchers at Purdue University $350,000. They used part of that money to help fund a study that discovered that if golfers imagine that a hole is bigger it will help them with their putting.

#12 If you can believe it, $10,000 from the federal government was actually used to purchase talking urinal cakes up in Michigan.

#13 The National Science Foundation recently gave a whopping $697,177 to a New York City-based theater company to produce a musical about climate change.

#14 The National Institutes of Health recently gave $666,905 to a group of researchers that is studying the benefits of watching reruns on television.

#15 The National Science Foundation has given 1.2 million dollars to a team of “scientists” that is spending part of that money on a study that is seeking to determine whether elderly Americans would benefit from playing World of Warcraft or not.

#16 The National Institutes of Health recently gave $548,731 to a team of researchers that concluded that those that drink heavily in their thirties also tend to feel more immature.

#17 The National Science Foundation recently spent $30,000 on a study to determine if “gaydar” actually exists. This is the conclusion that the researchers reached at the end of the study…

“Gaydar is indeed real and… its accuracy is driven by sensitivity to individual facial features”

#18 Back in 2011, the National Institutes of Health spent $592,527 on a study that sought to figure out once and for all why chimpanzees throw poop.

#19 The U.S. government spends more on the military than China, Russia, Japan, India, and the rest of NATO combined. In fact, the United States accounts for 41.0% of all military spending on the planet. China is next with only 8.2%.

#20 In a previous article, I noted that close to 500,000 federal employees now make at least $100,000 a year.

#21 In 2006, only 12 percent of all federal workers made $100,000 or more per year. Now, approximately 22 percent of all federal workers do.

#22 If you can believe it, there are 77,000 federal workers that make more than the governors of their own states do.

#23 During 2010, the average federal employee in the Washington D.C. area received total compensation worth more than $126,000.

#24 The U.S. Department of Defense had just nine civilians earning $170,000 or more back in 2005. When Barack Obama became president, the U.S. Department of Defense had 214 civilians earning $170,000 or more. By June 2010, the U.S. Department of Defense had 994 civilians earning $170,000 or more.

#25 During 2010, compensation for federal employees came to a grand total of approximately 447 billion dollars.

#26 If you can believe it, close to 15,000 retired federal employees are currently collecting federal pensions for life worth at least $100,000 annually. That list includes such names as Newt Gingrich, Bob Dole, Trent Lott, Dick Gephardt and Dick Cheney.

#27 During 2010, the federal government spent $33,387 on the hair care needs of U.S. Senators.

#28 During 2010, U.S. Senators pulled $72,370 out of the “Senate Restaurant Fund”.

#29 During 2010, an average of $4,005,900 of U.S. taxpayer money was spent on “personal” and “office” expenses per Senator.

#30 In 2013, 3.7 million dollars will be spent to support the lavish lifestyles of former presidents such as George W. Bush and Bill Clinton.

#31 During 2011, the federal government spent a total of 1.4 BILLION dollars just on the Obamas.

#32 When you combine all federal government spending, all state government spending and all local government spending, it comes to approximately 41 percent of U.S. GDP. But don’t worry, all of our politicians insist that this is not socialism.

#33 As I have written about previously, less than 30 percent of all Americans lived in a home where at least one person received financial assistance from the federal government back in 1983. Today, that number is sitting at an all-time high of 49 percent.

#34 Back in 1990, the federal government accounted for just 32 percent of all health care spending in America. This year, it is being projected that the federal government will account for more than 50 percent of all health care spending in the United States.

#35 The number of Americans on Medicaid soared from 34 million in 2000 to 54 million in 2011, and it is being projected that Obamacare will add 16 million more Americans to the Medicaid rolls.

#36 In one of my previous articles, I discussed how it is being projected that the number of Americans on Medicare will grow from 50.7 million in 2012 to 73.2 million in 2025.

#37 If you can believe it, Medicare is facing unfunded liabilities of more than 38 trillion dollars over the next 75 years. That comes to approximately $328,404 for each and every household in the United States.

#38 In the United States today, more than 61 million Americans receive some form of Social Security benefits. By 2035, that number is projected to soar to a whopping 91 million.

#39 Overall, the Social Security system is facing a 134 trillion dollar shortfall over the next 75 years.

#40 When Barack Obama first took office, the U.S. national debt was about 10.6 trillion dollars. Now it is about 16.7 trillion dollars. That is an increase of 6.1 trillion dollars in a little more than 4 years.

#41 The federal government has now run a budget deficit of more than a trillion dollars for four years in a row.

#42 If right this moment you went out and started spending one dollar every single second, it would take you more than 31,000 years to spend one trillion dollars.

#43 If you were alive when Jesus Christ was born and you spent one million dollars every single day since that point, you still would not have spent one trillion dollars by now.

#44 Some suggest that “taxing the rich” is the answer. Well, if Bill Gates gave every single penny of his entire fortune to the U.S. government, it would only cover the U.S. budget deficit for 15 days.

#45 If the federal government used GAAP accounting standards like publicly traded corporations do, the real federal budget deficit for 2011 would have been 5 trillion dollars instead of 1.3 trillion dollars.

#46 The United States already has more government debt per capita than Greece, Portugal, Italy, Ireland or Spain does.

#47 At this point, the United States government is responsible for more than a third of all the government debt in the entire world.

#48 The amount of U.S. government debt held by foreigners is about 5 times larger than it was just a decade ago.

#49 Between 2007 and 2010, U.S. GDP grew by only 4.26%, but the U.S. national debt soared by 61% during that same time period.

#50 The U.S. national debt is now more than 37 times larger than it was when Richard Nixon took us off the gold standard.

#51 The U.S. national debt is now more than 5000 times larger than it was when the Federal Reserve was first created.

#52 The U.S. national debt jumped more on the very first day of fiscal year 2013 than it did from 1776 to 1941 combined.

#53 Historically, the interest rate on 10 year U.S. Treasuries has averaged 6.68 percent. If the average interest rate on U.S. government debt rose to that level today, the U.S. government would find itself spending more than a trillion dollars per year just on interest on the national debt.

#54 A recently revised IMF policy paper entitled “An Analysis of U.S. Fiscal and Generational Imbalances: Who Will Pay and How?” projects that U.S. government debt will rise to about 400 percent of GDP by the year 2050.

#55 Boston University economist Laurence Kotlikoff is warning that the U.S. government is facing a gigantic tsunami of unfunded liabilities in the coming years that we are counting on our children and our grandchildren to pay. Kotlikoff speaks of a “fiscal gap” which he defines as “the present value difference between projected future spending and revenue”. His calculations have led him to the conclusion that the federal government is facing a fiscal gap of 222 trillion dollars in the years ahead.

Please share this article with as many people as you can. We are in the process of committing national financial suicide and time is rapidly running out to do anything about it.

Just like Detroit, a day is rapidly approaching when America will not be able to kick the can down the road anymore.

Sadly, our politicians don’t seem inclined to do anything about it and most of the population seems to think that our exploding national debt is not a significant problem.

By the time it becomes clear how wrong they were, it will be far too late to do anything about it.

Retail sales during the four day Thanksgiving weekend were down a whopping 11 percent from last year. This is a “make or break” time of the year for many retailers, and if things don’t turn around during the coming weeks we could see a tsunami of store closings in January and February. As you read this article, there is already more than a billion square feet of retail space sitting empty in the United States. Many have described the ongoing collapse of the retail industry as an “apocalypse”, and this apocalypse appears to be accelerating. Yes, the shift to online retailers is a significant factor, but as you will see below even online retailers struggled over the holiday weekend. The sad truth of the matter is that U.S. consumers are tapped out and are drowning in debt at this point, so they simply do not have as much money to spend as they once did.

Retail sales during the four day Thanksgiving weekend were down a whopping 11 percent from last year. This is a “make or break” time of the year for many retailers, and if things don’t turn around during the coming weeks we could see a tsunami of store closings in January and February. As you read this article, there is already more than a billion square feet of retail space sitting empty in the United States. Many have described the ongoing collapse of the retail industry as an “apocalypse”, and this apocalypse appears to be accelerating. Yes, the shift to online retailers is a significant factor, but as you will see below even online retailers struggled over the holiday weekend. The sad truth of the matter is that U.S. consumers are tapped out and are drowning in debt at this point, so they simply do not have as much money to spend as they once did.