Why are young people in America so frustrated these days? You are about to find out. Most young adults started out having faith in the system. They worked hard, they got good grades, they stayed out of trouble and many of them went on to college. But when their educations where over, they discovered that the good jobs that they had been promised were not waiting for them at the end of the rainbow. Even in the midst of this so-called “economic recovery”, the full-time employment rate for Americans under the age of 30 continues to fall. And incomes for that age group continue to fall as well. At the same time, young adults are dealing with record levels of student loan debt. As a result, more young Americans than ever are putting off getting married and having families, and more of them than ever are moving back in with their parents.

Why are young people in America so frustrated these days? You are about to find out. Most young adults started out having faith in the system. They worked hard, they got good grades, they stayed out of trouble and many of them went on to college. But when their educations where over, they discovered that the good jobs that they had been promised were not waiting for them at the end of the rainbow. Even in the midst of this so-called “economic recovery”, the full-time employment rate for Americans under the age of 30 continues to fall. And incomes for that age group continue to fall as well. At the same time, young adults are dealing with record levels of student loan debt. As a result, more young Americans than ever are putting off getting married and having families, and more of them than ever are moving back in with their parents.

It can be absolutely soul crushing when you discover that the “bright future” that the system had been promising you for so many years turns out to be a lie. A lot of young people ultimately give up on the system and many of them end up just kind of drifting aimlessly through life. The following is an example from a recent Wall Street Journal article…

James Roy, 26, has spent the past six years paying off $14,000 in student loans for two years of college by skating from job to job. Now working as a supervisor for a coffee shop in the Chicago suburb of St. Charles, Ill., Mr. Roy describes his outlook as “kind of grim.”

“It seems to me that if you went to college and took on student debt, there used to be greater assurance that you could pay it off with a good job,” said the Colorado native, who majored in English before dropping out. “But now, for people living in this economy and in our age group, it’s a rough deal.”

Young adults as a group have been experiencing a tremendous amount of economic pain in recent years. The following are 30 statistics about Americans under the age of 30 that will blow your mind…

#1 The labor force participation rate for men in the 18 to 24 year old age bracket is at an all-time low.

#2 The ratio of what men in the 18 to 29 year old age bracket are earning compared to the general population is at an all-time low.

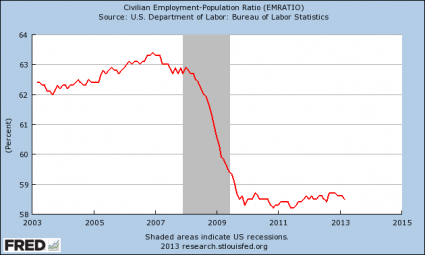

#3 Only about a third of all adults in their early 20s are working a full-time job.

#4 For the entire 18 to 29 year old age bracket, the full-time employment rate continues to fall. In June 2012, 47 percent of that entire age group had a full-time job. One year later, in June 2013, only 43.6 percent of that entire age group had a full-time job.

#5 Back in the year 2000, 80 percent of men in their late 20s had a full-time job. Today, only 65 percent do.

#6 In 2007, the unemployment rate for the 20 to 29 year old age bracket was about 6.5 percent. Today, the unemployment rate for that same age group is about 13 percent.

#7 American families that have a head of household that is under the age of 30 have a poverty rate of 37 percent.

#8 During 2012, young adults under the age of 30 accounted for 23 percent of the workforce, but they accounted for a whopping 36 percent of the unemployed.

#9 During 2011, 53 percent of all Americans with a bachelor’s degree under the age of 25 were either unemployed or underemployed.

#10 At this point about half of all recent college graduates are working jobs that do not even require a college degree.

#11 The number of Americans in the 16 to 29 year old age bracket with a job declined by 18 percent between 2000 and 2010.

#12 According to one survey, 82 percent of all Americans believe that it is harder for young adults to find jobs today than it was for their parents to find jobs.

#13 Incomes for U.S. households led by someone between the ages of 25 and 34 have fallen by about 12 percent after you adjust for inflation since the year 2000.

#14 In 1984, the median net worth of households led by someone 65 or older was 10 times larger than the median net worth of households led by someone 35 or younger. Today, the median net worth of households led by someone 65 or older is 47 times larger than the median net worth of households led by someone 35 or younger.

#15 In 2011, SAT scores for young men were the worst that they had been in 40 years.

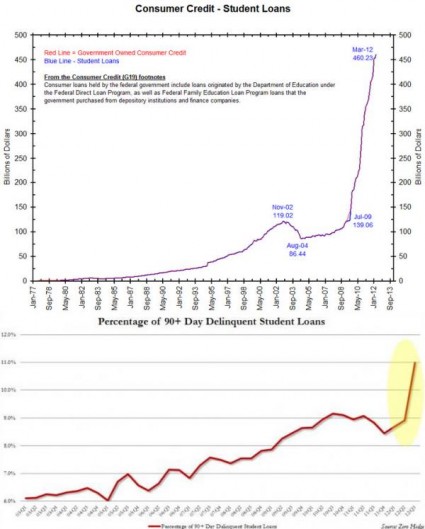

#16 Incredibly, approximately two-thirds of all college students graduate with student loans.

#17 According to the Federal Reserve, the total amount of student loan debt has risen by 275 percent since 2003.

#18 In America today, 40 percent of all households that are led by someone under the age of 35 are paying off student loan debt. Back in 1989, that figure was below 20 percent.

#19 The total amount of student loan debt in the United States now exceeds the total amount of credit card debt in the United States.

#20 According to the U.S. Department of Education, 11 percent of all student loans are at least 90 days delinquent.

#21 The student loan default rate in the United States has nearly doubled since 2005.

#22 One survey found that 70% of all college graduates wish that they had spent more time preparing for the “real world” while they were still in college.

#23 In the United States today, there are more than 100,000 janitors that have college degrees.

#24 In the United States today, 317,000 waiters and waitresses have college degrees.

#25 Today, an all-time low 44.2 percent of all Americans between the ages of 25 and 34 are married.

#26 According to the Pew Research Center, 57 percent of all Americans in the 18 to 24 year old age bracket lived with their parents during 2012.

#27 One poll discovered that 29 percent of all Americans in the 25 to 34 year old age bracket are still living with their parents.

#28 Young men are nearly twice as likely to live with their parents as young women the same age are.

#29 Overall, approximately 25 million American adults are living with their parents according to Time Magazine.

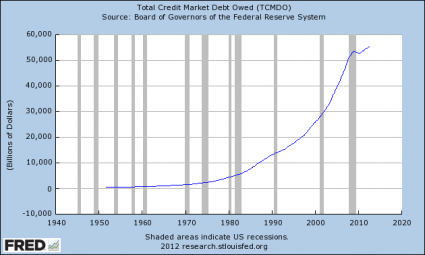

#30 Young Americans are becoming increasingly frustrated that previous generations have saddled them with a nearly 17 trillion dollar national debt that they are expected to make payments on for the rest of their lives.

And this trend is not just limited to the United States. As I have written about frequently, unemployment rates for young adults throughout Europe have been soaring to unprecedented heights. For example, the unemployment rate for those under the age of 25 in Italy has now reached 40.1 percent.

Simon Black of the Sovereign Man blog discussed this global trend in a recent article on his website…

Youth unemployment rates in these countries are upwards of 40% to nearly 70%. The most recent figures published by the Italian government show yet another record high in youth unemployment.

An entire generation is now coming of age without being able to leave the nest or have any prospect of earning a decent wage in their home country.

This underscores an important point that I’ve been writing about for a long time: young people in particular get the sharp end of the stick.

They’re the last to be hired, the first to be fired, the first to be sent off to fight and die in foreign lands, and the first to have their benefits cut.

And if they’re ever lucky enough to find meaningful employment, they can count on working their entire lives to pay down the debts of previous generations through higher and higher taxes.

But when it comes time to collect… finally… those benefits won’t be there for them.

Meanwhile, the overall economy continues to get even weaker.

In the United States, Gallup’s daily economic confidence index is now the lowest that it has been in more than a year.

For young people that are in high school or college right now, the future does not look bright. In fact, this is probably as good as the U.S. economy is going to get. It is probably only going to be downhill from here.

The system is failing, and young people are going to become even angrier and even more frustrated.

So what will that mean for our future?

Please feel free to share what you think by posting a comment below…