How much is 1,000,000,000,000,000 yen worth? Well, a quadrillion yen is worth approximately 10.5 trillion dollars. It is an amount of money that is larger than the “the economies of Germany, France and the U.K. combined“. It is such an astounding amount of debt that it is hard to even get your mind around it. The government debt to GDP ratio in Japan will reach 247 percent this year, and the Japanese currently spend about 50 percent of all central government tax revenue on debt service. Realistically, there are only two ways out of this overwhelming debt trap for the Japanese. Either they default or they try to inflate the debt away. At this point, the Japanese have chosen to try to inflate the debt away. They have initiated the greatest quantitative easing experiment that a major industrialized nation has attempted since the days of the Weimar Republic. Over the next two years, the Bank of Japan plans to zap 60 trillion yen into existence out of thin air and use it to buy government bonds. By the time this program is over, the monetary base in Japan will have approximately doubled. But authorities in Japan are desperate. They know that the Japanese debt bomb could set off global panic at any time, and they are trying to find a way out that will not cause too much pain.

How much is 1,000,000,000,000,000 yen worth? Well, a quadrillion yen is worth approximately 10.5 trillion dollars. It is an amount of money that is larger than the “the economies of Germany, France and the U.K. combined“. It is such an astounding amount of debt that it is hard to even get your mind around it. The government debt to GDP ratio in Japan will reach 247 percent this year, and the Japanese currently spend about 50 percent of all central government tax revenue on debt service. Realistically, there are only two ways out of this overwhelming debt trap for the Japanese. Either they default or they try to inflate the debt away. At this point, the Japanese have chosen to try to inflate the debt away. They have initiated the greatest quantitative easing experiment that a major industrialized nation has attempted since the days of the Weimar Republic. Over the next two years, the Bank of Japan plans to zap 60 trillion yen into existence out of thin air and use it to buy government bonds. By the time this program is over, the monetary base in Japan will have approximately doubled. But authorities in Japan are desperate. They know that the Japanese debt bomb could set off global panic at any time, and they are trying to find a way out that will not cause too much pain.

Unfortunately, the only way that this bizarre quantitative easing program will work is if investors in Japanese bonds act very, very irrationally. You see, the only way that Japan has been able to pile up this much debt in the first place is because they have been able to borrow gigantic piles of money at super low interest rates.

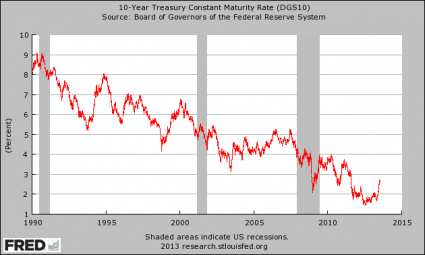

Right now, the yield on 10 year Japanese bonds is sitting at an absurdly low 0.76%. But even with such ridiculously low interest rates, the central government of Japan is still spending about half of all tax revenue on debt service.

If interest rates go up, the game is over.

But now that the Japanese government has announced that it plans to double the monetary base, it would be extremely irrational for investors not to demand higher rates on Japanese government debt. After all, why would you want to loan money to the Japanese government for less than one percent a year when the purchasing power of your money could potentially be halved over the next two years?

Amazingly, this is exactly what the Japanese government is counting on. They are counting on being able to wildly print up money and monetize debt, but also keep yields on Japanese bonds at insanely low levels at the same time.

For the moment, it is actually working. Investors in Japanese bonds are behaving very, very irrationally.

But if that changes at some point, we could potentially be looking at the greatest Asian economic crisis of all time.

And there are some very sharp minds out there that believe that is exactly what is going to happen.

For example, the founder of Hayman Capital Management, Kyle Bass, has been sounding the alarm about Japan for a long time. He correctly predicted the subprime mortgage meltdown, and in the process he made hundreds of millions of dollars for his clients. Now he believes that the next major crash is going to be in Japan.

According to Bass, the bond bubble in Japan is so large that once it begins to implode fear is going to start spreading like wildfire…

Remember, Japanese banks in general have 900% of their tangible assets invested in JGBs that are the most negatively convex instrument you can put into a portfolio. Assume for instance that a bank holds a 10 year bond yielding 80 basis points. A 100 basis point move will cost the JGB investor about 10 years of expected interest payments.

Think about the psychology of all the players and financial implications if rates do move 100 basis points. Think about the solvency of a nation which currently spends 50% of its central government tax revenues on debt service, half of which earns the lowest yields of any country in the world.

You can’t look at this as a simple question. You need to think about this as a multivariate equation. You have to think about the incentives and the fears of all the participants. And you need to think about the fiscal sustainability of the government.

If rates even rise by a full percentage point, it could start a stampede toward the exits that nobody in the entire world would be able to control…

I ran a survey of 1,009 Japanese investors where we asked: “If rates were to move up 100 basis points, would that engender more confidence and make you want to buy more JGBs?” or, “Would you take your money elsewhere, even if it were hamstringing your government’s ability to operate?” 8 – 9% of respondents that said that they would buy more bonds and almost 80% said they would run, not walk the other way.

For much more on this, you can watch a video of Kyle Bass discussing why Japan is doomed right here.

And of course Japan is not the only “debt bomb” that could potentially go off over in Asia. As I mentioned in another article, the major problem over in China is the level of private debt…

In China, the big problem is the absolutely stunning growth of private domestic debt. According to a recent World Bank report, the total amount of credit in China has risen from 9 trillion dollars in 2008 to 23 trillion dollars today.

That increase is roughly equivalent to the entire U.S. commercial banking system.

There is simply way, way too much debt in our world today. Never before has there been so much red ink all over the planet at the same time.

Many in the mainstream media insist that this party can go on indefinitely.

But that is what they said about the housing bubble too.

Sadly, the truth is that every financial bubble eventually bursts, and this global debt bubble will be no exception.

I hope that you are getting prepared while you still can.

When you add maturing debt to the new debt that the federal government is accumulating, the total is quite eye catching. You see, the truth is that the U.S. government must not only borrow enough money to fund government spending for this year, it must also “roll over” existing debt that has reached maturity. Of course the government never actually pays any of that debt off. Instead, it essentially takes out new debts to cover the old ones. So the U.S. government is actually borrowing far more money each year than most Americans realize. For fiscal year 2013, the U.S. budget deficit will be about

When you add maturing debt to the new debt that the federal government is accumulating, the total is quite eye catching. You see, the truth is that the U.S. government must not only borrow enough money to fund government spending for this year, it must also “roll over” existing debt that has reached maturity. Of course the government never actually pays any of that debt off. Instead, it essentially takes out new debts to cover the old ones. So the U.S. government is actually borrowing far more money each year than most Americans realize. For fiscal year 2013, the U.S. budget deficit will be about