If you are a man living in America today, to a large degree your value to society is determined by how much money you make. It should not be that way, but that is how our society works. And if you do not have a job at all and you cannot take care of your own family, then almost everyone looks down on you even if it is not your fault. Once you are unemployed, it becomes the number one defining factor in your life. Yes, there are a few people that may look at you in the same way, but in the eyes of most you will now be less of a man. Sadly, this is particularly true when it comes to romantic relationships. Unemployed men tend to have unhappier marriages, they tend to divorce more frequently, and as you will see below approximately 75 percent of all American women do not have any interest in dating unemployed men. Unfortunately for American men, the decline of the U.S. economy in recent years has had a disproportionate impact on them. The past five years have been the worst years for employment for American men in the post-World War II era, and things are only going to get worse from here.

If you are a man living in America today, to a large degree your value to society is determined by how much money you make. It should not be that way, but that is how our society works. And if you do not have a job at all and you cannot take care of your own family, then almost everyone looks down on you even if it is not your fault. Once you are unemployed, it becomes the number one defining factor in your life. Yes, there are a few people that may look at you in the same way, but in the eyes of most you will now be less of a man. Sadly, this is particularly true when it comes to romantic relationships. Unemployed men tend to have unhappier marriages, they tend to divorce more frequently, and as you will see below approximately 75 percent of all American women do not have any interest in dating unemployed men. Unfortunately for American men, the decline of the U.S. economy in recent years has had a disproportionate impact on them. The past five years have been the worst years for employment for American men in the post-World War II era, and things are only going to get worse from here.

Yes, unemployed women go through similar things. I do not mean to downplay the economic suffering of unemployed women at all. In fact, I write about it quite frequently.

Today, however, I want to focus on how the steadily declining U.S. economy is affecting men. If you are a single man and you are unemployed, that automatically means that most single women will not be interested in you at all. At least that is what one very shocking survey discovered…

Of the 925 single women surveyed, 75 percent said they’d have a problem with dating someone without a job. Only 4 percent of respondents asked whether they would go out with an unemployed man answered “of course.”

“Not having a job will definitely make it harder for men to date someone they don’t already know,” Irene LaCota, a spokesperson for It’s Just Lunch, said in a press release. “This is the rare area, compared to other topics we’ve done surveys on, where women’s old-fashioned beliefs about sex roles seem to apply.”

So what would happen if things were reversed and that same question was asked to men?

Well, it turns out that there is a big difference.

When men were asked that exact same question, the results were absolutely startling…

On the other hand, the prospect of dating an unemployed woman was not a problem for nearly two-thirds of men. In fact, 19 percent of men said they had no reservations and 46 percent of men said they were positive they would date an unemployed woman.

Perhaps traditional gender roles are not quite as dead as many people believe that they are.

And as I mentioned earlier, the declining economy is hitting men even harder than it is hitting women. Yes, millions upon millions of women are deeply suffering in this economy. There is no doubt about that. But men are actually having an even more difficult time than women are.

The following are 12 signs that the decline of the U.S. economy is having a disproportionate impact on men…

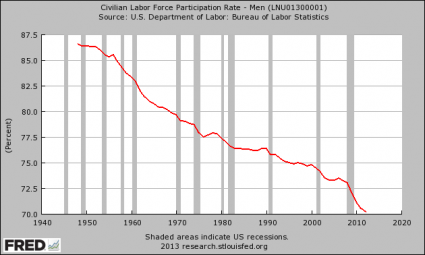

#1 The labor force participation rate for men is now at an all-time low…

#2 During the last recession, men lost twice as many jobs as women did. All of the jobs that women in the United States lost during the last recession have been regained, but only about 70 percent of the jobs that men lost during the last recession have been regained. Meanwhile, the size of the overall population continues to grow rapidly.

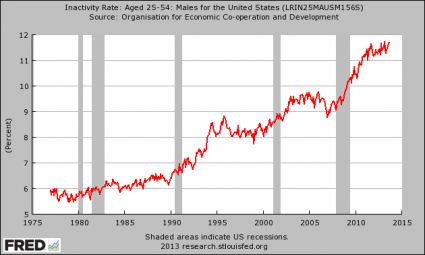

#3 The inactivity rate for men has risen even higher since the end of the last recession and is now hovering near an all-time record high…

#4 Since 2010, about a million construction workers have either been forced to switch industries or have disappeared from the labor force entirely. This has had a disproportionate impact on men.

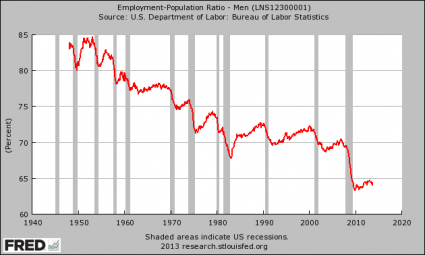

#5 Back in the 1950s, more than 80 percent of all men in the United States had jobs. Just before the last recession, about 70 percent of all men in the United States had jobs. Today, only 64 percent of all men in the United States have jobs…

#6 Back in the 1980s, more than 20 percent of the jobs in the United States were manufacturing jobs. Today, only about 9 percent of the jobs in the United States are manufacturing jobs. This has had a disproportionate impact on men.

#7 According to the Economic Policy Institute, the U.S. economy loses 9,000 jobs for every 1 billion dollars of goods that are imported. A disproportionate percentage of those job losses tend to come from male-dominated industries such as manufacturing. Since 1975, the United States has run a total trade deficit with the rest of the world of more than 8 trillion dollars, and right now there are more than 102 million working age Americans that do not have a job.

#8 Between 1969 and 2009, the median wages earned by American men between the ages of 30 and 50 dropped by 27 percent after you account for inflation.

#9 According to the Economic Policy Institute, the “real entry-level hourly wage for men who recently graduated from high school” has declined from $15.64 in 1979 to $11.68 today.

#10 Thanks to Obama administration policies which are systematically killing off small businesses in the United States, the percentage of self-employed Americans is at an all-time low today. This has had a disproportionate impact on men.

#11 According to CNN, American men in the 25 to 34-year-old age bracket are nearly twice as likely to live with their parents as women the same age are.

#12 According to Time Magazine, unemployed men are significantly more likely to get divorced than employed men are.

When a man cannot take care of his own family, it can be absolutely soul crushing. Though many would like to deny this, the truth is that men are still considered to be the primary breadwinners in society today. When a man finds that he cannot provide what his family needs no matter how hard he tries, it can be really easy to descend into a spiral of despair, depression and self-pity.

Unfortunately, the U.S. economy is not producing nearly enough jobs for everyone anymore and it never will again. Meanwhile, the quality of our jobs continues to decline at a staggering pace.

What all of this means is that the number of Americans living in poverty is going to continue to grow, and there will be lots more men that feel worthless because they can’t provide for their families.

The following is one example of a single dad that is forced to turn to the government for assistance because he cannot provide for his children on his own…

It means Lyman Curtis, single dad of five kids, will only be able to reliably heat his home in Dexter, Maine, for the first half of this winter, maybe through February.

After that, Curtis will drive to the local gas station to buy kerosene oil in 5-gallon increments — all he can afford to buy at one time.

“I know a lot of people who do it that way, because there’s just not enough money to heat your home and pay for groceries in your everyday life,” said Curtis, 38, who is the primary caregiver for his kids and relies on disability benefits and food stamps to survive.

Nobody should ever look down on someone like Lyman Curtis. He is doing the best that he can.

At this point our economy is kind of like a very twisted game of musical chairs. If your family is doing well at the moment, you should not be too complacent because the next time the music stops you might be the one that loses a job.

In recent years, millions upon millions of Americans have lost good jobs, and in most cases it was due to forces beyond their control.

And as the economy continues to deteriorate, Americans are going to become even more angry and even more frustrated. In fact, one recent survey found that 60 percent of all Americans “report feeling angry or irritable“.

But we have not even reached the next major wave of the economic collapse yet.

How “angry” and “irritable” will people feel once millions more Americans lose their jobs?

That is something to think about.

So what do you think about all of this?

What do you think about the fact that most women would not even consider dating an unemployed man?

Please feel free to share your thoughts by posting a comment below…