When one of our major politicians gets something exactly right, we should applaud them for it. In this case, Donald Trump’s call to audit the Federal Reserve is dead on correct. Most Americans don’t realize this, but the Federal Reserve has far more power over the economy than anyone else does – including Barack Obama. Financial markets all over the planet gyrate wildly at the smallest comment from Fed officials, and virtually every boom and bust cycle over the past 100 years can be traced directly back to specific decisions made by the Federal Reserve. We get all excited about what various presidential candidates say that they “will do for the economy”, but in the end it is the Fed that is holding all of the cards. The funny thing is that the Federal Reserve is not even part of the federal government. It is an independent private central bank that was designed by very powerful Wall Street interests a little over 100 years ago. It is at the heart of the debt-based financial system which is eating away at America like cancer, and it has no direct accountability to the American people whatsoever.

When one of our major politicians gets something exactly right, we should applaud them for it. In this case, Donald Trump’s call to audit the Federal Reserve is dead on correct. Most Americans don’t realize this, but the Federal Reserve has far more power over the economy than anyone else does – including Barack Obama. Financial markets all over the planet gyrate wildly at the smallest comment from Fed officials, and virtually every boom and bust cycle over the past 100 years can be traced directly back to specific decisions made by the Federal Reserve. We get all excited about what various presidential candidates say that they “will do for the economy”, but in the end it is the Fed that is holding all of the cards. The funny thing is that the Federal Reserve is not even part of the federal government. It is an independent private central bank that was designed by very powerful Wall Street interests a little over 100 years ago. It is at the heart of the debt-based financial system which is eating away at America like cancer, and it has no direct accountability to the American people whatsoever.

The Fed has been around for so long that most people assume that we need it.

But the truth is that we don’t actually need the Federal Reserve. In fact, the greatest period of economic growth in United States history happened during the decades before the Federal Reserve was created.

A little over 100 years ago, very powerful forces on Wall Street successfully pushed for the creation of an immensely powerful central bank, and since that time the value of the U.S. dollar has fallen by about 98 percent and our national debt has gotten more than 5000 times larger.

The Federal Reserve does whatever it feels like doing, and Fed officials insist that the institution must remain “independent” and “above politics” because monetary policy is too important to entrust to the American people.

To me, this is absolutely ridiculous. Everything else, including our national defense, is subject to the normal political process, and yet the decisions made by the Fed are so “important” that the American people can’t have a voice?

It is high time that the American people begin to learn what the Federal Reserve is really all about, and that can start with a full, comprehensive audit of all of the Federal Reserve’s activities. Yesterday, Donald Trump came out in favor of such an audit…

Previously, Trump has made quite a few comments that were very critical of the Fed. For example, last year he told Bloomberg News that he believed that the Federal Reserve was “creating a bubble”…

“In terms of real estate, if I want to develop … from that standpoint I like low interest rates. From the country’s standpoint, I’m just not sure it’s a very good thing, because I really do believe we’re creating a bubble.”

And of course Trump was exactly right about that too. By pushing interest rates to artificially low levels and creating billions upon billions of dollars out of thin air during the quantitative easing era, stock prices were driven to ridiculously high levels. Now that the artificial support has been withdrawn, stocks are beginning to crash, and the financial collapse which is starting to happen is going to be far worse than it otherwise would have been because of the Fed’s actions. The following comes from one of my previous articles…

As stocks continue to crash, you can blame the Federal Reserve, because the Fed is more responsible for creating the current financial bubble that we are living in than anyone else. When the Federal Reserve pushed interest rates all the way to the floor and injected lots of hot money into the financial markets during their quantitative easing programs, this pushed stock prices to wildly artificial levels. The only way that it would have been possible to keep stock prices at those wildly artificial levels would have been to keep interest rates ultra-low and to keep recklessly creating lots of new money. But now the Federal Reserve has ended quantitative easing and has embarked on a program of very slowly raising interest rates. This is going to have very severe consequences for the markets, but Janet Yellen doesn’t seem to care.

I don’t understand why so many Americans continue to support the Federal Reserve.

We don’t need a bunch of central planners setting interest rates and determining monetary policy. We are supposed to have a free market system, and the free market should be setting interest rates – not the Federal Reserve.

Unfortunately, just about every nation on the entire planet now has a central bank. Even though the nations of the world can’t agree on much, somehow central banking has been adopted virtually everywhere. At this point, more than 99.9% of the population of the world lives in a country that has a central bank.

There are still some minor island countries such as the Federated States of Micronesia that do not have a central bank, but the only major nation not to have one right now is North Korea. And nobody in their right mind would ever want to live there.

So how in the world did this happen?

Did the people of the world willingly choose this debt-based system or was it imposed upon them?

To my knowledge, there has never been a single vote where the population of a nation has willingly chosen to establish a central bank. I could be wrong about this, but I have never heard of one.

It is the elite that have always wanted central banking, and now they pretty much have the entire planet in their grasp.

That is why we should applaud Donald Trump when he stands up to the elite. And it isn’t just regarding the Fed that he has done this. The following comes from an excellent article that was just written by Dan Lyman…

Ultimately, Trump knows it is the global elite who have pried our borders wide open. He knows it is THEY who are responsible for the tens of millions of Third Worlders pouring into our nations. He knows that THEY are the monsters who need the world to be constantly at war. He knows THEY are radically altering our food supply with GMOs and poisonous chemicals. He knows THEY are responsible for poisoning our drinking water, filling our skies and air supplies with toxic waste, genociding our unborn children, collecting data on all citizens to implement the Orwellian police state, forcing poison into our babies’ veins – and soon the rest of us, redistributing what remains of our wealth under the guises of ‘saving the planet’ or ‘refugee aid,’ allowing and funding the ISIS Islamofascists to decimate places like Syria and Iraq in Satanic fashion, promoting the psychotic LGBT Nazis to goose-step all over our religious liberties and gender-privacy in school bathrooms. If there is a societal cancer metastasizing somewhere, it can usually be traced back to the same sources.

Yes, there are many things that we can criticize Trump and the other Republican candidates for. But when they nail something, we should be willing to admit that they got something right.

In this case, Donald Trump is absolutely correct to call for an audit of the Fed. As I promised in the title of this article, I want to share 100 reasons why the Fed should be audited. The following list has been adapted from one of my previous articles…

#1 We like to think that we have a government “of the people, by the people, for the people”, but the truth is that an unelected, unaccountable group of central planners has far more power over our economy than anyone else in our society does.

#2 The Federal Reserve is actually “independent” of the government. In fact, the Federal Reserve has argued vehemently in federal court that it is “not an agency” of the federal government and therefore not subject to the Freedom of Information Act.

#3 The Federal Reserve openly admits that the 12 regional Federal Reserve banks are organized “much like private corporations“.

#4 The regional Federal Reserve banks issue shares of stock to the “member banks” that own them.

#5 100% of the shareholders of the Federal Reserve are private banks. The U.S. government owns zero shares.

#6 The Federal Reserve is not an agency of the federal government, but it has been given power to regulate our banks and financial institutions. This should not be happening.

#7 According to Article I, Section 8 of the U.S. Constitution, the U.S. Congress is the one that is supposed to have the authority to “coin Money, regulate the Value thereof, and of foreign Coin, and fix the Standard of Weights and Measures”. So why is the Federal Reserve doing it?

#8 If you look at a “U.S. dollar”, it actually says “Federal Reserve note” at the top. In the financial world, a “note” is an instrument of debt.

#9 In 1963, President John F. Kennedy issued Executive Order 11110 which authorized the U.S. Treasury to issue “United States notes” which were created by the U.S. government directly and not by the Federal Reserve. He was assassinated shortly thereafter.

#10 Many of the debt-free United States notes issued under President Kennedy are still in circulation today.

#11 The Federal Reserve determines what levels some of the most important interest rates in our system are going to be set at. In a free market system, the free market would determine those interest rates.

#12 The Federal Reserve has become so powerful that it is now known as “the fourth branch of government“.

#13 The greatest period of economic growth in U.S. history was when there was no central bank.

#14 The Federal Reserve was designed to be a perpetual debt machine. The bankers that designed it intended to trap the U.S. government in a perpetual debt spiral from which it could never possibly escape. Since the Federal Reserve was established 100 years ago, the U.S. national debt has gotten more than 5000 times larger.

#15 A permanent federal income tax was established the exact same year that the Federal Reserve was created. This was not a coincidence. In order to pay for all of the government debt that the Federal Reserve would create, a federal income tax was necessary. The whole idea was to transfer wealth from our pockets to the federal government and from the federal government to the bankers.

#16 The period prior to 1913 (when there was no income tax) was the greatest period of economic growth in U.S. history.

#17 Today, the U.S. tax code is about 13 miles long.

#18 From the time that the Federal Reserve was created until now, the U.S. dollar has lost 98 percent of its value.

#19 From the time that President Nixon took us off the gold standard until now, the U.S. dollar has lost 83 percent of its value.

#20 During the 100 years before the Federal Reserve was created, the U.S. economy rarely had any problems with inflation. But since the Federal Reserve was established, the U.S. economy has experienced constant and never ending inflation.

#21 In the century before the Federal Reserve was created, the average annual rate of inflation was about half a percent. In the century since the Federal Reserve was created, the average annual rate of inflation has been about 3.5 percent.

#22 The Federal Reserve has stripped the middle class of trillions of dollars of wealth through the hidden tax of inflation.

#23 The size of M1 has nearly doubled since 2008 thanks to the reckless money printing that the Federal Reserve has been doing.

#24 The Federal Reserve has been starting to behave like the Weimar Republic, and we all remember how that ended.

#25 The Federal Reserve has been consistently lying to us about the level of inflation in our economy. If the inflation rate was still calculated the same way that it was back when Jimmy Carter was president, the official rate of inflation would be somewhere between 8 and 10 percent today.

#26 Since the Federal Reserve was created, there have been 18 distinct recessions or depressions: 1918, 1920, 1923, 1926, 1929, 1937, 1945, 1949, 1953, 1958, 1960, 1969, 1973, 1980, 1981, 1990, 2001, 2008.

#27 Within 20 years of the creation of the Federal Reserve, the U.S. economy was plunged into the Great Depression.

#28 The Federal Reserve created the conditions that caused the stock market crash of 1929, and even Ben Bernanke admits that the response by the Fed to that crisis made the Great Depression even worse than it should have been.

#29 The “easy money” policies of former Fed Chairman Alan Greenspan set the stage for the great financial crisis of 2008.

#30 Without the Federal Reserve, the “subprime mortgage meltdown” would probably never have happened.

#31 If you can believe it, there have been 10 different economic recessions since 1950. The Federal Reserve created the “dotcom bubble”, the Federal Reserve created the “housing bubble” and now it has created the largest bond bubble in the history of the planet.

#32 According to an official government report, the Federal Reserve made 16.1 trillion dollars in secret loans to the big banks during the last financial crisis. The following is a list of loan recipients that was taken directly from page 131 of the report…

Citigroup – $2.513 trillion

Morgan Stanley – $2.041 trillion

Merrill Lynch – $1.949 trillion

Bank of America – $1.344 trillion

Barclays PLC – $868 billion

Bear Sterns – $853 billion

Goldman Sachs – $814 billion

Royal Bank of Scotland – $541 billion

JP Morgan Chase – $391 billion

Deutsche Bank – $354 billion

UBS – $287 billion

Credit Suisse – $262 billion

Lehman Brothers – $183 billion

Bank of Scotland – $181 billion

BNP Paribas – $175 billion

Wells Fargo – $159 billion

Dexia – $159 billion

Wachovia – $142 billion

Dresdner Bank – $135 billion

Societe Generale – $124 billion

“All Other Borrowers” – $2.639 trillion

#33 The Federal Reserve also paid those big banks $659.4 million in “fees” to help “administer” those secret loans.

#34 During the last financial crisis, big European banks were allowed to borrow an “unlimited” amount of money from the Federal Reserve at ultra-low interest rates.

#35 The “easy money” policies of Federal Reserve Chairman Ben Bernanke have created the largest financial bubble this nation has ever seen, and this has set the stage for the great financial crisis that we are rapidly approaching.

#36 Since late 2008, the size of the Federal Reserve balance sheet has grown from less than a trillion dollars to more than 4 trillion dollars. This is complete and utter insanity.

#37 During the quantitative easing era, the value of the financial securities that the Fed has accumulated is greater than the total amount of publicly held debt that the U.S. government accumulated from the presidency of George Washington through the end of the presidency of Bill Clinton.

#38 Overall, the Federal Reserve now holds more than 32 percent of all 10 year equivalents.

#39 Quantitative easing creates financial bubbles, and when quantitative easing ends those bubbles tend to deflate rapidly.

#40 Most of the new money created by quantitative easing has ended up in the hands of the very wealthy.

#41 According to a prominent Federal Reserve insider, quantitative easing has been one giant “subsidy” for Wall Street banks.

#42 As one CNBC article stated, we have seen absolutely rampant inflation in “stocks and bonds and art and Ferraris“.

#43 Donald Trump once made the following statement about quantitative easing: “People like me will benefit from this.”

#44 Most people have never heard about this, but a very interesting study conducted for the Bank of England shows that quantitative easing actually increases the gap between the wealthy and the poor.

#45 The gap between the top one percent and the rest of the country is now the greatest that it has been since the 1920s.

#46 The mainstream media has sold quantitative easing to the American public as an “economic stimulus program”, but the truth is that the percentage of Americans that have a job has actually gone down since quantitative easing first began.

#47 The Federal Reserve is supposed to be able to guide the nation toward “full employment”, but the reality of the matter is that an all-time record 102 million working age Americans do not have a job right now. That number has risen by about 27 million since the year 2000.

#48 For years, the projections of economic growth by the Federal Reserve have consistently overstated the strength of the U.S. economy. But every single time, the mainstream media continues to report that these numbers are “reliable” even though all they actually represent is wishful thinking.

#49 The Federal Reserve system fuels the growth of government, and the growth of government fuels the growth of the Federal Reserve system. Since 1970, federal spending has grown nearly 12 times as rapidly as median household income has.

#50 The Federal Reserve is supposed to look out for the health of all U.S. banks, but the truth is that they only seem to be concerned about the big ones. In 1985, there were more than 18,000 banks in the United States. Today, there are only 6,891 left.

#51 The six largest banks in the United States (JPMorgan Chase, Bank of America, Citigroup, Wells Fargo, Goldman Sachs and Morgan Stanley) have collectively gotten 37 percent larger over the past five years.

#52 The U.S. banking system has 14.4 trillion dollars in total assets. The six largest banks now account for 67 percent of those assets and all of the other banks account for only 33 percent of those assets.

#53 The five largest banks now account for 42 percent of all loans in the United States.

#54 We were told that the purpose of quantitative easing was to help “stimulate the economy”, but today the Federal Reserve is actually paying the big banks not to lend out 1.8 trillion dollars in “excess reserves” that they have parked at the Fed.

#55 The Federal Reserve has allowed an absolutely gigantic derivatives bubble to inflate which could destroy our financial system at any moment. Right now, four of the “too big to fail” banks each have total exposure to derivatives that is well in excess of 40 trillion dollars.

#56 The total exposure that Goldman Sachs has to derivatives contracts is more than 381 times greater than their total assets.

#57 Federal Reserve Chairman Ben Bernanke has a track record of failure that would make the Chicago Cubs look good.

#58 The secret November 1910 gathering at Jekyll Island, Georgia during which the plan for the Federal Reserve was hatched was attended by U.S. Senator Nelson W. Aldrich, Assistant Secretary of the Treasury Department A.P. Andrews and a whole host of representatives from the upper crust of the Wall Street banking establishment.

#59 The Federal Reserve was created by the big Wall Street banks and for the benefit of the big Wall Street banks.

#60 In 1913, Congress was promised that if the Federal Reserve Act was passed that it would eliminate the business cycle.

#61 There has never been a true comprehensive audit of the Federal Reserve since it was created back in 1913.

#62 The Federal Reserve system has been described as “the biggest Ponzi scheme in the history of the world“.

#63 The following comes directly from the Fed’s official mission statement: “To provide the nation with a safer, more flexible, and more stable monetary and financial system.” Without a doubt, the Federal Reserve has failed in those tasks dramatically.

#64 The Fed decides what the target rate of inflation should be, what the target rate of unemployment should be and what the size of the money supply is going to be. This is quite similar to the “central planning” that goes on in communist nations, but very few people in our government seem upset by this.

#65 A couple of years ago, Federal Reserve officials walked into one bank in Oklahoma and demanded that they take down all the Bible verses and all the Christmas buttons that the bank had been displaying.

#66 The Federal Reserve has taken some other very frightening steps in recent years. For example, back in 2011 the Federal Reserve announced plans to identify “key bloggers” and to monitor “billions of conversations” about the Fed on Facebook, Twitter, forums and blogs. Someone at the Fed will almost certainly end up reading this article.

#67 Thanks to this endless debt spiral that we are trapped in, a massive amount of money is transferred out of our pockets and into the pockets of the ultra-wealthy each year. Incredibly, the U.S. government spent more than 415 billion dollars just on interest on the national debt in 2013.

#68 In January 2000, the average rate of interest on the government’s marketable debt was 6.620 percent. If we got back to that level today, we would be paying more than a trillion dollars a year just in interest on the national debt and it would collapse our entire financial system.

#69 The American people are being killed by compound interest but most of them don’t even understand what it is. Albert Einstein once made the following statement about compound interest…

“Compound interest is the eighth wonder of the world. He who understands it, earns it … he who doesn’t … pays it.”

#70 Most Americans have absolutely no idea where money comes from. The truth is that the Federal Reserve just creates it out of thin air. The following is how I have previously described how money is normally created by the Fed in our system…

When the U.S. government decides that it wants to spend another billion dollars that it does not have, it does not print up a billion dollars.

Rather, the U.S. government creates a bunch of U.S. Treasury bonds (debt) and takes them over to the Federal Reserve.

The Federal Reserve creates a billion dollars out of thin air and exchanges them for the U.S. Treasury bonds.

#71 What does the Federal Reserve do with those U.S. Treasury bonds? They end up getting auctioned off to the highest bidder. But this entire process actually creates more debt than it does money…

The U.S. Treasury bonds that the Federal Reserve receives in exchange for the money it has created out of nothing are auctioned off through the Federal Reserve system.

But wait.

There is a problem.

Because the U.S. government must pay interest on the Treasury bonds, the amount of debt that has been created by this transaction is greater than the amount of money that has been created.

So where will the U.S. government get the money to pay that debt?

Well, the theory is that we can get money to circulate through the economy really, really fast and tax it at a high enough rate that the government will be able to collect enough taxes to pay the debt.

But that never actually happens, does it?

And the creators of the Federal Reserve understood this as well. They understood that the U.S. government would not have enough money to both run the government and service the national debt. They knew that the U.S. government would have to keep borrowing even more money in an attempt to keep up with the game.

#72 Of course the U.S. government could actually create money and spend it directly into the economy without the Federal Reserve being involved at all. But then we wouldn’t be 17 trillion dollars in debt and that wouldn’t serve the interests of the bankers at all.

#73 The following is what Thomas Edison once had to say about our absolutely insane debt-based financial system…

That is to say, under the old way any time we wish to add to the national wealth we are compelled to add to the national debt.

Now, that is what Henry Ford wants to prevent. He thinks it is stupid, and so do I, that for the loan of $30,000,000 of their own money the people of the United States should be compelled to pay $66,000,000 — that is what it amounts to, with interest. People who will not turn a shovelful of dirt nor contribute a pound of material will collect more money from the United States than will the people who supply the material and do the work. That is the terrible thing about interest. In all our great bond issues the interest is always greater than the principal. All of the great public works cost more than twice the actual cost, on that account. Under the present system of doing business we simply add 120 to 150 per cent, to the stated cost.

But here is the point: If our nation can issue a dollar bond, it can issue a dollar bill. The element that makes the bond good makes the bill good.

#74 The United States now has the largest national debt in the history of the world, and we are stealing roughly 100 million dollars from our children and our grandchildren every single hour of every single day in a desperate attempt to keep the debt spiral going.

#75 Thomas Jefferson once stated that if he could add just one more amendment to the U.S. Constitution it would be a ban on all government borrowing…

I wish it were possible to obtain a single amendment to our Constitution. I would be willing to depend on that alone for the reduction of the administration of our government to the genuine principles of its Constitution; I mean an additional article, taking from the federal government the power of borrowing.

#76 At this moment, the U.S. national debt is sitting at $18,141,409,083,212.36. If we had followed the advice of Thomas Jefferson, it would be sitting at zero.

#77 When the Federal Reserve was first established, the U.S. national debt was sitting at about 2.9 billion dollars. On average, we have been adding more than that to the national debt every single day since Obama has been in the White House.

#78 We are on pace to accumulate more new debt during the 8 years of the Obama administration than we did under all of the other presidents in all of U.S. history combined.

#79 If all of the new debt that has been accumulated since John Boehner became Speaker of the House had been given directly to the American people instead, every household in America would have been able to buy a new truck.

#80 Between 2008 and 2012, U.S. government debt grew by 60.7 percent, but U.S. GDP only grew by a total of about 8.5 percent during that entire time period.

#81 Since 2007, the U.S. debt to GDP ratio has increased from 66.6 percent to 102.98 percent.

#82 According to the U.S. Treasury, foreigners hold approximately 5.6 trillion dollars of our debt.

#83 The amount of U.S. government debt held by foreigners is about 5 times larger than it was just a decade ago.

#84 As I have written about previously, if the U.S. national debt was reduced to a stack of one dollar bills it would circle the earth at the equator 45 times.

#85 If Bill Gates gave every single penny of his entire fortune to the U.S. government, it would only cover the U.S. budget deficit for 15 days.

#86 Sometimes we forget just how much money a trillion dollars is. If you were alive when Jesus Christ was born and you spent one million dollars every single day since that point, you still would not have spent one trillion dollars by now.

#87 If right this moment you went out and started spending one dollar every single second, it would take you more than 31,000 years to spend one trillion dollars.

#88 In addition to all of our debt, the U.S. government has also accumulated more than 200 trillion dollars in unfunded liabilities. So where in the world will all of that money come from?

#89 The greatest damage that quantitative easing has been causing to our economy is the fact that it is destroying worldwide faith in the U.S. dollar and in U.S. debt. If the rest of the world stops using our dollars and stops buying our debt, we are going to be in a massive amount of trouble.

#90 Over the past several years, the Federal Reserve has been monetizing a staggering amount of U.S. government debt even though Ben Bernanke once promised that he would never do this.

#91 China recently announced that they are going to quit stockpiling more U.S. dollars. If the Federal Reserve was not recklessly printing money, this would probably not have happened.

#92 Most Americans have no idea that one of our most famous presidents was absolutely obsessed with getting rid of central banking in the United States. The following is a February 1834 quote by President Andrew Jackson about the evils of central banking…

I too have been a close observer of the doings of the Bank of the United States. I have had men watching you for a long time, and am convinced that you have used the funds of the bank to speculate in the breadstuffs of the country. When you won, you divided the profits amongst you, and when you lost, you charged it to the Bank. You tell me that if I take the deposits from the Bank and annul its charter I shall ruin ten thousand families. That may be true, gentlemen, but that is your sin! Should I let you go on, you will ruin fifty thousand families, and that would be my sin! You are a den of vipers and thieves. I have determined to rout you out and, by the Eternal, (bringing his fist down on the table) I will rout you out.

#93 There are plenty of possible alternative financial systems, but at this point all 187 nations that belong to the IMF have a central bank. Are we supposed to believe that this is just some sort of a bizarre coincidence?

#94 The capstone of the global central banking system is an organization known as the Bank for International Settlements. The following is how I described this organization in a previous article…

An immensely powerful international organization that most people have never even heard of secretly controls the money supply of the entire globe. It is called the Bank for International Settlements, and it is the central bank of central banks. It is located in Basel, Switzerland, but it also has branches in Hong Kong and Mexico City. It is essentially an unelected, unaccountable central bank of the world that has complete immunity from taxation and from national laws. Even Wikipedia admits that “it is not accountable to any single national government.” The Bank for International Settlements was used to launder money for the Nazis during World War II, but these days the main purpose of the BIS is to guide and direct the centrally-planned global financial system. Today, 58 global central banks belong to the BIS, and it has far more power over how the U.S. economy (or any other economy for that matter) will perform over the course of the next year than any politician does. Every two months, the central bankers of the world gather in Basel for another “Global Economy Meeting”. During those meetings, decisions are made which affect every man, woman and child on the planet, and yet none of us have any say in what goes on. The Bank for International Settlements is an organization that was founded by the global elite and it operates for the benefit of the global elite, and it is intended to be one of the key cornerstones of the emerging one world economic system.

#95 The borrower is the servant of the lender, and the Federal Reserve has turned all of us into debt slaves.

#96 Debt is a form of social control, and the global elite use all of this debt to dominate all the rest of us. 40 years ago, the total amount of debt in our system (all government debt, all business debt, all consumer debt, etc.) was sitting at about 3 trillion dollars. Today, the grand total is approaching 60 trillion dollars.

#97 Unless something dramatic is done, our children and our grandchildren will be debt slaves for their entire lives as they service our debts and pay for our mistakes.

#98 Now that you know this information, you are responsible for doing something about it.

#99 Congress has the power to shut down the Federal Reserve any time that it would like. But right now most of our politicians fully endorse the current system, and nothing is ever going to happen until the American people start demanding change.

#100 The design of the Federal Reserve system was flawed from the very beginning. If something is not done very rapidly, it is inevitable that our entire financial system is going to suffer an absolutely nightmarish collapse.

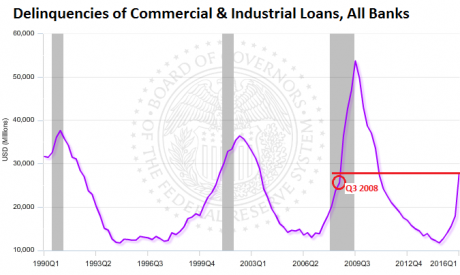

You are about to see more very clear evidence that a new economic crisis has already begun. During economic recoveries, business debt delinquencies generally fall, and during times of economic recession business debt delinquencies generally rise. In fact, you will see below that business debt delinquencies shot up dramatically just prior to the last two recessions, and the exact same thing is happening again right now. In 2008, business debt delinquencies increased at a very frightening pace just before Lehman Brothers collapsed, and this was a very clear sign that big trouble was ahead. Unfortunately for us, in 2016 business debt delinquencies have already shot up above the level they were sitting at just before the collapse of Lehman Brothers, and every time debt delinquencies have ever gotten this high the U.S. economy has always fallen into recession.

You are about to see more very clear evidence that a new economic crisis has already begun. During economic recoveries, business debt delinquencies generally fall, and during times of economic recession business debt delinquencies generally rise. In fact, you will see below that business debt delinquencies shot up dramatically just prior to the last two recessions, and the exact same thing is happening again right now. In 2008, business debt delinquencies increased at a very frightening pace just before Lehman Brothers collapsed, and this was a very clear sign that big trouble was ahead. Unfortunately for us, in 2016 business debt delinquencies have already shot up above the level they were sitting at just before the collapse of Lehman Brothers, and every time debt delinquencies have ever gotten this high the U.S. economy has always fallen into recession.