How can anyone not see that the U.S. economy is collapsing all around us? It just astounds me when people try to tell me that “everything is just fine” and that “things are getting better” in America. Are there people out there that are really that blind? If you want to see the economic collapse, just open up your eyes and look around you. By almost every economic and financial measure, the U.S. economy has been steadily declining for many years. But most Americans are so tied into “the matrix” that they can only understand the cheerful propaganda that is endlessly being spoon-fed to them by the mainstream media. As I have said so many times, the economic collapse is not a single event. The economic collapse has been happening, it is is happening right now, and it will continue to happen. Yes, there will be times when our decline will be punctuated by moments of great crisis, but that will be the exception rather than the rule. A lot of people that write about “the economic collapse” hype it up as if it will be some huge “event” that will happen very rapidly and then once it is all over we will rebuild. Unfortunately, that is not how the real world works. We are living in the greatest debt bubble in the history of the world, and once it completely bursts there will be no going back to how things were before. Right now, we are living in a “credit card economy”. As long as we can keep borrowing more money, most people think that things are just fine. But anyone that has lived on credit cards knows that eventually there comes a point when the game is over, and we are rapidly approaching that point as a nation.

How can anyone not see that the U.S. economy is collapsing all around us? It just astounds me when people try to tell me that “everything is just fine” and that “things are getting better” in America. Are there people out there that are really that blind? If you want to see the economic collapse, just open up your eyes and look around you. By almost every economic and financial measure, the U.S. economy has been steadily declining for many years. But most Americans are so tied into “the matrix” that they can only understand the cheerful propaganda that is endlessly being spoon-fed to them by the mainstream media. As I have said so many times, the economic collapse is not a single event. The economic collapse has been happening, it is is happening right now, and it will continue to happen. Yes, there will be times when our decline will be punctuated by moments of great crisis, but that will be the exception rather than the rule. A lot of people that write about “the economic collapse” hype it up as if it will be some huge “event” that will happen very rapidly and then once it is all over we will rebuild. Unfortunately, that is not how the real world works. We are living in the greatest debt bubble in the history of the world, and once it completely bursts there will be no going back to how things were before. Right now, we are living in a “credit card economy”. As long as we can keep borrowing more money, most people think that things are just fine. But anyone that has lived on credit cards knows that eventually there comes a point when the game is over, and we are rapidly approaching that point as a nation.

Have you ever been there? Have you ever desperately hoped that you could just get one more credit card or one more loan so that you could keep things going?

At first, living on credit can be a lot of fun. You can live a much higher standard of living than you otherwise would be able to.

But inevitably a day of reckoning comes.

If the federal government and the American people were forced at this moment to live within their means, the U.S. economy would immediately plunge into a depression.

That is a 100% rock solid guarantee.

But our politicians and the mainstream media continue to perpetuate the fiction that we can live in this credit card economic fantasy land indefinitely.

And most Americans could not care less about the future. As long as “things are good” today, they don’t really think much about what the future will hold.

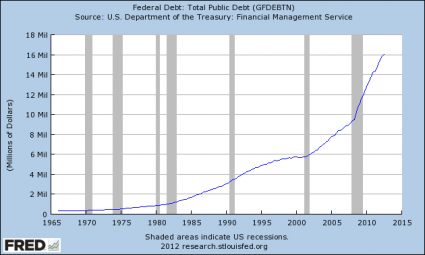

As a result of our very foolish short-term thinking, we have now run up a national debt of 16.4 trillion dollars. It is the largest debt in the history of the world, and it has gotten more than 23 times larger since Jimmy Carter first entered the White House.

The chart that you see below is a recipe for national financial suicide…

Of course things have accelerated over the past four years. Since Barack Obama entered the White House, the U.S. government has run a budget deficit of well over a trillion dollars every single year, and we have stolen more than 100 million dollars from our children and our grandchildren every single hour of every single day.

It is the biggest theft of all time. What we are doing to our children and our grandchildren is beyond criminal.

And now our debt is at a level that most economists would consider terminal. When Barack Obama first entered the White House, the U.S. debt to GDP ratio was under 70 percent. Today, it is up to 103 percent.

We are officially in “the danger zone”.

If things really were “getting better” in America, we would not need to borrow so much money.

Our politicians are stealing from the future in order to make the present look better. During Obama’s first term, the federal government accumulated more debt than it did under the first 42 U.S presidents combined.

That is utter insanity!

If you started paying off just the new debt that the U.S. has accumulated during the Obama administration at the rate of one dollar per second, it would take more than 184,000 years to pay it off.

So what is the solution?

Get ready to laugh.

The most prominent economic journalist in the entire country, Paul Krugman of the New York Times, recently suggested the following in an article that he wrote entitled “Kick That Can“…

Realistically, we’re not going to resolve our long-run fiscal issues any time soon, which is O.K. — not ideal, but nothing terrible will happen if we don’t fix everything this year. Meanwhile, we face the imminent threat of severe economic damage from short-term spending cuts.

So we should avoid that damage by kicking the can down the road. It’s the responsible thing to do.

You mean that we might actually do damage to the debt-fueled economic fantasy world that we are living in if we stopped stealing so much money from future generations?

Oh the humanity!

It is horrifying to think that all that one of the “top economic minds” in America can come up with is to “kick the can” down the road some more.

Unfortunately, neither Paul Krugman nor most of the American people understand that our financial system is actually designed to create government debt.

The bankers that helped create the Federal Reserve intended to permanently enslave the U.S. government to a perpetually expanding spiral of debt, and their plans worked.

At this point, the U.S. national debt is more than 5000 times larger than it was when the Federal Reserve was first created.

So why don’t the American people understand what the Federal Reserve system is doing to us?

It is because most of them are still plugged into the matrix. A Zero Hedge article that I came across today put it beautifully…

US society in a nutshell: Chris Dorner has been around for a week and has 222 million results on Google; the Federal Reserve has been around for one hundred years and has 187 million results.

If nothing is done about our exploding debt, it is only a matter of time before we reach financial oblivion.

According to Boston University economist Laurence Kotlikoff, the U.S. government is facing a “present value difference between projected future spending and revenue” of 222 trillion dollars in the years ahead.

So how in the world are we going to come up with an extra 222 trillion dollars?

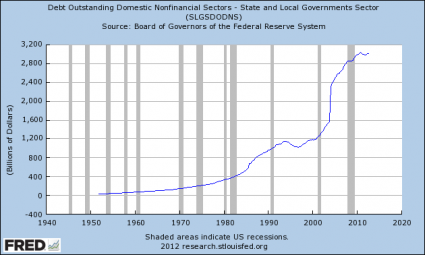

But it is not just the U.S. government that is drowning in debt.

Just check out this chart which shows the astounding growth of state and local government debt in recent years…

All over the United States there are state and local governments that are on the verge of bankruptcy. Just check out what is going on in Detroit. The only way that most of our state and local governments can keep going at this point is to also “kick the can” down the road some more.

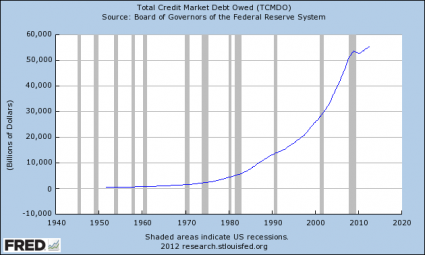

And of course most of the rest of us are drowning in debt as well.

40 years ago, the total amount of debt in the U.S. economic system (government + business + consumer) was less than 2 trillion dollars.

Today, the total amount of debt in the U.S. economic system has grown to more than 55 trillion dollars.

Can anyone say bubble?

The good news is that U.S. GDP is now more than 12 times larger than it was 40 years ago.

The bad news is that the total amount of debt in our financial system is now more than 30 times larger than it was 40 years ago…

At the same time that we are going into so much debt, our ability to produce wealth continues to decline.

According to the World Bank, U.S. GDP accounted for 31.8 percent of all global economic activity in 2001. That number dropped to 21.6 percent in 2011. That is not just a decline – that is a nightmarish freefall. Just check out the chart in this article.

We are becoming less competitive as a nation with each passing year. In fact, the U.S. has fallen in the global economic competitiveness rankings compiled by the World Economic Forum for four years in a row.

Most Americans don’t understand this, but the United States buys far more from the rest of the world than they buy from us each year. In 2012, we had a trade deficit of more than 500 billion dollars with the rest of the world.

That means that more than 500 billion dollars that could have gone to U.S. workers and U.S. businesses went out of the country instead.

So how does our country survive if hundreds of billions of dollars more is flowing out of the country than is flowing into it?

Well, to make up the shortfall we go to the countries that we sent our money to and we beg them to lend it back to us. If that doesn’t work, we just print and borrow even more money.

Overall, the United States has run a trade deficit of more than 8 trillion dollars with the rest of the world since 1975.

That is 8 trillion dollars that could have saved U.S. businesses, paid the salaries of U.S. workers and that would have helped fund government.

But instead, our foolish policies have greatly enriched China and the oil barons of the Middle East.

Sadly, politicians from both political parties continue to boldly support the one world economic agenda of the global elite.

Just consider how destructive many of these “free trade” deals have been to our economy…

When NAFTA was pushed through Congress in 1993, the United States had a trade surplus with Mexico of 1.6 billion dollars.

By 2010, we had a trade deficit with Mexico of 61.6 billion dollars.

Back in 1985, our trade deficit with China was approximately 6 million dollars (million with a little “m”) for the entire year.

In 2012, our trade deficit with China was 315 billion dollars. That was the largest trade deficit that one nation has had with another nation in the history of the world.

In particular, our trade with China is extremely unbalanced. Today, U.S. consumers spend approximately 4 dollars on goods and services from China for every one dollar that Chinese consumers spend on goods and services from the United States.

But isn’t getting cheap stuff from China good?

No, because it costs us good paying jobs.

According to the Economic Policy Institute, the United States is losing half a million jobs to China every single year.

Overall, more than 56,000 manufacturing facilities in the United States have been shut down since 2001. During 2010, manufacturing facilities in the United States were shutting down at a rate of 23 per day. How can anyone say that “things are getting better” when our economic infrastructure is being absolutely gutted?

The truth is that there are never going to be enough jobs in America ever again, because millions of our jobs are being sent overseas and millions of our jobs are being lost to technology.

You won’t hear this on the news, but the percentage of the civilian labor force in the United States that is employed has been steadily declining every single year since 2006.

Younger workers have been hit particularly hard. In 2007, the unemployment rate for the 20 to 29 age bracket was about 6.5 percent. Today, the unemployment rate for that same age group is about 13 percent.

If you are under the age of 30 and you aren’t living with your parents, there is a really good chance that you are living in poverty. If you can believe it, U.S. families that have a head of household that is under the age of 30 have a poverty rate of 37 percent.

Our economy has been steadily bleeding huge numbers of middle class jobs, and many of those jobs have been replaced by low paying jobs in recent years.

According to one study, 60 percent of the jobs lost during the last recession were mid-wage jobs, but 58 percent of the jobs created since then have been low wage jobs.

And at this point, an astounding 53 percent of all American workers make less than $30,000 a year.

Oh, but “things are getting better”, right?

Maybe if you live on Wall Street or if you are an employee of the federal government.

But for most families this economic decline has been a total nightmare. Median household income in America has fallen for four consecutive years. Overall, it has declined by over $4000 during that time span.

Sometimes people forget how good things were about a decade ago. About three times as many new homes were sold in the United States in 2005 as were sold in 2012.

But we like to live in denial.

In fact, a lot of families are trying to keep up their standards of living by going into tremendous amounts of debt.

Back in 1983, the bottom 95 percent of all income earners in the United States had 62 cents of debt for every dollar that they earned. By 2007, that figure had soared to $1.48.

Fake it until you make it, right?

But how much debt can our system possibly handle?

Total home mortgage debt in the United States is now about 5 times larger than it was just 20 years ago.

Total credit card debt in the United States is now more than 8 times larger than it was just 30 years ago.

We are a nation that is completely addicted to debt, but as the financial crisis of 2008 demonstrated, all of that debt can have horrific consequences.

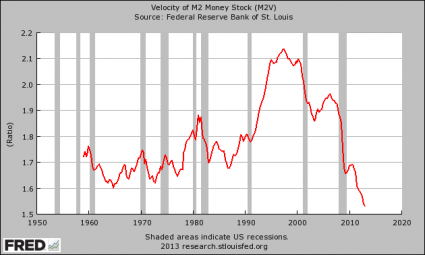

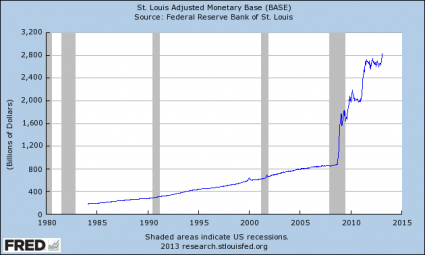

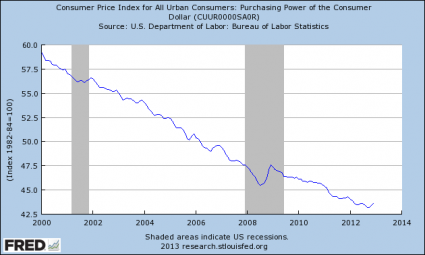

As the economy has slowed in recent years, the Federal Reserve has decided that “the solution” is to recklessly print money in an attempt to get the debt spiral cranked up again.

Have they gone overboard? You be the judge…

And of course this won’t have any affect on the value of the money that you have been saving up all these years right?

Wrong.

Every single dollar that you own is continually losing value…

Overall, the value of the U.S. dollar has declined by more than 96 percent since the Federal Reserve was first created.

As the cost of living continues to go up and wages continue to go down, millions of American families have fallen out of the middle class and into poverty.

If you can believe it, the number of Americans on food stamps has grown from about 17 million in the year 2000 to more than 47 million today.

But “things are getting better”, right?

Incredibly, more than a million public school students in the United States are homeless. This is the first time that has ever happened in our history.

But “things are getting better”, right?

There are now 20.2 million Americans that spend more than half of their incomes on housing. That represents a 46 percent increase from 2001.

But “things are getting better”, right?

In 1999, 64.1 percent of all Americans were covered by employment-based health insurance. Today, only 55.1 percent are covered by employment-based health insurance.

But “things are getting better”, right?

Today, more Americans than ever have found themselves forced to turn to the federal government for help.

Overall, the federal government runs nearly 80 different “means-tested welfare programs”, and at this point more than 100 million Americans are enrolled in at least one of them.

According to the U.S. Census Bureau, 49 percent of all Americans live in a home that receives direct monetary benefits from the federal government. Back in 1983, less than a third of all Americans lived in a home that received direct monetary benefits from the federal government.

So is it a good sign or a bad sign that the percentage of Americans that are financially dependent on the federal government is at an all-time high?

And in future years the number of Americans that are receiving benefits from the federal government is projected to absolutely skyrocket.

Back in 1965, only one out of every 50 Americans was on Medicaid. Today, one out of every 6 Americans is on Medicaid, and things are about to get a whole lot worse. It is being projected that Obamacare will add 16 million more Americans to the Medicaid rolls.

If you take a look at Medicare, things are very more sobering.

As I wrote recently, it is being projected that the number of Americans on Medicare will grow from 50.7 million in 2012 to 73.2 million in 2025.

At this point, Medicare is facing unfunded liabilities of more than 38 trillion dollars over the next 75 years. That comes to approximately $328,404 for every single household in the United States.

Are you ready to contribute your share?

Social Security is a complete and total nightmare as well.

Right now, there are approximately 56 million Americans collecting Social Security benefits.

By 2035, that number is projected to soar to an astounding 91 million.

Overall, the Social Security system is facing a 134 trillion dollar shortfall over the next 75 years.

Oh, but don’t worry because “things are getting better”, right?

I honestly do not know how anyone can look at the numbers above and come to the conclusion that the economy is in good shape.

We have accumulated the largest mountain of debt in the history of the world, our economic infrastructure is being gutted, we are bleeding good jobs, government dependence is at an all-time high and we are getting poorer as a nation with each passing day.

But other than that, everything is rainbows and lollipops, right?

If you want to see the economic collapse, just open up your eyes.

And if dramatic changes are not made quickly, things are going to get much, much worse from here.

Please share this article with as many people as possible. Time is quickly running out and there are a whole lot of people out there that we need to wake up while we still can.

Is the global economic downturn going to accelerate as we roll into the second half of this year? There is turmoil in the Middle East, we are seeing things happen in the bond markets that we have not seen happen in more than 30 years, and much of Europe has already plunged into a full-blown economic depression. Sadly, most Americans will never understand what is happening until financial disaster strikes them personally. As long as they can go to work during the day and eat frozen pizza and watch reality television at night, most of them will consider everything to be just fine. Unfortunately, the truth is that everything is not fine. The world is becoming increasingly unstable, we are living in the terminal phase of the greatest debt bubble in the history of the planet and the global financial system is even more vulnerable than it was back in 2008. Unfortunately, most people seem to only have a 48 hour attention span at best these days. They don’t have the patience to watch long-term trends develop. And the coming economic collapse is not going to happen all at once. Rather, it is like watching a very, very slow-motion train wreck happen. The coming economic nightmare is going to unfold over a number of years. Yes, there will be moments of great panic, but mostly it will be a steady decline into economic oblivion. And there are a lot of indications that the second half of this year is not going to be as good as the first half was. The following are 19 reasons to be deeply concerned about the global economy as we head into the second half of 2013…

Is the global economic downturn going to accelerate as we roll into the second half of this year? There is turmoil in the Middle East, we are seeing things happen in the bond markets that we have not seen happen in more than 30 years, and much of Europe has already plunged into a full-blown economic depression. Sadly, most Americans will never understand what is happening until financial disaster strikes them personally. As long as they can go to work during the day and eat frozen pizza and watch reality television at night, most of them will consider everything to be just fine. Unfortunately, the truth is that everything is not fine. The world is becoming increasingly unstable, we are living in the terminal phase of the greatest debt bubble in the history of the planet and the global financial system is even more vulnerable than it was back in 2008. Unfortunately, most people seem to only have a 48 hour attention span at best these days. They don’t have the patience to watch long-term trends develop. And the coming economic collapse is not going to happen all at once. Rather, it is like watching a very, very slow-motion train wreck happen. The coming economic nightmare is going to unfold over a number of years. Yes, there will be moments of great panic, but mostly it will be a steady decline into economic oblivion. And there are a lot of indications that the second half of this year is not going to be as good as the first half was. The following are 19 reasons to be deeply concerned about the global economy as we head into the second half of 2013…