Just like “America’s time-share king”, America just keeps on making the same mistakes over and over again. Prior to the financial collapse of 2008, time-share mogul David Siegel and his wife Jackie began construction on their “dream home” near Disney World in Orlando, Florida. This dream home would be approximately 90,000 square feet in size, would be worth $100 million when completed, and would be named “Versailles” after the French palace that inspired it. In fact, you may remember David and Jackie from an excellent 2012 documentary entitled “The Queen of Versailles”. That film documented how the Siegels almost lost everything after the financial collapse of 2008 devastated the U.S. economy because they were overleveraged and drowning in debt. But since that time, David’s time-share company has bounced back, and the Siegels now plan to finally finish construction on their dream home and make it bigger and better than ever before. But before you pass judgment on the Siegels, it is important to keep in mind that we are behaving exactly the same way as a nation. Instead of addressing our fundamental problems after the last financial crisis, we have just continued to make the exact same mistakes that we made before. And ultimately, things are going to end very, very badly for us.

Just like “America’s time-share king”, America just keeps on making the same mistakes over and over again. Prior to the financial collapse of 2008, time-share mogul David Siegel and his wife Jackie began construction on their “dream home” near Disney World in Orlando, Florida. This dream home would be approximately 90,000 square feet in size, would be worth $100 million when completed, and would be named “Versailles” after the French palace that inspired it. In fact, you may remember David and Jackie from an excellent 2012 documentary entitled “The Queen of Versailles”. That film documented how the Siegels almost lost everything after the financial collapse of 2008 devastated the U.S. economy because they were overleveraged and drowning in debt. But since that time, David’s time-share company has bounced back, and the Siegels now plan to finally finish construction on their dream home and make it bigger and better than ever before. But before you pass judgment on the Siegels, it is important to keep in mind that we are behaving exactly the same way as a nation. Instead of addressing our fundamental problems after the last financial crisis, we have just continued to make the exact same mistakes that we made before. And ultimately, things are going to end very, very badly for us.

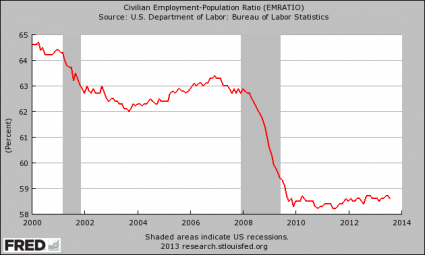

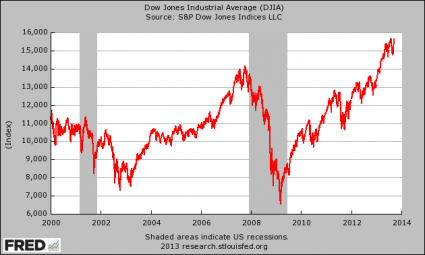

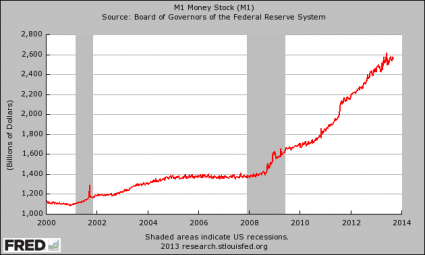

As Americans, we like to think that we are somehow entitled to the biggest and best of everything. We have been trained to believe that we are the wealthiest and most prosperous nation on the entire planet and that it will always be that way. This generation was handed the keys to the greatest economic machine in world history, but instead of treating it with great care, we have wrecked it. Our economic infrastructure is being systematically dismantled, Wall Street has been transformed into the biggest casino in the history of the planet, we have piled up a mountain of debt unlike anything the world has ever seen, and the reckless Federal Reserve is turning our currency into Monopoly money. All of our decisions have been designed to make things better for ourselves in the short-term without any consideration about what we were doing to the future of this country.

That is why “Versailles” is such a perfect metaphor for America. The Siegels always had to have the biggest and the best of everything, and they almost lost it all when the financial markets crashed…

David Siegel (“They call me the time-share king”) and his wife, Jackie Siegel — titular star of the 2012 documentary “The Queen of Versailles” — began building their dream home near Disney World about a decade ago. Soon it became evident that the sheer size of the mansion was almost unprecedented in America; it’s thought that only Biltmore House and Oheka Castle are bigger and still standing, and both of those are now run as tourist attractions, not true single-family homes.

But when the bottom fell out of the financial markets in 2008, their fortunes were upended too. By the time the documentary ended, their dream home had gone into default and they’d put it on the market. The listing asked for $100 million finished — “based on the royal palace of Louix XIV of the 17th century or to the buyer’s specifications — or $75 million “as is with all exterior finishings in crates in the 20-car garage on site.”

But just like the U.S. economy, the Siegels have seemingly recovered, at least for the moment.

Thanks to a rebound in the time-share business, the Siegels plan to finally complete their dream home and make it bigger and better than ever…

The unfinished home sits on 10 acres of lakefront property and when completed will feature 11 kitchens, 30 bathrooms, 20-car garage, two-lane bowling alley, indoor rollerskating rink, three indoor pools, two outdoor pools, video arcade, ballroom, two-story movie theater modeled off the Paris Opera House, fitness center with 10,000-square-foot spa, yoga studios, 20,000-bottle wine cellar and an exotic fish aquarium.

Two tennis courts, a baseball diamond and formal garden will be included on the grounds.

The couple admitted that some of their plans for the house – such as children’s playrooms – will have to be modified now that their kids are older.

However, they are determined to see the project through.

‘I’m not at the ending to my story yet, but so far, it’s a happy ending, and I’m really looking forward to starting the next chapter of my life and moving into my palace, finishing it and throwing lots of parties – anxious for the world to see it,’ Mrs Siegel said.

It is easy to point fingers at the Siegels, but the truth is that they are just behaving like we have been behaving as an entire nation.

When our financial bubbles burst the last time, our leaders did not really do anything to address our fundamental economic problems. Instead, they were bound and determined to reinflate those bubbles and make them even larger than before.

Now we stand at the precipice of the greatest financial crisis in our history, and we only have ourselves to blame.

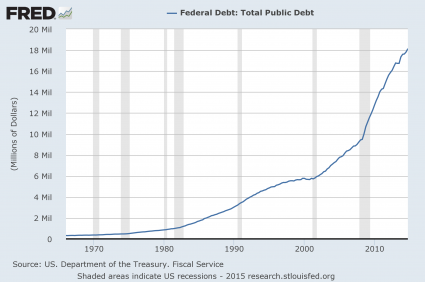

Just consider what has happened to our national debt. Just prior to the last recession, it was sitting at about 9 trillion dollars. Today, it has just crossed the 18 trillion dollar mark…

You may not think that you are to blame for this, but most of the people that will read this article voted for politicians that fully supported all of this borrowing and spending. And yes, that includes most Democrats and most Republicans.

We have stolen trillions of dollars from future generations of Americans in a desperate attempt to prop up our failing standard of living in the present. What we have done is a horrific crime, and if we lived in a just society a whole lot of people would be going to prison over this.

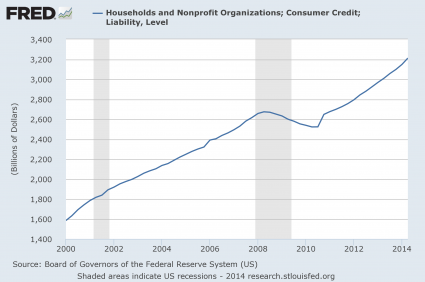

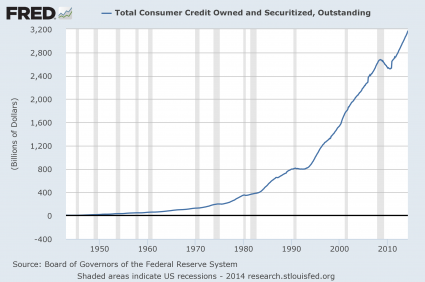

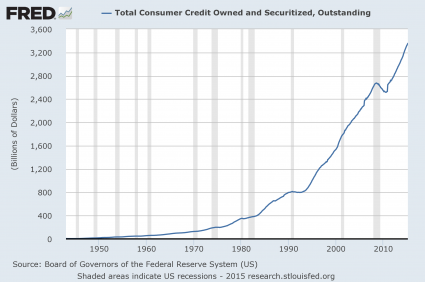

A similar pattern emerges when we look at the spending habits of ordinary Americans. This next chart shows one measure of consumer credit in America. During the last recession, we actually had a brief period of deleveraging (which was good), but now we are back on the exact same trajectory as before…

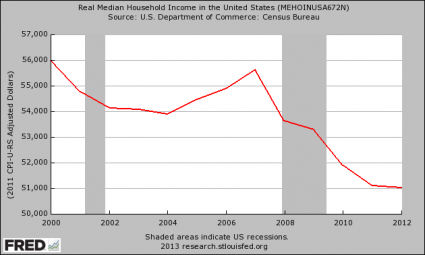

Even though we had a higher standard of living than all previous generations of Americans, that was never good enough for us. We always had to have more, and we have borrowed and spent ourselves into oblivion.

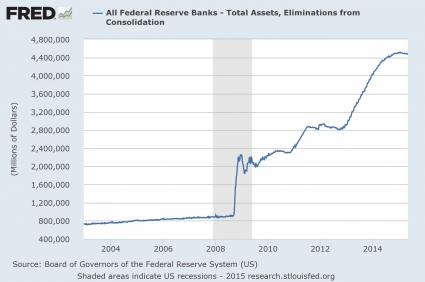

We have also shown absolutely no respect for our currency. Having the primary reserve currency of the world has been an incredible advantage for the U.S. economy, but we are squandering that privilege. Like I said at the top of the article, the Federal Reserve has been treating the U.S. dollar like Monopoly money in recent years in an attempt to prop up the financial system. Just look at what “quantitative easing” has done to the Fed balance sheet since the last recession…

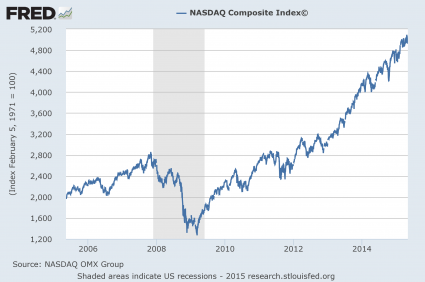

Most of the new money that the Fed has created has been funneled into the financial markets. This has created some financial bubbles which are absolutely insane. For example, just look at how the NASDAQ has performed since the last financial crisis…

These Fed-created bubbles are inevitably going to implode, because they have no relation to economic reality whatsoever. And when they implode, millions of Americans are going to be financially wiped out.

Just like David and Jackie Siegel, we simply can’t help ourselves. We just keep on making the same old mistakes.

And in the end, we will all pay a great, great price for our utter foolishness.