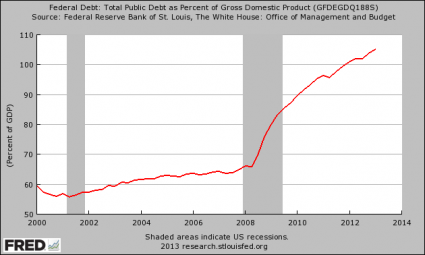

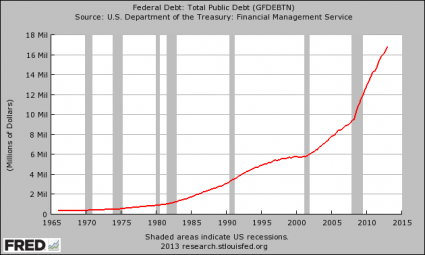

Will rapidly rising interest rates rip through the U.S. financial system like a giant lawnmower blade? Yes, the U.S. economy survived much higher interest rates in the past, but at that time there were not hundreds of trillions of dollars worth of interest rate derivatives hanging over our financial system like a Sword of Damocles. This is something that I have been talking about for quite some time, and now a Mexican billionaire has come forward with a similar warning. Hugo Salinas Price was the founder of the Elektra retail chain down in Mexico, and he is extremely concerned that rising interest rates could burst the derivatives bubble and cause “massive bankruptcies around the globe”. Of course there are a whole lot of people out there that would be quite glad to see the “too big to fail” banks go bankrupt, but the truth is that if they go down our entire economy will go down with them. Our situation is similar to a patient with a very advanced stage of cancer. You can try to kill the cancer with drugs, but you will almost certainly kill the patient at the same time. Well, that is essentially what our relationship with the big banks is like. Our entire economic system is based on credit, and just like we saw back in 2008, if the big banks start failing credit freezes up and suddenly nobody can get any money for anything. When the next great credit crunch comes, every important number in our economy will rapidly start getting much worse.

Will rapidly rising interest rates rip through the U.S. financial system like a giant lawnmower blade? Yes, the U.S. economy survived much higher interest rates in the past, but at that time there were not hundreds of trillions of dollars worth of interest rate derivatives hanging over our financial system like a Sword of Damocles. This is something that I have been talking about for quite some time, and now a Mexican billionaire has come forward with a similar warning. Hugo Salinas Price was the founder of the Elektra retail chain down in Mexico, and he is extremely concerned that rising interest rates could burst the derivatives bubble and cause “massive bankruptcies around the globe”. Of course there are a whole lot of people out there that would be quite glad to see the “too big to fail” banks go bankrupt, but the truth is that if they go down our entire economy will go down with them. Our situation is similar to a patient with a very advanced stage of cancer. You can try to kill the cancer with drugs, but you will almost certainly kill the patient at the same time. Well, that is essentially what our relationship with the big banks is like. Our entire economic system is based on credit, and just like we saw back in 2008, if the big banks start failing credit freezes up and suddenly nobody can get any money for anything. When the next great credit crunch comes, every important number in our economy will rapidly start getting much worse.

The big banks are going to play a starring role in the next financial crash just like they did in the last one. Only this next crash may be quite a bit worse. Just check out what billionaire Hugo Salinas Price told King World News recently…

I think we are going to see a series of bankruptcies. I think the rise in interest rates is the fatal sign which is going to ignite a derivatives crisis. This is going to bring down the derivatives system (and the financial system).

There are (over) one quadrillion dollars of derivatives and most of them are related to interest rates. The spiking of interest rates in the United States may set that off. What is going to happen in the world is eventually we are going to come to a moment where there is going to be massive bankruptcies around the globe.

What is going to be left after the dust settles is gold, and some people are going to have it and some people are not. Then the problem is going to be to hold on to what you’ve got because it’s not going to be a very pleasant world.

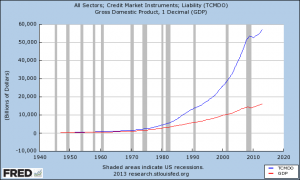

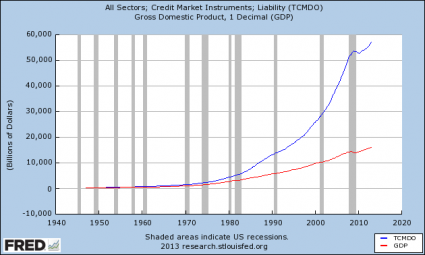

Right now, there are about 441 trillion dollars of interest rate derivatives sitting out there. If interest rates stay about where they are right now and they don’t go much higher, we will be fine. But if they start going much higher, all bets will be off and we could see financial carnage on a scale that we have never seen before.

And at the moment the big banks have got to behave themselves because the government is investigating allegations that they have been cheating pension funds and other investors out of millions of dollars by manipulating the trading of interest rate derivatives. The following is from an article that the Telegraph posted on Friday…

The Commodity Futures Trading Commission (CFTC) is probing 15 banks over allegations that they instructed brokers to carry out trades that would move ISDAfix, the leading benchmark rate for interest rate swaps.

Pension funds and companies who invest in interest rate derivatives often deal with banks to insure against big movements in the ISDAfix rate or to speculate on changes to interest rate swaps

ISDAfix is published each morning after banks submit bids for swaps via Icap, the inter-dealer broker, in a number of currencies. The CFTC has been investigating suggestions that the banks deliberately moved the rate in order to profit on these deals.

Given the hundreds of trillions of dollars worth of interest rate derivatives trades that occur annually, even the slightest manipulation can have a substantial effect. The CFTC, which started to investigate ISDAfix after last summer’s Libor scandal has now been handed emails and phone call recordings that show the rate was deliberately moved, according to Bloomberg.

Essentially they got their hands caught in the cookie jar and so they have got to play it straight (at least for now).

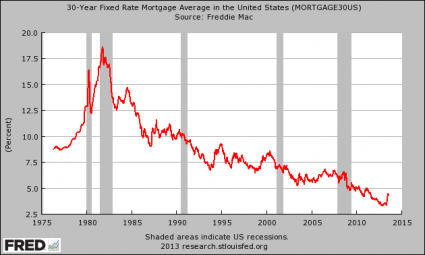

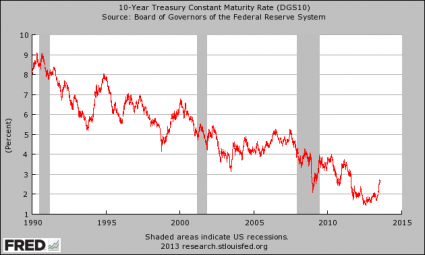

Meanwhile, it looks like the Fed may not be able to keep long-term interest rates down for much longer.

The Federal Reserve has been using quantitative easing to try to keep long-term interest rates low, but now some officials over at the Fed are becoming extremely alarmed about how bloated the Fed balance sheet has become. For example, the following was recently written by the head of the Dallas Fed, Richard Fisher…

This later program is referred to as quantitative easing, or QE, by the public and as large-scale asset purchases, or LSAPs, internally at the Fed. As a result of LSAPs conducted over three stages of QE, the Fed’s System Open Market Account now holds $2 trillion of Treasury securities and $1.3 trillion of agency and mortgage-backed securities (MBS). Since last fall, when we initiated the third stage of QE, we have regularly been purchasing $45 billion a month of Treasuries and $40 billion a month in MBS, meanwhile reinvesting the proceeds from the paydowns of our mortgage-based investments. The result is that our balance sheet has ballooned to more than $3.5 trillion. That’s $3.5 trillion, or $11,300 for every man, woman and child residing in the United States.

Fisher has compared the current Fed balance sheet to a “Gordian Knot”, and he hopes that the Fed will be able to unwind this knot without creating “market havoc”…

The point is: We own a significant slice of these critical markets. This is, indeed, something of a Gordian Knot.

Those of you familiar with the Gordian legend know there were two versions to it: One holds that Alexander the Great simply dispatched with the problem by slicing the intractable knot in half with his sword; the other posits that Alexander pulled the knot out of its pole pin, exposed the two ends of the cord and proceeded to untie it. According to the myth, the oracles then divined that he would go on to conquer the world.

There is no Alexander to simply slice the complex knot that we have created with our rounds of QE. Instead, when the right time comes, we must carefully remove the program’s pole pin and gingerly unwind it so as not to prompt market havoc. For starters though, we need to stop building upon the knot. For this reason, I have advocated that we socialize the idea of the inevitability of our dialing back and eventually ending our LSAPs. In June, I argued for the Chairman to signal this possibility at his last press conference and at last week’s meeting suggested that we should gird our loins to make our first move this fall. We shall see if that recommendation obtains with the majority of the Committee.

But of course it should be obvious to everyone that the Fed is not going to be able to reduce the size of its balance sheet without causing huge distress in the financial markets. A few weeks ago, just the suggestion that the Fed may eventually begin to slow down the pace of quantitative easing caused the markets to throw an epic temper tantrum.

Unfortunately, the Fed may not be able to keep control of long-term interest rates even if they continue quantitative easing indefinitely. Over the past several weeks long-term interest rates have been rising steadily, and the yield on 10 year U.S. Treasuries crept a bit higher on Monday.

At this point, many on Wall Street are convinced that the bull market for bonds is over and that rates will eventually go much, much higher than they are right now no matter what the Fed does. The following is an excerpt from a recent CNBC article…

The Federal Reserve will lose control of interest rates as the “great rotation” out of bonds into equities takes off in full force, according to one market watcher, who sees U.S. 10-year Treasury yields hitting 5-6 percent in the next 18-24 months.

“It is our opinion that interest rates have begun their assent, that the Fed will eventually lose control of interest rates. The yield curve will first steepen and then will shift, moving rates significantly higher,” said Mike Crofton, President and CEO, Philadelphia Trust Company told CNBC on Wednesday.

If the yield on 10 year U.S. Treasuries does hit 6 percent, we are going to have a major disaster on our hands.

Hugo Salinas Price is exactly right – the derivatives bubble is the number one threat that our financial system is facing, and it could potentially bring down a whole bunch of our big banks.

But for the moment, Wall Street is still in a euphoric mood. The Dow is near a record high and many investors are hoping that this rally will last for the rest of the year.

Unfortunately, I wouldn’t count on that happening. The truth is that the stock market has become completely divorced from economic reality.

Since March 2009, the size of the U.S. economy has grown by approximately $1.3 trillion, but stock market wealth has grown by an astounding $12 trillion.

And the stock market has just kept on rising even though GDP growth forecasts have been steadily falling.

It doesn’t make any sense.

But Obama, Bernanke and the wizards on Wall Street assure us that there is no end to the party in sight.

Believe them at your own peril.

The people at the controls are completely and totally clueless and we are rapidly careening toward disaster.

Perhaps we should do what one little town in Minnesota did and put a 4-year-old kid in charge.

That kid certainly could not be much worse than our current leadership, don’t you think?