Has the next major economic downturn already started? The way that you would answer that question would probably depend on where you live. If you live in New York City, or the suburbs of Washington D.C., or you work for one of the big tech firms in the San Francisco area, you would probably respond to such a question by saying of course not. In those areas, the economy is doing great and prices for high end homes are still booming. But in most of the rest of the nation, evidence continues to mount that the next recession has already begun for the poor and the middle class. As you will read about below, major retailers had an absolutely dreadful start to 2014 and home sales are declining just as they did back in 2007 before the last financial crisis. Meanwhile, the U.S. economy continues to lose more good jobs and 20 percent of all U.S. families do not have a single member that is employed at this point. 2014 is turning out to be eerily similar to 2007 in so many ways, but most people are not paying attention.

Has the next major economic downturn already started? The way that you would answer that question would probably depend on where you live. If you live in New York City, or the suburbs of Washington D.C., or you work for one of the big tech firms in the San Francisco area, you would probably respond to such a question by saying of course not. In those areas, the economy is doing great and prices for high end homes are still booming. But in most of the rest of the nation, evidence continues to mount that the next recession has already begun for the poor and the middle class. As you will read about below, major retailers had an absolutely dreadful start to 2014 and home sales are declining just as they did back in 2007 before the last financial crisis. Meanwhile, the U.S. economy continues to lose more good jobs and 20 percent of all U.S. families do not have a single member that is employed at this point. 2014 is turning out to be eerily similar to 2007 in so many ways, but most people are not paying attention.

During the first quarter of 2014, earnings by major U.S. retailers missed estimates by the biggest margin in 13 years. The “retail apocalypse” continues to escalate, and the biggest reason for this is the fact that middle class consumers in the U.S. are tapped out. And this is not just happening to a few retailers – this is something that is happening across the board. The following is a summary of how major U.S. retailers performed in the first quarter of 2014 that was put together by Jim Quinn…

Wal-Mart Profit Plunges By $220 Million as US Store Traffic Declines by 1.4%

Target Profit Plunges by $80 Million, 16% Lower Than 2013, as Store Traffic Declines by 2.3%

Sears Loses $358 Million in First Quarter as Comparable Store Sales at Sears Plunge by 7.8% and Sales at Kmart Plunge by 5.1%

JC Penney Thrilled With Loss of Only $358 Million For the Quarter

Kohl’s Operating Income Plunges by 17% as Comparable Sales Decline by 3.4%

Costco Profit Declines by $84 Million as Comp Store Sales Only Increase by 2%

Staples Profit Plunges by 44% as Sales Collapse and Closing Hundreds of Stores

Gap Income Drops 22% as Same Store Sales Fall

American Eagle Profits Tumble 86%, Will Close 150 Stores

Aeropostale Losses $77 Million as Sales Collapse by 12%

Best Buy Sales Decline by $300 Million as Margins Decline and Comparable Store Sales Decline by 1.3%

Macy’s Profit Flat as Comparable Store Sales decline by 1.4%

Dollar General Profit Plummets by 40% as Comp Store Sales Decline by 3.8%

Urban Outfitters Earnings Collapse by 20% as Sales Stagnate

McDonalds Earnings Fall by $66 Million as US Comp Sales Fall by 1.7%

Darden Profit Collapses by 30% as Same Restaurant Sales Plunge by 5.6% and Company Selling Red Lobster

TJX Misses Earnings Expectations as Sales & Earnings Flat

Dick’s Misses Earnings Expectations as Golf Store Sales Plummet

Home Depot Misses Earnings Expectations as Customer Traffic Only Rises by 2.2%

Lowes Misses Earnings Expectations as Customer Traffic was Flat

That is quite a startling list.

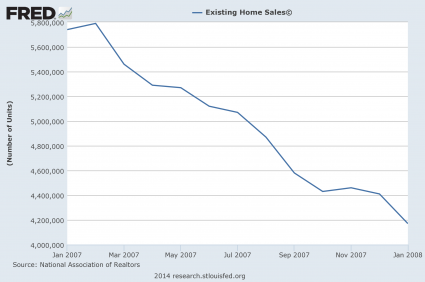

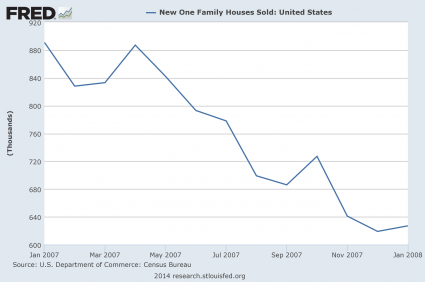

But plummeting retail sales are not the only sign that the U.S. middle class is really struggling right now. Home sales have also been extremely disappointing for quite a few months. This is how Wolf Richter described what we have been witnessing…

This is precisely what shouldn’t have happened but was destined to happen: Sales of existing homes have gotten clobbered since last fall. At first, the Fiscal Cliff and the threat of a US government default – remember those zany times? – were blamed, then polar vortices were blamed even while home sales in California, where the weather had been gorgeous all winter, plunged more than elsewhere.

Then it spread to new-home sales: in April, they dropped 4.7% from a year ago, after March’s year-over-year decline of 4.9%, and February’s 2.8%. Not a good sign: the April hit was worse than February’s, when it was the weather’s fault. Yet April should be the busiest month of the year (excellent brief video by Lee Adler on this debacle).

We have already seen that in some markets, in California for example, sales have collapsed at the lower two-thirds of the price range, with the upper third thriving. People who earn median incomes are increasingly priced out of the market, and many potential first-time buyers have little chance of getting in. In San Diego, for example, sales of homes below $200,000 plunged 46% while the upper end is doing just fine.

As Richter noted, sales of upper end homes are still doing fine in many areas.

But how long will that be able to continue if things continue to get even worse for the poor and the middle class? Traditionally, the U.S. economy has greatly depended upon consumer spending by the middle class. If that continues to dry up, how long can we avoid falling into a recession? For even more numbers that seem to indicate economic trouble for the middle class, please see my previous article entitled “27 Huge Red Flags For The U.S. Economy“.

Other analysts are expressing similar concerns. For example, check out what John Williams of shadowstats.com had to say during one recent interview…

We’re turning down anew. The first quarter should revise into negative territory… and I believe the second quarter will report negative as well.

That will all happen by July 30 when you have the annual revisions to the GDP. In reality the economy is much weaker than that. Economic growth is overstated with the GDP because they understate inflation, which is used in deflating the number…

What we’re seeing now is just… we’ve been barely stagnant and bottomed out… but we’re turning down again.

The reason for this is that the consumer is strapped… doesn’t have the liquidity to fuel the growth in consumption.

Income… the median household income, net of inflation, is as low as it was in 1967. The average guy is not staying ahead of inflation…

This has been a problem now for decades… You were able to buy consumption from the future by borrowing more money, expanding your debt. Greenspan saw the problem was income, so he encouraged debt expansion.

That all blew apart in 2007/2008… the income problems have continued, but now you don’t have the ability to borrow money the way you used to. Without that and the income problems remaining, there’s no way that consumption can grow faster than inflation if income isn’t.

As a result – personal consumption is more than two thirds of the economy – there’s no way you can have positive sustainable growth in the U.S. economy without the consumer being healthy.

The key to the health of the middle class is having plenty of good jobs.

But the U.S. economy continues to lose more good paying jobs.

For example, Hewlett-Packard has just announced that it plans to eliminate 16,000 more jobs in addition to the 34,000 job cuts that have already been announced.

Today, there are 27 million more working age Americans that do not have a job than there were in 2000, and the quality of our jobs continues to decline.

This is absolutely destroying the middle class. Unless the employment situation in this country starts to turn around, there does not seem to be much hope that the middle class will recover any time soon.

Meanwhile, there are emerging signs of trouble for the wealthy as well.

For instance, just like we witnessed back in 2007, things are starting to look a bit shaky at the “too big to fail” banks. The following is an excerpt from a recent CNBC report…

Citigroup has joined the ranks of those with trading troubles, as a high-ranking official told the Deutsche Bank 2014 Global Financial Services Investor Conference Tuesday that adjusted trading revenue probably will decline 20 percent to 25 percent in the second quarter on an annualized basis.

“People are uncertain,” Chief Financial Officer John Gerspach said of investor behavior, according to an account from the Wall Street Journal. “There just isn’t a lot of movement.”

In recent weeks, officials at JPMorgan Chase and Barclays also both reported likely drops in trading revenue. JPMorgan said it expected a decline of 20 percent of the quarter, while Barclays anticipates a 41 percent drop, prompting it to announce mass layoffs that will pare 19,000 jobs by the end of 2016.

Remember, very few people expected a recession the last time around either. In fact, Federal Reserve Chairman Ben Bernanke repeatedly promised us that we would not have a recession and then we went on to experience the worst economic downturn since the Great Depression.

It will be the same this time as well. Just like in 2007, we will continue to get an endless supply of “hopetimism” from our politicians and the mainstream media, and they will continue to fill our heads with visions of rainbows, unicorns and economic prosperity for as far as the eyes can see.

But then the next recession will strike and most Americans will be completely blindsided by it.