Does the economy move in predictable waves, cycles or patterns? There are many economists that believe that it does, and if their projections are correct, the rest of this decade is going to be pure hell for the United States. Many mainstream economists want nothing to do with economic cycle theorists, but it should be noted that economic cycle theories have enabled some analysts to correctly predict the timing of recessions, stock market peaks and stock market crashes over the past couple of decades. Of course none of the theories discussed below is perfect, but it is very interesting to note that all of them seem to indicate that the U.S. economy is about to enter a major downturn. So will the period of 2015 to 2020 turn out to be pure hell for the United States? We will just have to wait and see.

Does the economy move in predictable waves, cycles or patterns? There are many economists that believe that it does, and if their projections are correct, the rest of this decade is going to be pure hell for the United States. Many mainstream economists want nothing to do with economic cycle theorists, but it should be noted that economic cycle theories have enabled some analysts to correctly predict the timing of recessions, stock market peaks and stock market crashes over the past couple of decades. Of course none of the theories discussed below is perfect, but it is very interesting to note that all of them seem to indicate that the U.S. economy is about to enter a major downturn. So will the period of 2015 to 2020 turn out to be pure hell for the United States? We will just have to wait and see.

One of the most prominent economic cycle theories is known as “the Kondratieff wave”. It was developed by a Russian economist named Nikolai Kondratiev, and as Wikipedia has noted, his economic theories got him into so much trouble with the Russian government that he was eventually executed because of them…

The Soviet economist Nikolai Kondratiev (also written Kondratieff) was the first to bring these observations to international attention in his book The Major Economic Cycles (1925) alongside other works written in the same decade. Two Dutch economists, Jacob van Gelderen and Samuel de Wolff, had previously argued for the existence of 50 to 60 year cycles in 1913. However, the work of de Wolff and van Gelderen has only recently been translated from Dutch to reach a wider audience.

Kondratiev’s ideas were not supported by the Soviet government. Subsequently he was sent to the gulag and was executed in 1938.

In 1939, Joseph Schumpeter suggested naming the cycles “Kondratieff waves” in his honor.

In recent years, there has been a resurgence of interest in the Kondratieff wave. The following is an excerpt from an article by Christopher Quigley that discussed how this theory works…

Kondratiev’s analysis described how international capitalism had gone through many such “great depressions” and as such were a normal part of the international mercantile credit system. The long term business cycles that he identified through meticulous research are now called “Kondratieff” cycles or “K” waves.

The K wave is a 60 year cycle (+/- a year or so) with internal phases that are sometimes characterized as seasons: spring, summer, autumn and winter:

- Spring phase: a new factor of production, good economic times, rising inflation

- Summer: hubristic ‘peak’ war followed by societal doubts and double digit inflation

- Autumn: the financial fix of inflation leads to a credit boom which creates a false plateau of prosperity that ends in a speculative bubble

- Winter: excess capacity worked off by massive debt repudiation, commodity deflation & economic depression. A ‘trough’ war breaks psychology of doom.

Increasingly economic academia has come to realize the brilliant insight of Nikolai Kondratiev and accordingly there have been many reports, articles, theses and books written on the subject of this “cyclical” phenomenon. An influential essay, written by Professor W. Thompson of Indiana University, has indicated that K waves have influenced world technological development since the 900’s. His thesis states that “modern” economic development commenced in 930AD in the Sung province of China and he propounds that since this date there have been 18 K waves lasting on average 60 years.

So what does the Kondratieff wave theory suggest is coming next for us?

Well, according to work done by Professor W. Thompson of Indiana University, we are heading into an economic depression that should last until about the year 2020…

Based on Professor Thompson’s analysis long K cycles have nearly a thousand years of supporting evidence. If we accept the fact that most winters in K cycles last 20 years (as outlined in the chart above) this would indicate that we are about halfway through the Kondratieff winter that commenced in the year 2000. Thus in all probability we will be moving from a “recession” to a “depression” phase in the cycle about the year 2013 and it should last until approximately 2017-2020.

But of course the Kondratieff wave is far from the only economic cycle theory that indicates that we are heading for an economic depression.

The economic cycle theories of author Harry Dent also predict that we are on the verge of massive economic problems. He mainly focuses on demographics, and the fact that our population is rapidly getting older is a major issue for him. The following is an excerpt from a Business Insider article that summarizes the major points that Dent makes in his new book…

- Young people cause inflation because they “cost everything and produce nothing.” But young people eventually “begin to pay off when they enter the workforce and become productive new workers (supply) and higher-spending consumers (demand).”

- Unfortunately, the U.S. reached its demographic “peak spending” from 2003-2007 and is headed for the “demographic cliff.” Germany, England, Switzerland are all headed there too. Then China will be the first emerging market to fall off the cliff, albeit in a few decades. The world is getting older.

- The U.S. stock market will crash. “Our best long-term and intermediate cycles suggest another slowdown and stock crash accelerating between very early 2014 and early 2015, and possibly lasting well into 2015 or even 2016. The worst economic trends due to demographics will hit between 2014 and 2019. The U.S. economy is likely to suffer a minor or major crash by early 2015 and another between late 2017 and late 2019 or early 2020 at the latest.”

- “The everyday consumer never came out of the last recession.” The rich are the ones feeling great and spending money, as asset prices (not wages) are aided by monetary stimulus.

- The U.S. and Europe are headed in the same direction as Japan, a country still in a “coma economy precisely because it never let its debt bubble deleverage,” Dent argues. “The only way we will not follow in Japan’s footsteps is if the Federal Reserve stops printing new money.”

- “The reality is stark, when dyers start to outweigh buyers, the market changes.” It all comes down to an aging population, Dent writes. “Fewer spenders, borrowers, and investors will be around to participate in the next boom.”

- The U.S. has a crazy amount of debt and “economists and politicians have acted like we can just wave a magic wand of endless monetary injections and bailouts and get over what they see as a short-term crisis.” But the problem, Dent says, is long-term and structural — demographics.

- Businesses can “dominate the years to come” by focusing on cash and cash flow, being “lean and mean,” deferring major capital expenditures, selling nonstrategic real estate, and firing weak employees now.

- The big four challenges in the years ahead will be 1) private and public debt 2) health care and retirement entitlements 3) authoritarian governance around the globe and 4) environmental pollution that threatens the global economy.

According to Dent, “You need to prepare for that crisis, which will occur between 2014 and 2023, with the worst likely starting in 2014 and continuing off and on into late 2019.”

So just like the Kondratieff wave, Dent’s work indicates that we are going to experience a major economic crisis by the end of this decade.

Another economic cycle theory that people are paying more attention to these days is the relationship between sun spot cycles and the stock market. It turns out that market peaks often line up very closely with peaks in sun spot activity. This is a theory that was first popularized by an English economist named William Stanley Jevons.

Sun spot activity appears to have peaked in early 2014 and is projected to decline for the rest of the decade. If historical trends hold up, that is a very troubling sign for the stock market.

And of course there are many, many other economic cycle theories that seem to indicate that trouble is ahead for the United States as well. The following is a summary of some of them from an article by GE Christenson and Taki Tsaklanos…

Charles Nenner Research (source)

Stocks should peak in mid-2013 and fall until about 2020. Similarly, bonds should peak in the summer of 2013 and fall thereafter for 20 years. He bases his conclusions entirely on cycle research. He expects the Dow to fall to around 5,000 by 2018 – 2020.Kress Cycles (Clif Droke) (source)

The major 120 year cycle plus all minor cycles trend down into late 2014. The stock market should decline hard into late 2014.Elliott Wave (Robert Prechter) (source)

He believes that the stock market has peaked and has entered a generational bear-market. He anticipates a crash low in the market around 2016 – 2017.Market Energy Waves (source)

He sees a 36 year cycle in stock markets that is peaking in mid-2013 and will cycle down for 2013 – 2016. “… the controlling energy wave is scheduled to flip back to negative on July 19 of this year.” Equity markets should drop 25 – 50%.Armstrong Economics (source)

His economic confidence model projects a peak in confidence in August 2013, a bottom in September 2014, and another peak in October 2015. The decline into January 2020 should be severe. He expects a world-wide crash and contraction in economies from 2015 – 2020.Cycles per Charles Hugh Smith (source)

He discusses four long-term cycles that bottom in the 2010 – 2020 period. They are: Credit expansion/contraction cycle, Price inflation/wage cycle, Generational cycle, and Peak oil extraction cycle.

So does history repeat itself?

Well, it should be disconcerting to a lot of people that 2014 is turning out to be eerily similar to 2007. But we never learned the lessons that we should have learned from the last major economic crisis, and most Americans are way too apathetic to notice that we are making many of the very same mistakes all over again.

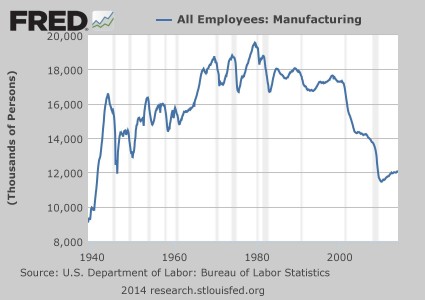

And in recent months there have been a whole host of indications that the next major economic downturn is just around the corner. For example, just this week we learned that manufacturing job openings have declined for four months in a row. For many more indicators like this, please see my previous article entitled “17 Facts To Show To Anyone That Believes That The U.S. Economy Is Just Fine“.

Let’s hope that all of the economic cycle theories discussed above are wrong this time, but we would be quite foolish to ignore their warnings.

Everything indicates that a great economic storm is rapidly approaching, and we should use this time of relative calm to get prepared while we still can.

{kind=link}