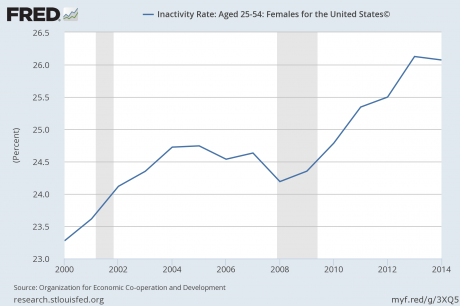

If there were any shreds of hope left that the stunning decline of the middle class could be turned around, Obamacare has absolutely destroyed them. Over the past decade or so, the middle class in the United States has been absolutely eviscerated. The number of working age Americans without a job has increased by 27 million since the year 2000, median household income in the U.S. has fallen for five years in a row, and the poverty numbers in this country are spiraling out of control. And now here comes Obamacare. As you will see below, Obamacare is causing millions of Americans to lose their current health insurance policies, it is causing health insurance premiums to explode to absolutely ridiculous levels, and it is systematically killing jobs even though the employer mandate has been delayed for a while. All of this is creating a tremendous amount of stress for millions of middle class families that are already stretched extremely thin financially. According to CNN, a survey that was conducted earlier this year found that 76 percent of all Americans are living paycheck to paycheck. Most of those families simply cannot afford to pay much higher health insurance premiums for new policies that also come with much larger deductibles and significantly increased out-of-pocket costs. Millions of those families will ultimately end up choosing to do without health insurance altogether, and that will create a whole host of new problems. This is a disaster that is so enormous that it is really hard to put into words. If the U.S. health care system was a separate country, it would be the 6th largest economy on the entire globe all by itself. And now Obamacare is going to bring the entire U.S. health care system to its knees.

If there were any shreds of hope left that the stunning decline of the middle class could be turned around, Obamacare has absolutely destroyed them. Over the past decade or so, the middle class in the United States has been absolutely eviscerated. The number of working age Americans without a job has increased by 27 million since the year 2000, median household income in the U.S. has fallen for five years in a row, and the poverty numbers in this country are spiraling out of control. And now here comes Obamacare. As you will see below, Obamacare is causing millions of Americans to lose their current health insurance policies, it is causing health insurance premiums to explode to absolutely ridiculous levels, and it is systematically killing jobs even though the employer mandate has been delayed for a while. All of this is creating a tremendous amount of stress for millions of middle class families that are already stretched extremely thin financially. According to CNN, a survey that was conducted earlier this year found that 76 percent of all Americans are living paycheck to paycheck. Most of those families simply cannot afford to pay much higher health insurance premiums for new policies that also come with much larger deductibles and significantly increased out-of-pocket costs. Millions of those families will ultimately end up choosing to do without health insurance altogether, and that will create a whole host of new problems. This is a disaster that is so enormous that it is really hard to put into words. If the U.S. health care system was a separate country, it would be the 6th largest economy on the entire globe all by itself. And now Obamacare is going to bring the entire U.S. health care system to its knees.

Obamacare: Since October 1st, The Number Of Americans With Health Insurance Has Fallen By Nearly 4 Million

Last week, Barack Obama decided to allow Americans to keep their current health insurance plans for one more year.

Isn’t that generous of him? Especially considering the fact that he promised us over and over that if we liked our current health insurance policies that we would be able to keep them permanently.

The funny thing is that Obama is not actually changing the law. So if your health insurance company allows you to stay on your current health insurance plan that does not meet the requirements of Obamacare, it is technically breaking the law.

And if you continue to stay on that current health insurance plan that does not meet the requirements of Obamacare, you are technically breaking the law.

It is just that Obama has promised not to enforce what the law says for one year.

For a president to just blatantly disregard the rule of law is a very dangerous precedent. Do we really want the president to have the power to decide what laws are going to be enforced and what laws are not going to be enforced?

That sounds dangerously close to a dictatorship to me.

And in any event, there are many Americans that are not going to be able to keep their current policies no matter what Obama says. For example, just two hours after Obama announced his plan last week, the state of Washington announced that they would not be allowing insurance companies to extend their old health insurance plans if they don’t comply with Obamacare under any circumstances…

State Insurance Commissioner Mike Kreidler has rejected President Obama’s proposal to allow insurance companies to extend health insurance policies for people who have received notices that their policies will be cancelled at the end of the year.

Within two hours of President Obama’s news conference announcing the proposed administrative fix for Americans upset by their policy cancellations, Kreidler issued a statement rejecting the proposal.

“I understand that many people are upset by the notices they have recently received from their health plans and they may not need the new benefits [in the Affordable Care Act] today,” he said. “But I have serious concerns about how President Obama’s proposal would be implemented and more significantly, its potential impact on the overall stability of our health insurance market.”

“I do not believe his proposal is a good deal for the state of Washington,” Kreidler’s statement continued. “We will not be allowing insurance companies to extend their policies.”

How do you think the people of the state of Washington will respond to that?

Things are getting crazy out there, and the number of people that are losing their health insurance policies is absolutely stunning.

According to the Wall Street Journal, so far 106,185 Americans have enrolled in Obamacare since October 1st. Most of those that have successfully enrolled have done so through the state insurance exchanges. So far, only 26,794 Americans have signed up for health insurance using the federally run exchanges on HealthCare.gov.

Meanwhile, during that same time frame, 4.02 million Americans have had their health insurance policies cancelled.

So that means that the number of Americans with health insurance has actually decreased by 3,918,205 since October 1st.

Wasn’t Obamacare supposed to result in more Americans being covered?

And according to U.S. Senator Rand Paul, Obama not only knew that this would happen, he actually wrote the regulation that caused this to happen…

“I’m still learning about it. It’s 20,000 pages of regulations. The Bill was 2,000 pages and I didn’t realize this until this week, the whole idea of you losing or getting your insurance cancelled wasn’t in the original Obamacare. It was a regulation WRITTEN BY PRESIDENT OBAMA, three months later. So we had a vote, this is before I got up there. The Republicans had a vote to try to cancel that regulation so you COULDN’T BE CANCELLED, to grandfather everybody in. You know what the vote was? Straight party line. EVERY DEMOCRAT VOTED TO KEEP THE RULE THAT CANCELS YOUR INSURANCE.”

So now millions of Americans, including women battling cancer, are losing health insurance plans that they were depending upon.

Thanks Obama?

Obamacare: Skyrocketing Health Insurance Premiums

How much more are you willing to pay for health insurance than you are paying right now?

10 percent?

20 percent?

30 percent?

Well, according to one study health insurance premiums for men are going to go up by an average of 99 percent under Obamacare and health insurance premiums for women are going to go up by an average of 62 percent under Obamacare.

And of course some groups are going to see increases that are much larger than that. For example, it is being projected that health insurance premiums for healthy 30-year-old men will rise by an average of 260 percent.

Ouch.

And there are some families out there that have already been hit with health insurance premium increases that are absolutely jaw-dropping. In a previous article, I included the example of one family down in Texas that has been hit with a 539% rate increase…

Obamacare is named the “Affordable Care Act,” after all, and the President promised the rates would be “as low as a phone bill.” But I just received a confirmed letter from a friend in Texas showing a 539% rate increase on an existing policy that’s been in good standing for years.

As the letter reveals (see below), the cost for this couple’s policy under Humana is increasing from $212.10 per month to $1,356.60 per month. This is for a couple in good health whose combined income is less than $70K — a middle-class family, in other words.

Obamacare: Enormous Deductibles And Huge Out-Of-Pocket Expenses For All

It isn’t just health insurance premiums that are going up either. Deductibles are going up too. In fact, just check out what one survey of Americans living in seven different states recently discovered…

Expenses for some policies can reach $6,350 for a single person and $12,700 per family, the most allowed by the health-care law, according to a survey by HealthPocket Inc. of seven states, including California and Ohio. That’s 26 percent higher than the average deductible in the seven states, and a scenario likely repeated across the country, said Kev Coleman, head of research and data at Sunnyvale, California-based HealthPocket.

That same article has a great quote from an elderly New Jersey resident. 82-year-old Larry Saphire thinks that if you have to pay a $5,000 deductible up front, “you might as well not have any insurance at all”…

“If you have to pay $5,000 upfront” when illness hits, “you might as well not have any insurance at all,” said Larry Saphire, 82, of West Orange, New Jersey, who shopped for coverage for his wife and two children, ages 16 and 21. “That’s not insurance.”

On California’s state-run exchange site, the standard low-premium “bronze” plan carries a $5,000 deductible per person, a $60 co-pay to see a doctor and a 30 percent fee, known as coinsurance, on hospital care. In Rhode Island, Blue Cross Blue Shield’s bronze plan has a $5,800 deductible while Missouri’s U.S.-run exchange offers plans by Anthem Blue Cross with the maximum-allowable $6,350 in out-of-pocket costs.

Obamacare: The Quality Of Care Is Going To Go Into The Toilet

A lot of Americans that are signing up for Obamacare are going to be in for a huge shock. Many of the best hospitals and many of the best doctors are not covered by their plans…

Meanwhile, sometime between March and June, the other shoe drops: People who bought exchange policies realize that the restricted networks insurers created to keep the premium costs low cut out the best hospitals and doctors. A newly insured child with cancer cannot get into a top pediatric hospital because her insurance has zero coverage for out-of-network emergency care. Tearful Mom goes on the evening news and says that she thought when they went on Obamacare, that meant they were safe, and why can’t I take my baby to Philadelphia Children’s Hospital, Mr. President?

Can you imagine being a parent in that situation?

In response, some hospitals are already filing suit over this. For instance, check out what is happening over in Seattle…

Seattle Children’s Hospital filed suit against Washington State’s Office of the Insurance Commissioner this week, after Obamacare implementation caused the hospital to be cut from four of the six insurance plans offered by the new Washington Health Benefit Exchange.

And even if you are on Medicare that does not mean that the quality of your care is going to stay the same either. As Reuters just reported, UnitedHealth is dumping “thousands of doctors” from their Medicare Advantage plans for the elderly because of Obamacare…

UnitedHealth Group dropped thousands of doctors from its networks in recent weeks, leaving many elderly patients unsure whether they need to switch plans to continue seeing their doctors, the Wall Street Journal reported on Friday.

The insurer said in October that underfunding of Medicare Advantage plans for the elderly could not be fully offset by the company’s other healthcare business. The company also reported spending more healthcare premiums on medical claims in the third quarter, due mainly to government cuts to payments for Medicare Advantage services.

In the United States, we already pay much more for health care than everyone else in the world, and we typically have to wait longer to see a doctor than most of the rest of the industrialized world does.

Now Obamacare is going to make all of this even worse, and the quality of the care that we receive is going to go downhill fast.

Obamacare: The Jobs Killer

A while back, Obama unilaterally made the decision to delay the implementation of the employer mandate until 2015.

That was probably a good political decision, because it would have been a huge political issue in the 2014 elections.

But the truth is that we won’t have to wait until 2015 for Obamacare to start killing jobs. In fact, according to CNBC it is already happening…

Approximately one-third of business decision-makers at companies with between 40 and 500 employees, say the health-care law has already increased their costs due to hikes in both the cost of insurance and compliance, according to a recent report from political-research firm Public Opinion Strategies. As a result, many business leaders say they are already making personnel decisions based on the Affordable Care Act.

Among franchised businesses, 27 percent report their company has replaced full-time workers with part-time workers and 31 percent have reduced worker hours. Among non-franchised businesses, 12 percent are replacing full-time workers with part-time workers or reducing hours. This is happening now, with more than a year before the mandate goes into effect; and undoubtedly, these numbers will rise as we approach next July’s “look back” period for tabulating workers’ hours.

It is kind of startling that we are already seeing employers make such big changes even though the employer mandate does not come into effect until 2015. You can find a very long list of some of the employers that have already either eliminated jobs or cut hours because of Obamacare right here.

Remember, this is just the tip of the iceberg. Once we get closer to the deadline things are going to get much, much worse.

At a time when the middle class desperately needs jobs, Obamacare is going to slaughter them.

And even if you are able to keep your current job, that does not mean that your health plan will remain the same. In fact, Forbes is projecting that a staggering 51 percent of all employment-based health insurance plans will be canceled and replaced with new ones.

Overall, Forbes is projecting that an astounding 93 million Americans will eventually lose their current health insurance policies due to Obamacare.

Obamacare: Providing Huge Incentives For Many Americans To Work Less And Make Less Money

Did you know that Obamacare is going to cause millions of Americans to want to keep their incomes under certain levels?

If you make too much money under Obamacare, you will miss out on some absolutely massive health care subsidies. The following is an excerpt from one of my previous articles…

—–

The figures that you are about to see were calculated using the Kaiser Family Foundation subsidy calculator. These numbers apply to a husband and a wife that are both 62 years old.

A non-smoking, married couple living in San Francisco, California earning $63,000 a year will have to pay $20,318 a year for a silver plan under Obamacare and $12,647 a year for a bronze plan.

At $63,000, that couple would be making too much money to be eligible for a subsidy, so that couple will have to pay the total cost of whatever plan they choose by themselves.

But if that couple only made $62,000 a year, things would dramatically change.

The plans would still cost the same, but the couple would now be eligible for an Obamacare subsidy of $14,428.

So a silver plan would end up costing them only $5,890, and they would ultimately pay nothing for a bronze plan.

In other words, by reducing their income by $1,000, that couple would save $14,428 if they got a silver plan or they would save $12,647 if they got a bronze plan.

Isn’t that bizarre?

—–

In the end, millions upon millions of middle class families will decide to go without health insurance entirely for one reason or another.

This will work great until they get into an accident or become seriously ill.

As I have discussed previously, approximately 60 percent of all personal bankruptcies in the United States are related to medical bills. And most of those bankruptcies actually happen to people that are supposedly “covered” by health insurance.

Obamacare is going to make all of this so much worse. Millions of middle class families will end up with no health insurance at all, and because so many of them are living paycheck to paycheck a single health emergency will be enough to send them hurtling down the path to financial oblivion.

If you get into an accident, a visit to the emergency room and a single night in the hospital can easily cost tens of thousands of dollars in many areas of the country.

If you get a serious illness such as cancer, the medical bills can be absolutely astronomical. For instance, there are many cancer patients that rack up medical bills well in excess of a million dollars by the time that they die.

Something desperately needs to be done about our horrible health care system. Unfortunately, Obamacare is going to make just about everything that is bad about our current system much, much worse.

And the American people are becoming increasingly disgusted and frustrated with Obamacare. According to Real Clear Politics, an average of recent opinion polls shows that the American people are opposed to Obamacare by an average margin of 14.2 percentage points.

So what do you think about Obamacare?

Please feel free to share your opinion by posting a comment below, and please share this information with as many people as you possibly can.

The critics of Obamacare have been proven right. The Obama administration promised that health insurance premiums would go down. Instead, they have absolutely skyrocketed. The Obama administration promised that Obamacare would not kill jobs. Instead, firms are hiring fewer workers because of suffocating health care costs. As you will see below, even the Federal Reserve is admitting this. The Obama administration also promised that the big health insurance companies would love the new Obamacare plans and would eagerly compete with one another to win customers in the new health insurance marketplaces. Instead, many of the big health insurance companies are now dropping Obamacare plans altogether.

The critics of Obamacare have been proven right. The Obama administration promised that health insurance premiums would go down. Instead, they have absolutely skyrocketed. The Obama administration promised that Obamacare would not kill jobs. Instead, firms are hiring fewer workers because of suffocating health care costs. As you will see below, even the Federal Reserve is admitting this. The Obama administration also promised that the big health insurance companies would love the new Obamacare plans and would eagerly compete with one another to win customers in the new health insurance marketplaces. Instead, many of the big health insurance companies are now dropping Obamacare plans altogether.

{kind=link}